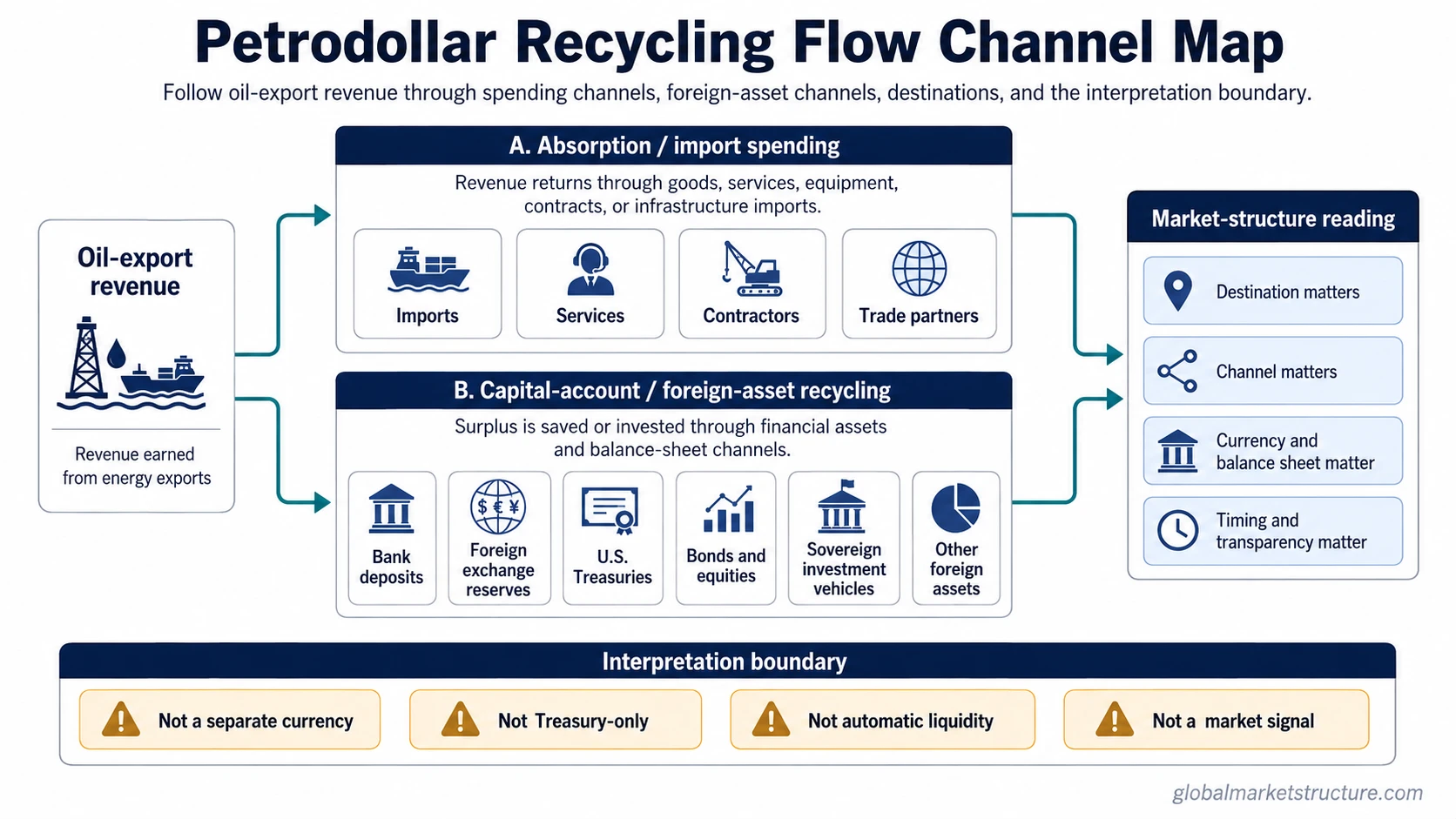

Petrodollar recycling is the process where oil-export revenues return to the global economy through import spending or investment in foreign assets. The main routes are absorption through goods and services and capital-account recycling through bank deposits, reserves, Treasuries, bonds, equities, and sovereign investment vehicles. It is not a separate currency, not the full petrodollar system, not automatic Treasury buying, and not a trading signal.

Core definition: petrodollar recycling describes how dollar-linked oil revenue earned by exporting countries is spent, saved, invested, or reallocated back into global markets.

Main interpretation boundary: the effect depends on where the money goes. A payment for imports does not have the same market-structure implication as a reserve purchase, a bank deposit, a bond allocation, or a sovereign fund investment.

How petrodollar recycling works

The starting point is oil-export revenue. When an oil-exporting country earns more foreign currency from energy exports than it immediately spends abroad, part of that revenue can re-enter the global economy through goods, services, bank balances, reserve assets, securities, or sovereign investment vehicles.

