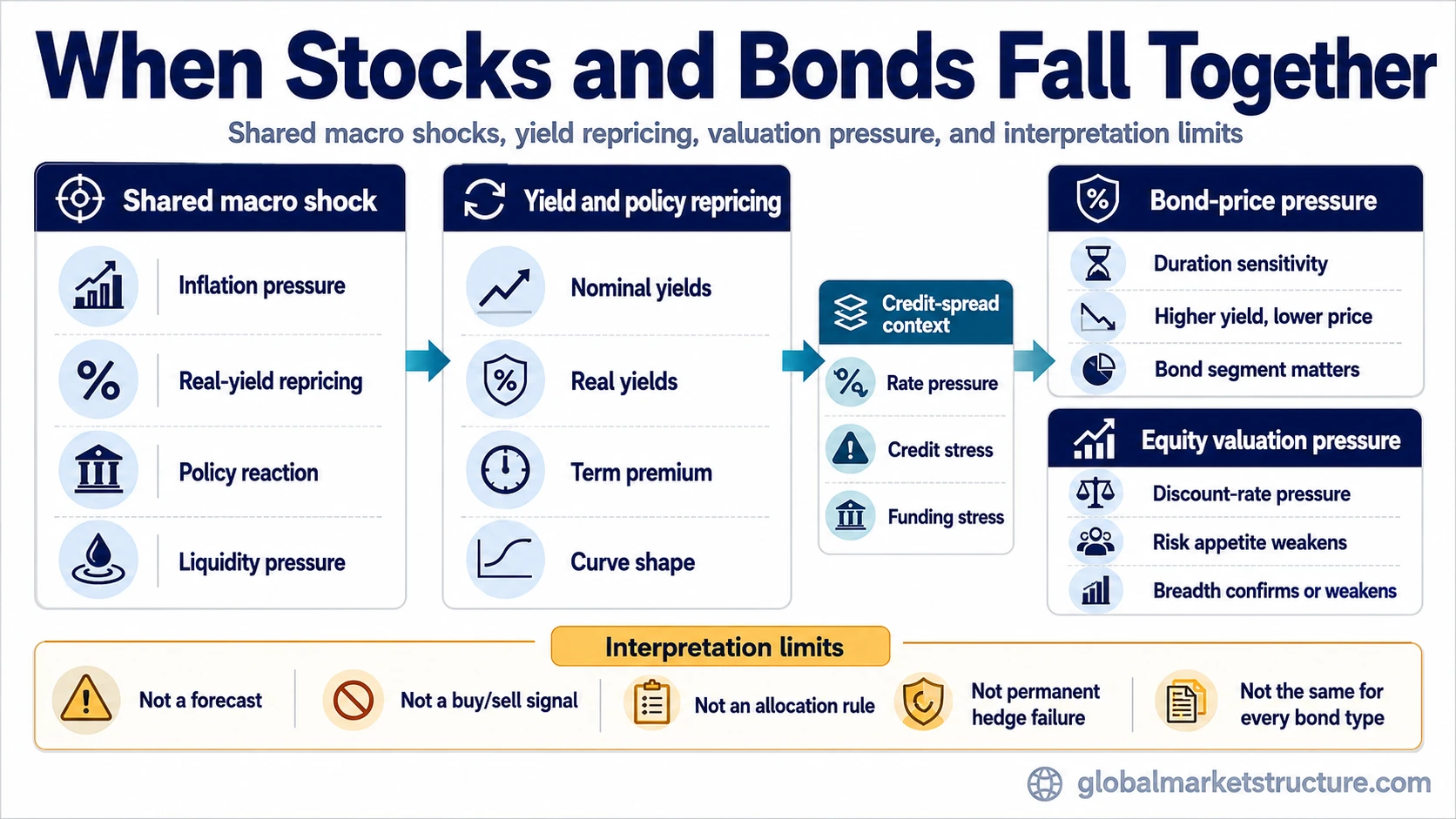

Stocks and bonds can fall together when the same macro shock pressures bond prices and equity valuations at the same time. The usual channels are inflation pressure, yield repricing, real-yield pressure, policy reaction, duration sensitivity, and weaker risk appetite. A joint decline is a co-movement condition, not a forecast, a buy/sell signal, or proof that bond diversification has permanently failed.

