A margin call works by forcing a leveraged account, fund, clearing member, or market participant to restore required equity or collateral after it falls below a required threshold. In market-structure terms, the important issue is not the notice itself, but the adjustment that can follow when many leveraged holders need cash, collateral, or exposure reduction during the same stress window.

A single margin call can remain an account-level event. It becomes more relevant to broader markets when leverage is widespread, liquidity is thin, volatility is rising, and affected holders try to meet collateral demands by reducing positions into weaker market depth.

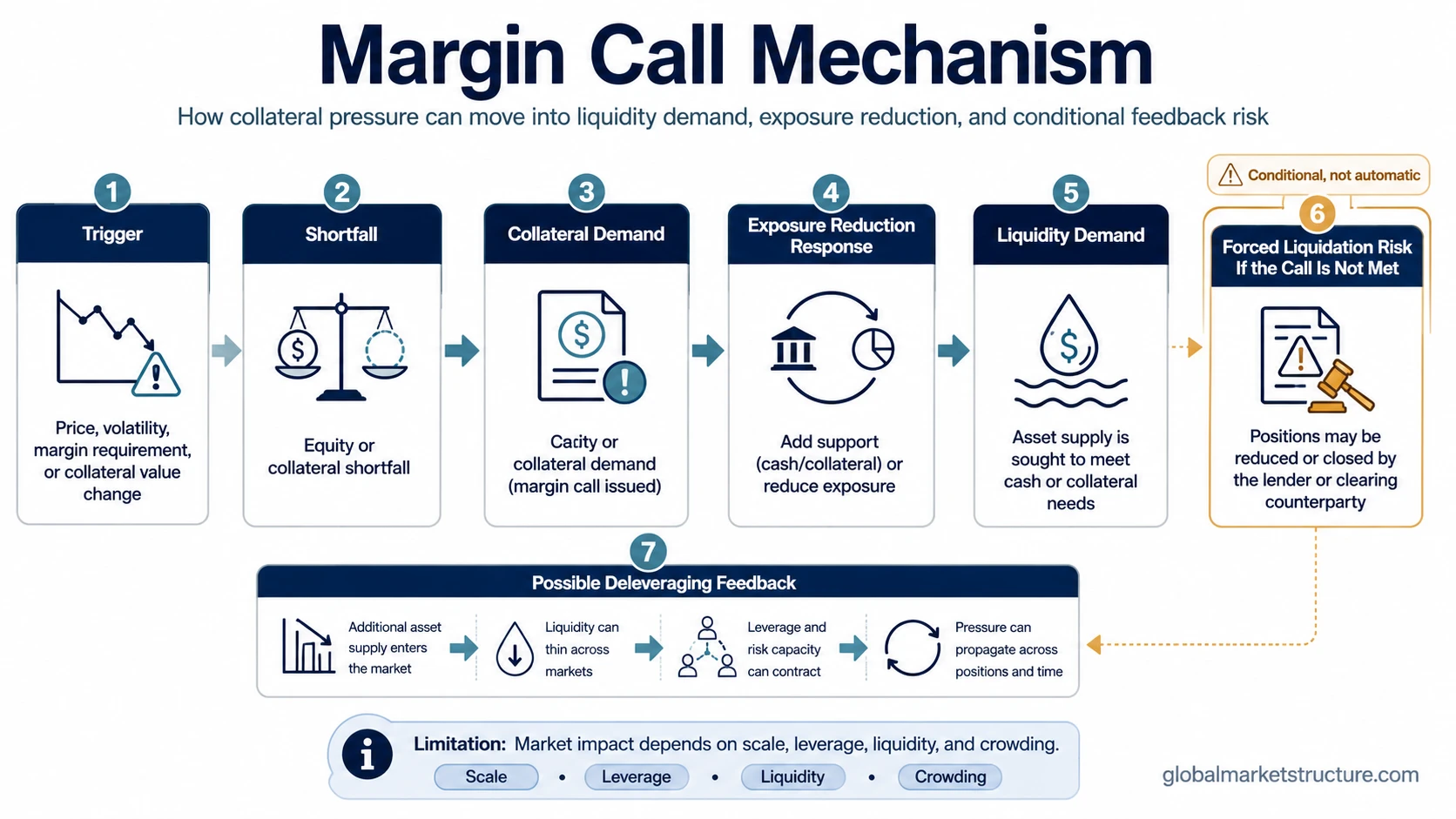

Definition: A margin call is a demand to restore required equity, margin, or collateral. It can be met by adding cash, posting eligible collateral, or reducing exposure. Forced selling is possible, but it is not automatic.

