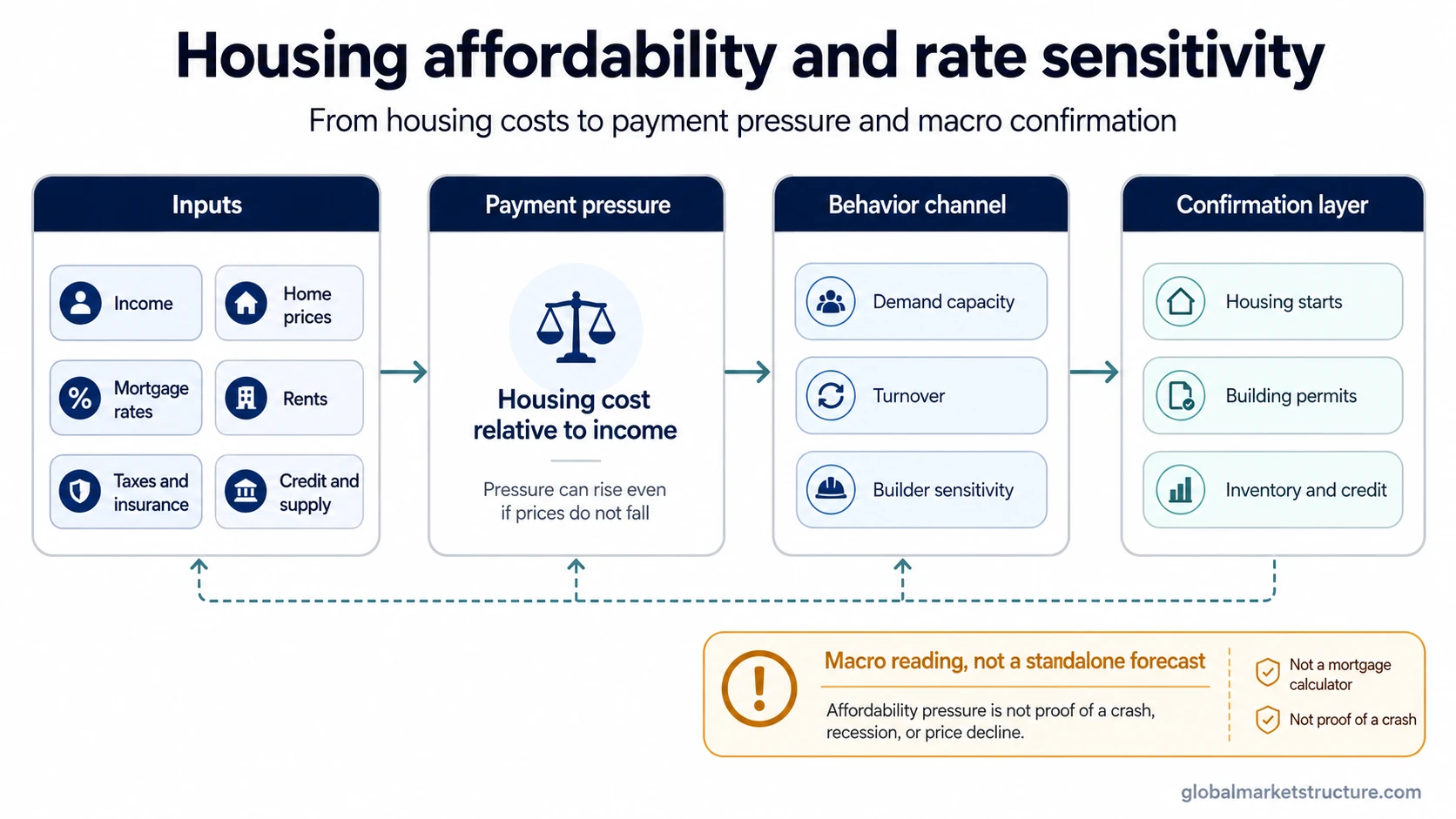

Housing affordability is the relationship between household income and the cost of renting or owning housing. In macro analysis, it works as a rate-sensitive payment-pressure gauge because mortgage rates, home prices, rents, taxes, insurance, and income growth shape how much housing demand households can sustain.

Affordability is not a mortgage calculator, a housing crash forecast, or a personal qualification test. It is a way to read pressure in the housing system: how difficult shelter costs become relative to income, and whether that pressure may begin to affect demand, turnover, construction, and broader growth sensitivity.

Key points

- Housing affordability compares income with the cost of renting or owning housing.

- It worsens when housing costs or financing costs rise faster than income.

- It matters because payment pressure can affect demand, turnover, construction activity, and rate sensitivity.

- It does not automatically prove recession risk, a housing crash, lower prices, or personal mortgage qualification.

What housing affordability means

Housing affordability describes how manageable shelter costs are relative to household income. For owners, the pressure can come from home prices, mortgage rates, down payments, taxes, insurance, maintenance, and credit access. For renters, the pressure comes mainly from rent levels, income growth, local supply, and household budget constraints.

The concept is useful because housing is both a household expense and a rate-sensitive part of the economy. When income rises faster than housing costs, households may absorb higher payments more easily. When housing costs rise faster than income, the same household income supports less demand, even if the desire for housing has not changed.