A falling stock market can coincide with falling bond prices when investors demand higher yields while also reducing the valuation they are willing to pay for future equity cash flows. The bond side is usually about price sensitivity to yields. The equity side is usually about discount rates, growth expectations, earnings-risk tolerance, and risk appetite.

Definition: Stocks and bonds fall together when equity prices and bond prices decline over the same measurement window. In return terms, that usually reflects a more positive stock-bond correlation episode, not a permanent rule about how the two asset classes must behave.

Condition, Implication, and Limit

The cleanest reading separates what is observable from what can be inferred. The same joint decline can come from inflation pressure, real-yield repricing, term-premium movement, credit stress, liquidity pressure, or a mix of several forces.

| Observable condition | Likely implication | Interpretation limit |

|---|---|---|

| Inflation expectations rise while equities weaken | Markets may be repricing higher policy pressure and weaker valuation support. | Inflation pressure alone does not prove a lasting correlation regime. |

| Real yields rise | Bond prices can fall while equity multiples face discount-rate pressure. | Real-yield pressure is not the same as broad credit stress. |

| Nominal yields rise | Bond prices can decline through duration sensitivity. | Nominal yields do not reveal whether inflation, real rates, term premium, or growth expectations are driving the move. |

| The yield curve steepens or flattens sharply | The market may be repricing the timing, location, or persistence of rate pressure. | Curve shape needs context; it is not a standalone explanation for equity weakness. |

| Term premium appears to rise | Longer-duration bonds may weaken as investors demand more compensation for holding maturity risk. | A term-premium reading is weaker when the move cannot be separated from real-rate, inflation, growth, or liquidity repricing. |

| Credit spreads widen alongside equity weakness | The move may include rising credit-risk compensation, not only rate pressure. | Credit-spread stress and rate-driven duration losses are different mechanisms. |

| Policy expectations reprice tighter | Bond yields may rise while equities adjust to higher discount rates and weaker liquidity expectations. | Policy repricing does not automatically identify the full cause of the decline. |

| Funding stress appears with cross-asset volatility | Both assets may weaken if participants are raising liquidity or reducing balance-sheet exposure. | Liquidity pressure should be checked against breadth, credit, currency, and funding indicators. |

Those conditions are more useful as a diagnostic set than as a ranking of causes. The interpretation improves when several signals point to the same shared shock and weakens when only one market segment is moving.

Why Stocks and Bonds Can Fall at the Same Time

A joint stock-bond decline usually reflects a shared shock rather than two unrelated moves. If inflation pressure rises, investors may expect tighter policy or higher real yields. Bond prices can fall as yields rise, while equity valuations can compress because future cash flows are discounted at a higher rate.

The bond market side depends heavily on duration. Longer-duration bonds are usually more sensitive to changes in yields because more of their cash-flow value sits farther in the future. Shorter-duration instruments may react differently, and credit-sensitive bonds may reflect a separate spread component.

The equity side is not only about higher yields. Equities can weaken when higher real yields reduce valuation support, when policy expectations tighten, when inflation threatens margins, or when risk appetite falls.

The strongest interpretation usually appears when several lenses point in the same direction: yields rise, real rates rise, policy expectations tighten, credit spreads stop behaving calmly, volatility rises, and equity breadth weakens. A single yield move is a weaker basis for interpretation.

Real Yields, Nominal Yields, and Duration Pressure

Nominal yields describe the yield investors observe before separating inflation effects. Real yields adjust that yield for inflation expectations. This distinction matters because equities can react differently to a nominal-yield move driven by stronger growth than to a real-yield move driven by tighter financial conditions.

When real yields rise, the pressure can become more direct for both assets. Bonds face price weakness as yields rise. Equity valuations can face pressure because the discount-rate baseline becomes less supportive. The reading becomes less clear if nominal yields rise mainly because growth expectations are improving and credit conditions remain stable.

Duration adds the bond-side sensitivity layer. Longer-duration exposure tends to move more for a given yield change than shorter-duration exposure. That is why a joint decline in stocks and one bond segment does not prove that every bond exposure is behaving the same way.