Key Points

- A margin call starts with a collateral or equity shortfall against a required threshold.

- The broader market effect depends on leverage, crowding, volatility, liquidity, and whether many holders react together.

- Forced liquidation can follow if the call is not met or if risk controls require exposure reduction, but it is not the same event as the margin call.

- Deleveraging risk grows when many holders cut borrowed exposure to meet funding or collateral needs.

- Margin calls can amplify stress, but they do not prove that a crash, selloff, or systemic event will occur.

How Margin Calls Work in Market-Structure Terms

A margin call begins when the value of equity or collateral supporting a leveraged position no longer satisfies the required margin level. That shortfall can come from an adverse price move, a rise in required margin, a change in collateral value, or a combination of these forces.

The immediate demand is usually simple: restore the requirement. The broader market question is whether that can happen without asset sales, position cuts, or a scramble for liquidity in the same markets where other leveraged holders are under similar strain.

For market interpretation, the margin call is a funding and collateral stress point. It exposes where leverage depends on stable prices, stable collateral values, available cash, and enough market depth to transact without large price impact.

The Margin Call Mechanism

The mechanism can move from a private account event to a broader market-pressure event only when the adjustment response spreads across holders, funds, clearing members, or connected markets.

- Price, volatility, or margin requirement changes: Collateral value falls, position losses rise, or required margin increases.

- Equity or collateral shortfall appears: The holder no longer satisfies the required threshold.

- Cash or collateral demand follows: The required level must be restored through cash, eligible collateral, or lower exposure.

- Exposure reduction may begin: If cash or collateral is limited, positions may be cut to reduce the margin requirement.

- Forced liquidation risk appears: If the call is not met, liquidation can occur through broker, lender, clearing, or risk-control processes.

- Liquidity demand rises: Affected holders may sell assets, raise cash, or compete for funding while market depth is already weaker.

- Feedback risk grows: Selling can reduce collateral values further, creating additional margin stress for other leveraged holders.

The sequence is conditional. A margin call does not need to become a forced-flow event if liquidity, collateral access, or balance-sheet capacity is sufficient to meet the demand without selling risk assets.

Common Mistake: A Margin Call Is Not Automatically Forced Selling

Common mistake: Treating every margin call as immediate forced selling overstates the mechanism. The call is a demand to restore required support. Forced selling is one possible response, not the definition of the event.

A margin call can be met by adding cash, posting eligible collateral, reducing the size of the leveraged position, or some combination of those responses. Forced selling becomes more likely when liquid resources are limited, collateral is difficult to mobilize, volatility is high, or risk controls require liquidation before the requirement can be restored.

This distinction matters because market stress usually comes from the response channel, not from the call notice alone. The call creates a need for adjustment. The adjustment can become market-moving when many holders need liquidity during the same window.

Conditions That Change the Market Impact

The same margin-call mechanism can have a small or large market effect depending on surrounding structure. Scale, timing, liquidity, and crowding matter more than the existence of a single call.

| Condition | What It Changes | Why It Matters |

|---|---|---|

| High leverage | Small price moves can create larger equity or collateral shortfalls. | More holders may need to restore margin after the same market move. |

| Crowded exposure | Many holders own similar positions or rely on similar collateral. | Position reductions can concentrate in the same assets instead of being spread across markets. |

| Weak market liquidity | Orders have greater price impact because depth is thinner. | The same amount of selling can move prices more than it would in normal conditions. |

| Rising volatility | Margin requirements may rise and collateral values may become less stable. | Funding needs can increase while risk appetite is already falling. |

| Collateral quality pressure | Assets used as collateral may be discounted, rejected, or harder to finance. | More cash or higher-quality collateral may be needed to support the same exposure. |

| Synchronized reactions | Liquidity demand becomes clustered rather than isolated. | Forced-flow pressure becomes more relevant to broader market structure. |

