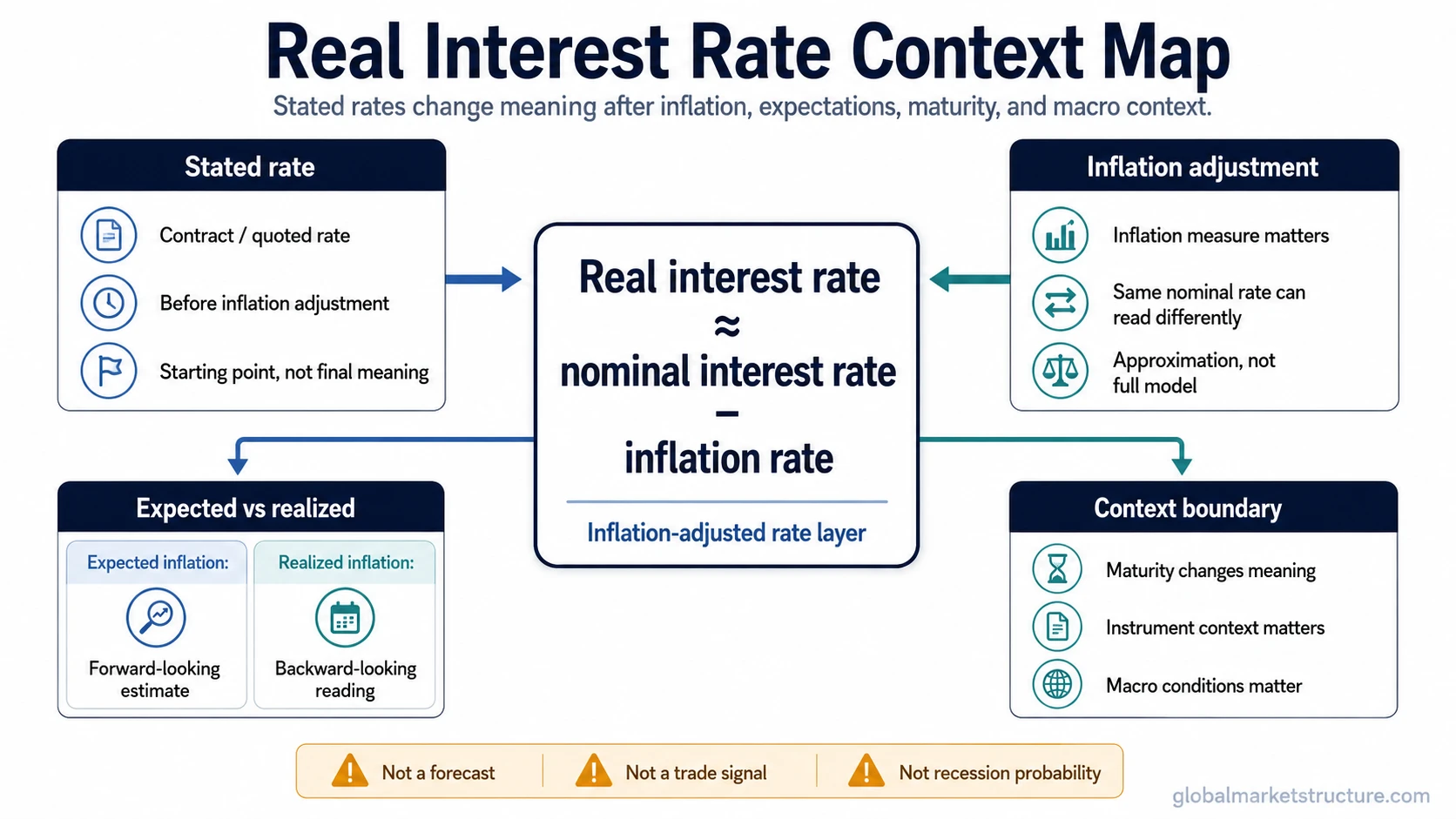

A real interest rate is an interest rate adjusted for inflation. A simple approximation is nominal interest rate minus inflation, but the meaning depends on which inflation measure is used, whether inflation is expected or already realized, and the macro context around the rate.

Definition: Real interest rate measures the purchasing-power value of an interest rate after inflation is taken into account. It helps show whether a stated rate is high or low in inflation-adjusted terms.

The concept is useful because a nominal rate alone does not show the full burden on borrowers or the full return to savers. A 6% nominal rate has a different meaning when inflation is 2% than when inflation is 7%.

A real interest rate is not a market forecast, recession signal, or trade signal by itself. It is one input for interpreting monetary conditions, borrowing costs, saving incentives, and the pressure that inflation places on stated rates.

Key Points

- Real interest rate adjusts a stated nominal rate for inflation.

- The simple approximation is nominal interest rate minus inflation rate.

- Expected inflation and realized inflation can produce different readings.

- The concept is useful for macro context, but it is not a standalone forecast or trade signal.

Real Interest Rate Formula

The simplified real interest rate formula is:

Real interest rate ≈ nominal interest rate − inflation rate

If a nominal interest rate is 6% and inflation is 3%, the approximate real interest rate is 3%. If inflation is 7%, the same 6% nominal rate is roughly -1% in real terms.

This simple formula is an approximation, not a full market model. The exact interpretation can change with compounding, the time period being measured, the inflation index being used, and whether the rate is backward-looking or based on expected inflation.