The useful distinction is between spending and financial recycling. Spending absorbs the revenue through imports and foreign services. Financial recycling places the surplus into assets or accounts that can affect reserve balances, banking liquidity, bond demand, portfolio flows, and cross-border capital allocation.

| Channel | What happens | Possible destinations | Market-structure implication | Main limitation |

|---|---|---|---|---|

| Absorption / import spending | Oil revenue is used to buy foreign goods, services, infrastructure, technology, defense goods, or other imports. | Foreign exporters, service providers, contractors, and trade partners. | Revenue returns to the global economy through trade demand rather than through financial asset accumulation. | It should not be read as automatic demand for U.S. Treasuries or automatic dollar-market liquidity. |

| Capital-account / foreign-asset recycling | Oil revenue is saved or invested abroad instead of being immediately spent on imports. | Bank deposits, reserves, government bonds, corporate bonds, equities, sovereign funds, and other foreign assets. | Revenue may influence cross-border capital flows, reserve composition, banking balances, and asset demand. | The effect depends on destination, currency denomination, transparency, balance-sheet channel, and timing. |

Where recycled petrodollars can go

Recycled petrodollars do not have one fixed destination. The same oil-export surplus can be absorbed through imports, placed into banking channels, accumulated as official reserves, invested through public-sector portfolios, or allocated through sovereign investment vehicles.

| Destination | How to read it | Why it changes interpretation |

|---|---|---|

| Imports and services | Oil revenue is spent on goods, services, infrastructure, equipment, or external contracts. | This is an absorption channel, not a direct financial-asset channel. |

| Bank deposits | Surplus revenue sits in domestic or international banking channels. | The liquidity effect depends on the banking system, currency denomination, and balance-sheet use. |

| Foreign exchange reserves | Official-sector balances are held in reserve assets. | Reserve accumulation can matter for currency management, external buffers, and sovereign balance-sheet structure. |

| Foreign holdings of U.S. Treasuries | Some surplus may be allocated to U.S. government securities. | This can connect oil-export surpluses to safe-asset demand, but it is only one possible channel. |

| Bonds and equities | Capital is invested in public or private financial markets. | The market effect depends on asset class, region, mandate, and portfolio allocation. |

| Sovereign wealth fund allocations | Surplus is invested through a state-owned investment vehicle. | This can shift the interpretation from short-term liquidity to long-horizon capital allocation. |

Why the destination matters

Petrodollar recycling can affect market structure only through the channel it actually uses. Import spending supports trade partners and contractors. Bank deposits may affect funding conditions if they connect to active banking balance sheets. Reserve purchases may affect official asset composition. Portfolio allocations may affect bond, equity, or alternative-asset demand.

That is why the phrase should not be treated as a single liquidity signal. A large oil surplus can have different implications depending on whether it is spent, saved, invested, held in reserves, parked in deposits, or reallocated across asset classes.

Interpretation boundary: petrodollar recycling can describe a capital-flow mechanism, but it does not automatically tell the reader that liquidity is easing, the dollar will strengthen, Treasury demand will rise, or risk assets will move in a specific direction.

Petrodollar recycling vs petrodollar system

Petrodollar recycling is narrower than the petrodollar system. Recycling describes what can happen after oil-export revenue is earned: the revenue can be spent abroad, saved, invested, or placed into foreign assets. The broader system refers to the monetary, trade, and geopolitical context around dollar-denominated oil markets.

The difference matters because a recycling analysis should focus on the flow mechanism. It should not turn into a broad argument about dollar dominance, reserve-currency status, energy geopolitics, or collapse narratives.

A practical scenario

Suppose oil prices rise and an oil-exporting country earns more foreign currency than it needs for immediate domestic spending. One portion of the revenue may be used to import equipment, food, services, or infrastructure inputs. Another portion may be saved in bank deposits, added to reserves, or allocated through a sovereign investment vehicle.

The first portion mainly works through trade demand. The second portion works through financial balance sheets and portfolio allocation. Both are part of petrodollar recycling, but they do not mean the same thing for market structure.

Common false readings

| False reading | Cleaner interpretation |

|---|---|

| Petrodollar recycling is a separate currency. | It is a label for oil-export revenue flows, usually discussed in relation to dollar-linked oil trade and foreign-asset recycling. |

| All recycled petrodollars become U.S. Treasury purchases. | Treasuries can be one destination, but imports, deposits, reserves, bonds, equities, and sovereign funds can also absorb the revenue. |

| Petrodollar recycling always creates global liquidity. | The liquidity effect depends on channel, balance-sheet use, currency denomination, banking connection, and asset destination. |

| Petrodollar recycling proves dollar dominance or dollar collapse. | It is one capital-flow mechanism. Reserve-currency arguments require broader evidence than recycling flows alone. |

| Petrodollar recycling is a market signal. | It is context for capital-flow interpretation, not a buy/sell signal or forecast. |

Market-structure interpretation boundary

Petrodollar recycling is most useful as a flow map. It helps separate oil-export income from the channels that absorb or invest that income. The market-structure question is not simply whether oil exporters earned more revenue. The better question is where that revenue went and which balance sheets were affected.

For a cleaner reading, separate five checks: the size of the surplus, the spending-versus-investment split, the currency denomination, the reserve or sovereign-fund channel, and the connection to bank balance sheets or securities markets. The concept becomes weaker when those destinations are unknown or when the claim depends on current allocation data that has not been verified.

FAQ

What is petrodollar recycling?

Petrodollar recycling is the process where oil-export revenues return to the global economy through import spending or investment in foreign assets such as bank deposits, reserves, bonds, equities, Treasuries, and sovereign investment vehicles.

Is petrodollar recycling the same as the petrodollar system?

No. Petrodollar recycling is the flow mechanism after oil revenue is earned. The petrodollar system is the broader monetary and trade context around dollar-linked oil markets.

Do recycled petrodollars always go into U.S. Treasuries?

No. Treasuries can be one possible destination, but oil-export revenues can also be spent on imports, held as deposits, accumulated as reserves, or invested in bonds, equities, sovereign funds, and other foreign assets.

Does petrodollar recycling always create liquidity?

No. The liquidity effect depends on the channel, asset destination, currency denomination, banking-system connection, and whether the revenue is spent, saved, invested, or reallocated.

Can petrodollar recycling be used as a market signal?

No. It is a capital-flow concept that can provide context, but it does not predict equity, bond, oil, or currency returns by itself.