Margin Call vs Forced Liquidation vs Deleveraging

A margin call, forced liquidation, and deleveraging are connected, but they describe different parts of the pressure chain.

| Concept | What It Means | Where It Fits in the Sequence |

|---|---|---|

| Margin call | A demand to restore required equity, margin, or collateral. | The initial stress point after a threshold is breached. |

| Forced liquidation | The involuntary closing or sale of positions when requirements are not met or risk controls require action. | A possible outcome after the margin call, not the same thing as the call itself. |

| Deleveraging | The broader reduction of borrowed exposure, balance-sheet risk, or leveraged positioning. | The wider process that can emerge when many holders reduce exposure together. |

Deleveraging pressure becomes more important when margin calls do not stay isolated. A series of collateral demands can push holders to reduce risk, sell assets, repay financing, or shrink balance-sheet exposure across related markets.

How Margin Calls Can Feed Liquidity Pressure

Margin calls can create liquidity strain because they convert mark-to-market losses, collateral changes, or margin requirement changes into near-term funding needs. Affected holders may need cash when market liquidity is already less reliable.

The stress becomes more visible when asset sales are used to raise cash. If similar assets are sold into thin depth, prices can fall, collateral values can weaken further, and additional holders may face new shortfalls. That feedback channel connects margin calls with broader forced-flow conditions.

Limitation: The mechanism can amplify stress, but it does not automatically create a market decline. The outcome depends on available liquidity, collateral quality, risk controls, market depth, leverage concentration, and whether calls can be met without selling.

A Practical Failure-Mode Scenario

Volatility rises after a sharp repricing in a leveraged market segment. Several holders that use similar collateral face higher margin demands at roughly the same time. Some can post cash, but others reduce exposure because liquid resources are limited.

The first sales do not prove a systemic event. The stress becomes more important if market depth is weak, buyers step back, and the assets being sold are also used as collateral elsewhere. In that setting, lower prices can create new shortfalls, which can force additional holders to raise cash or reduce exposure.

The diagnostic sequence is collateral pressure becoming liquidity demand, liquidity demand becoming exposure reduction, and exposure reduction becoming feedback risk when leverage and crowding are high enough.

What Margin Calls Do Not Prove

Margin calls are useful for understanding stress inside leveraged systems, but they should not be treated as market predictions. The presence of margin calls does not prove that a crash, broad selloff, or systemic event is inevitable.

- They do not guarantee forced liquidation: A call can be met with cash, collateral, or position reduction before liquidation is required.

- They do not prove a market top: Margin stress is one part of a broader leverage and liquidity picture.

- They are not trade signals: They describe funding and collateral stress, not a direct buy or sell instruction.

- They do not affect all markets equally: The impact depends on where leverage, collateral dependence, and liquidity weakness are concentrated.

The strongest market-structure reading comes from combining margin-call stress with evidence of weak liquidity, crowded positioning, deteriorating collateral quality, higher volatility, and synchronized exposure reduction.

FAQ

What triggers a margin call?

A margin call is triggered when required equity, margin, or collateral falls below the required threshold. That can happen because of adverse price moves, higher margin requirements, weaker collateral value, or a combination of these pressures.

Do margin calls always cause forced selling?

No. A margin call can be met by adding cash, posting eligible collateral, or reducing exposure. Forced selling becomes more likely when the participant cannot restore the requirement or when risk controls require liquidation.

Why do margin calls matter during market stress?

They matter because many participants may need liquidity during the same stress window. If market depth is weak and exposures are crowded, attempts to raise cash or reduce positions can amplify stress.

How are margin calls connected to deleveraging?

Margin calls can contribute to deleveraging when participants reduce borrowed exposure to restore collateral or margin requirements. The connection becomes broader when many participants cut exposure together.