Stronger and Weaker Readings

A joint decline deserves more attention when it is broad, persistent, and supported by several cross-asset signals. It deserves less weight when it is narrow, temporary, or isolated inside one bond segment.

| Reading quality | What to check | Why it matters |

|---|---|---|

| Stronger | Stocks fall while yields and real yields rise. | Both assets may be reacting to tighter discount-rate pressure. |

| Stronger | Credit spreads widen at the same time. | The move may include rising risk compensation, not only duration pressure. |

| Stronger | Equity breadth weakens and volatility rises. | The decline may be broadening across risk assets rather than remaining isolated. |

| Stronger | The correlation window extends beyond a short event reaction. | Persistent co-movement carries more regime information than a one-day shock. |

| Weaker | Only long-duration bonds are weak while credit spreads remain calm. | The move may be mostly rate-duration pressure rather than broad risk stress. |

| Weaker | The move reverses quickly after a policy headline. | A temporary event reaction may not define a broader correlation regime. |

| Weaker | One bond segment falls while others remain stable. | Bond behavior is not uniform across maturity, credit, inflation-linked, and cash-like exposures. |

| Weaker | Equity weakness is narrow or sector-specific. | The stock-side move may reflect valuation or earnings risk in one area rather than a full cross-asset regime shift. |

Common False Readings

Not permanent hedge failure: A period where stocks and bonds decline together does not prove that bonds have permanently stopped diversifying equity risk. Correlation can change with inflation pressure, policy expectations, growth shocks, liquidity conditions, and the measurement window.

Not a yield-only story: Higher yields can explain part of the move, but not always the full move. Real yields, inflation expectations, curve shape, term premium, credit spreads, volatility, and liquidity conditions can all change the interpretation.

Not one bond behavior: Long-duration bonds, short-duration bonds, credit-sensitive bonds, inflation-linked bonds, and cash-like instruments can respond differently. A joint decline between equities and one bond exposure should not be generalized across the entire bond universe.

Not a market signal: Positive co-movement between stocks and bonds does not create a forecast, trade instruction, allocation rule, or automatic risk-off conclusion. It is an observed relationship that needs macro and cross-asset context.

Example of a Joint Stock-Bond Decline Reading

A common scenario is that equities fall while government bond prices also decline. The tempting interpretation is that diversification has failed. The cleaner reading starts by separating the channels: yields are rising, real yields are rising, the curve is moving, and investors are reassessing policy pressure.

The case becomes more convincing if credit spreads widen, volatility rises, equity breadth weakens, and the move persists beyond a short headline reaction. The case remains unresolved if the decline is confined to long-duration bonds, credit markets stay calm, and equities are weakening only in rate-sensitive segments.

The practical distinction is between observed co-movement and causal proof. Stocks and bonds falling together can signal a shared macro repricing, but the cause still has to be checked through yields, inflation expectations, credit, duration, policy reaction, liquidity, and the chosen correlation window.

Relationship to Stock-Bond Correlation

A joint decline is one possible expression of stock-bond correlation. The broader relationship also includes periods when equities rise while bonds fall, bonds rise while equities fall, both rise together, or the relationship becomes unstable across different time windows.

The key distinction is that correlation measures co-movement, while interpretation asks why that co-movement is occurring. A positive correlation window may come from inflation pressure, policy repricing, liquidity stress, or a temporary event reaction. The same reading can weaken once the measurement window changes.

For market-structure analysis, the joint decline is a condition to diagnose. The stronger question is whether surrounding signals point to inflation pressure, real-yield repricing, term-premium pressure, credit stress, liquidity demand, or only a short-lived correlation window.

FAQ

Why do stocks and bonds fall together?

Stocks and bonds can fall together when the same macro shock pressures both assets. Rising yields can reduce bond prices, while higher real yields, tighter policy expectations, inflation pressure, or weaker risk appetite can pressure equity valuations.

Does a joint stock-bond decline mean diversification is broken?

No. A joint decline can weaken diversification during a specific window, but it does not prove permanent hedge failure. Correlation regimes can shift with inflation, policy expectations, growth shocks, liquidity conditions, and the measurement period.

Are all bonds affected the same way when stocks fall?

No. Bond behavior depends on maturity, duration, credit exposure, inflation sensitivity, liquidity, and the source of the shock. Long-duration bonds can react differently from short-duration or credit-sensitive exposures.

Is a joint stock-bond decline a market forecast?

No. A joint decline is an observed co-movement condition. It can help diagnose the market environment, but it does not create a forecast, buy/sell signal, or allocation rule by itself.