Nominal Interest Rate vs Real Interest Rate

A nominal interest rate is the stated rate before inflation adjustment. A real interest rate adjusts that stated rate for inflation, which makes it more useful for understanding purchasing power.

| Concept | What it shows | Why it matters |

|---|---|---|

| Nominal interest rate | The stated rate before inflation adjustment | Useful for contracts, quoted rates, and headline comparisons |

| Real interest rate | The inflation-adjusted value of the stated rate | Useful for purchasing-power, saving, borrowing, and macro interpretation |

The difference matters most when inflation is changing. A nominal rate can rise while the real interest rate falls if inflation rises faster than the stated rate. The opposite can also happen when inflation falls faster than nominal rates.

Why Expected and Realized Inflation Matter

Real interest rate interpretation changes depending on whether inflation is measured after the fact or estimated in advance. Realized inflation looks backward. Expected inflation looks forward.

A backward-looking calculation may show what the real burden was over a completed period. A forward-looking estimate tries to judge the inflation-adjusted burden that borrowers, savers, and policymakers may face in the future.

This distinction matters because financial markets often react to expectations before the realized data is fully known. If inflation expectations move sharply, the perceived real rate can change even before official inflation data confirms the shift.

How Real Interest Rates Fit Monetary Conditions

Real interest rates help connect inflation, nominal policy settings, and purchasing-power pressure. When real rates are higher, borrowing can become more restrictive in inflation-adjusted terms. When real rates are lower or negative, the real burden of borrowing may be lighter even if the nominal rate still looks high.

That interpretation is conditional. A higher real interest rate does not automatically mean risk assets must fall, and a lower real interest rate does not automatically mean financial conditions are easy. Growth expectations, credit spreads, liquidity, currency pressure, and market positioning can all change the broader signal.

In macro market-structure analysis, the real interest rate is best treated as a rates input. It helps frame whether nominal rates are restrictive or accommodative after inflation, but it needs surrounding evidence before it can support a broader regime interpretation.

Real Interest Rate vs Real Yields, Nominal Yields, Bond Yields, and Yield Curve

Real interest rate is often confused with nearby rates concepts. The overlap is understandable, but each term has a different role.

| Term | Main meaning | Common confusion |

|---|---|---|

| Real interest rate | An interest rate adjusted for inflation | Often treated as if the simple formula explains every market effect |

| Real yields | Market yield measures adjusted for inflation expectations or inflation-linked pricing context | Often used interchangeably with real interest rate even when the market instrument matters |

| Nominal yields | Yields quoted before inflation adjustment | Can look high or low without showing the inflation-adjusted burden |

| Bond yields | Broader bond-market return measures connected to price, maturity, coupon, and yield assumptions | Can be mistaken for a single interest-rate concept |

| Yield curve | The relationship between yields across different maturities | Can be confused with the level of one inflation-adjusted rate |

Yield-curve shape adds another layer. A change in real-rate interpretation can affect how investors read different maturities, but curve shape still depends on short-end policy expectations, long-end growth and inflation expectations, and term premium. That is why a curve-shape concept such as curve flattening should not be reduced to the real interest rate alone.

Simple Real Interest Rate Example

A nominal interest rate of 5% can feel restrictive when inflation is 1%, because the approximate real interest rate is 4%. The same 5% nominal rate can feel much less restrictive when inflation is 6%, because the approximate real interest rate is -1%.

The stated rate did not change in that example. The interpretation changed because inflation changed. That is the main reason real interest rate is useful in macro analysis: it shows how the purchasing-power meaning of the same nominal rate can shift across inflation environments.

The example is still incomplete without context. The maturity of the rate, the inflation measure, and the difference between expected and realized inflation can all change the final read.

Common Misuse of Real Interest Rate

The most common mistake is treating real interest rate as a complete market signal. A higher real rate can indicate more restrictive inflation-adjusted conditions, but it does not automatically determine the direction of equities, bonds, currencies, or credit markets.

Limitation: Real interest rate is a context variable, not a standalone forecast. It should be read alongside inflation expectations, growth expectations, liquidity, credit conditions, and the maturity or instrument being analyzed.

Another mistake is using one inflation measure as if it answers every question. Consumer inflation, expected inflation, realized inflation, and market-implied inflation compensation can point to different interpretations depending on the use case.

How to Read the Concept in Context

A clean reading starts with the nominal rate, subtracts the relevant inflation measure, and then asks what the result means for the specific context. A household loan, a central-bank setting, a Treasury yield, and a cross-asset regime discussion do not all use the concept in the same way.

For macro interpretation, the real interest rate becomes more useful when it is paired with other market-structure inputs. Inflation expectations, liquidity conditions, credit spreads, yield-curve behavior, and currency pressure can change whether a real-rate move feels restrictive, supportive, or ambiguous.

The useful boundary is simple: real interest rate explains the inflation-adjusted rate layer. It does not replace the broader rates, liquidity, and cross-asset framework needed to interpret market conditions.

FAQ

What is the real interest rate formula?

The simple approximation is real interest rate equals nominal interest rate minus inflation rate. The result can change depending on the inflation measure and time period used.

Is real interest rate the same as real yield?

Not always. Real interest rate is the broader inflation-adjusted rate concept, while real yield often refers to market yield measures tied to specific instruments or inflation-linked pricing context.

Does a high real interest rate predict market direction?

No. A high real interest rate can show more restrictive inflation-adjusted conditions, but market direction also depends on growth expectations, liquidity, credit conditions, positioning, and other macro inputs.