That makes affordability different from a simple price chart. A home price can be flat while affordability worsens if mortgage rates, taxes, or insurance rise. A home price can also rise while affordability holds up better if income growth is strong enough to offset part of the pressure.

What housing affordability measures

Affordability is usually built around the relationship between income and housing costs, but the exact components depend on the index, dataset, or framework being used. Some measures focus on ownership costs. Others include rent burden, local prices, median income, or financing assumptions.

For macro interpretation, the useful question is not only whether housing is expensive. The better question is which component is creating pressure and whether that pressure is likely to change behavior across households, builders, lenders, or local housing markets.

| Affordability component | What changes | Macro reading | Limitation |

|---|---|---|---|

| Income | Wages, employment income, and household earnings | Higher income can absorb higher housing costs | Income gains may be uneven or may lag prices |

| Home prices | Purchase price and required mortgage size | Higher prices can raise payment burden | Prices may stay high when supply is tight |

| Mortgage rates | Financing cost and monthly payment | Higher rates can reduce demand capacity | Rate effects depend on prices, income, credit, and inventory |

| Rents | Cost of shelter for non-owners | Rent pressure can show broader shelter stress | Rental markets vary by region and supply conditions |

| Taxes and insurance | Ownership carrying costs outside the mortgage payment | Rising non-mortgage costs can weaken affordability | These costs are often local and may not be captured equally by every index |

| Credit conditions | Borrowing availability and qualification pressure | Tighter credit can reinforce demand pressure | Affordability and credit access are related but not identical |

| Supply and inventory | Available homes and construction response | Tight supply can keep prices high despite weak affordability | Supply constraints can delay or distort price response |

Why housing affordability matters for macro and rates

Housing affordability matters for macro analysis because it connects interest rates to household behavior. When rates rise, a given home price usually becomes more expensive to finance. If income does not rise enough to offset that change, monthly payment pressure increases.

That pressure can reduce the number of households able or willing to transact at current prices. Buyers may delay purchases, sellers may avoid moving if their existing financing is cheaper, and turnover can weaken. Builders may then respond to weaker demand signals, financing costs, or inventory conditions.

The chain is not mechanical, but the logic is clear: rates and housing costs affect payment pressure, payment pressure can affect demand and turnover, and demand conditions can influence construction behavior. Affordability pressure becomes easier to interpret when it is checked against housing starts, because starts reflect current construction activity rather than household payment burden.

Building permits add a different layer because they point more toward future supply intent. If affordability weakens but permits remain resilient, the housing system may be absorbing pressure differently than if permits and starts both deteriorate.

Housing affordability is not a mortgage calculator

A mortgage calculator estimates what a household might afford under specific assumptions about income, debt, down payment, rate, taxes, insurance, and lender rules. Housing affordability, as a macro concept, is broader. It describes pressure across households and markets rather than giving one buyer a borrowing answer.

This distinction matters because the same affordability backdrop can affect households differently. A high-income household, a renter, a first-time buyer, a cash buyer, and a locked-in homeowner may experience the same market in different ways. Macro affordability does not decide whether one person should buy, sell, rent, wait, or qualify for a loan.

Affordability indexes can help organize the data, but they are still measurement tools. They do not replace local analysis, credit conditions, inventory data, or household-specific financial constraints.

What poor affordability can and cannot signal

Poor affordability can show that housing demand is becoming harder to sustain. It can also help explain why turnover slows, why some buyers step back, why sellers may stay locked into existing homes, or why builders become more sensitive to changes in demand and financing conditions.

Affordability pressure does not prove:

- a recession;

- a housing crash;

- lower home prices;

- a personal inability to buy;

- a direct market signal;

- a complete view of housing activity.

The limitation is supply. If available inventory is tight, weak affordability may reduce transactions without forcing prices lower quickly. If credit remains available and employment income holds up, household stress may build more slowly. If supply increases while demand is already weak, the same affordability pressure may matter more.

That is why affordability works best when it is checked against activity and supply data. Broader housing market indicators can help show whether payment pressure is spreading into activity, inventory, credit, or construction behavior.

A simple macro scenario

A common macro scenario is that mortgage rates rise while home prices remain high and income growth slows. Monthly payment pressure increases, so some buyers delay purchases and turnover weakens.

That does not prove a housing downturn by itself. The interpretation becomes stronger only if starts, permits, inventory, credit, and broader macro data confirm that affordability pressure is affecting real activity.

The same affordability reading can have different meanings depending on the surrounding conditions. Tight supply may keep prices firm even as transactions weaken. Strong income growth may soften the pressure from higher rates. Tighter credit can make the pressure more visible because fewer households can convert demand into completed purchases.

Related housing indicators

Housing affordability is best treated as the payment-pressure layer of the housing system. It shows how income, rates, prices, rents, taxes, insurance, and credit conditions interact, but it does not show the entire activity picture by itself.

Housing starts help confirm whether affordability pressure is affecting current construction activity. Building permits help show whether builders are changing future supply plans. Inventory, credit standards, builder confidence, and turnover data can add more context when the affordability signal is difficult to interpret on its own.

The practical macro reading is simple: housing affordability can identify pressure, but confirmation comes from activity, supply, credit, and broader growth data. The concept is strongest when it is used as part of a housing-rate sensitivity framework, not as a standalone forecast.