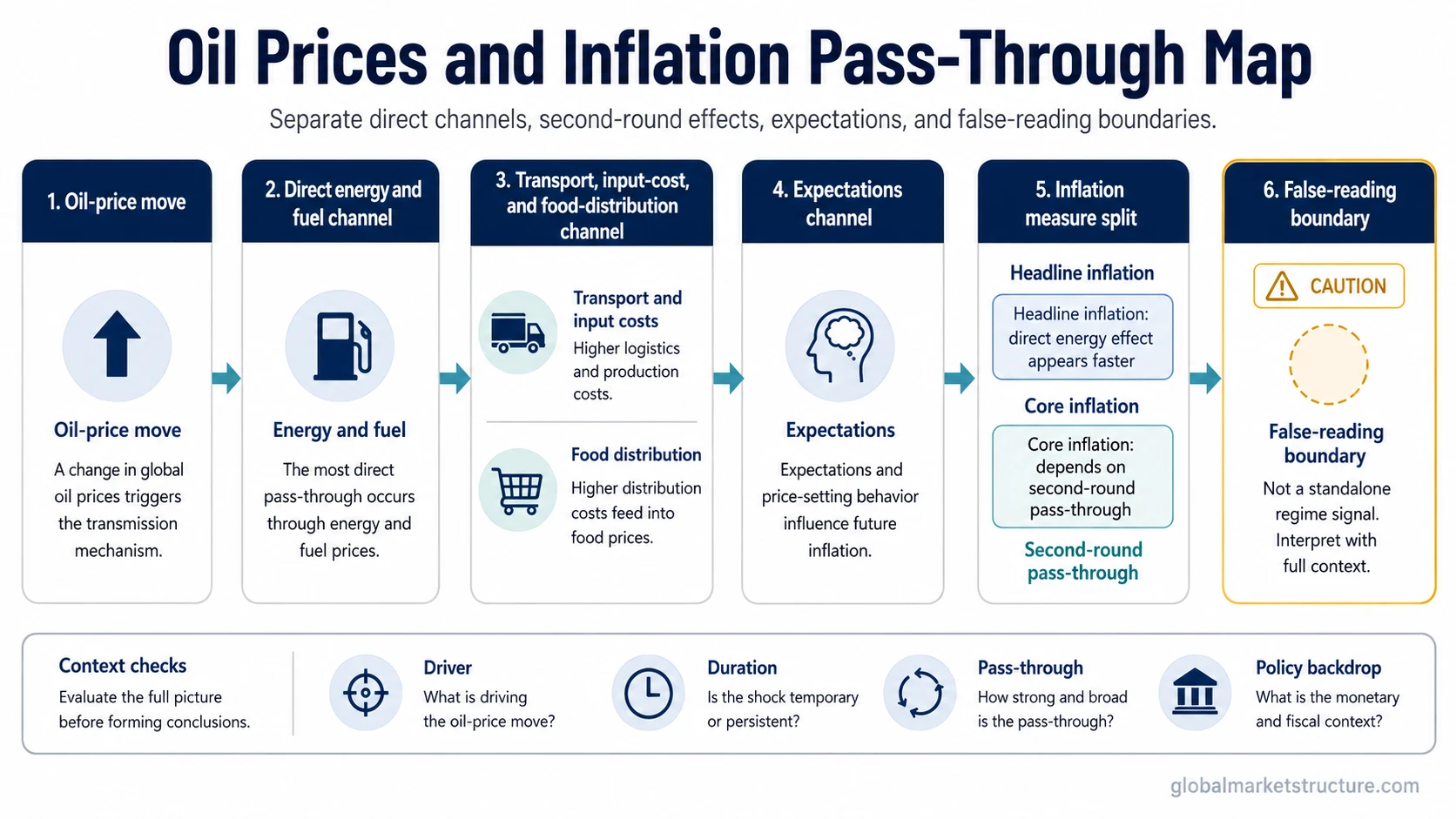

Oil prices can affect inflation through energy, fuel, transportation, production, food-cost, and expectations channels. The clearest short-term effect usually appears in headline inflation because energy is included directly. Core inflation depends more on whether energy costs spread into broader prices, wages, and expectations. Oil is one inflation channel, not a complete inflation-regime signal by itself.

- Oil usually affects headline inflation before it affects broader inflation measures.

- Core inflation depends more on second-round pass-through into prices, wages, and expectations.

- The same oil move can reflect demand, supply pressure, currency effects, geopolitical risk, or broader commodity pressure.

- The inflation reading is stronger when driver, duration, pass-through, expectations, and policy context align.

How Oil Prices Feed Into Inflation

Oil prices affect inflation most directly through energy products that consumers and businesses pay for. Gasoline, diesel, heating fuel, jet fuel, shipping, and distribution costs can move quickly when crude or refined-product prices change.

The indirect channel is slower. Higher energy costs can raise production, transportation, packaging, and food distribution costs. That pressure becomes more important for broader inflation when firms can pass those costs through and when households, workers, or businesses begin adjusting expectations.

The driver matters. An oil-price increase caused by strong demand can carry a different macro message than an oil-price increase caused by supply disruption. A falling oil price can ease headline pressure, but it does not automatically mean underlying inflation pressure has disappeared.

Headline Inflation Usually Reacts First

Headline inflation includes energy prices, so oil-related moves can show up quickly when fuel and energy costs change. That is why oil often has a visible short-term effect on reported inflation readings.

Core inflation usually excludes volatile food and energy components, but that does not make oil irrelevant. The connection is more conditional. Oil becomes more relevant to core inflation when higher energy costs spread into transportation, goods prices, services pricing, wages, or inflation expectations.

The practical distinction is simple: headline inflation captures the direct energy effect faster, while core inflation asks whether the oil move is spreading beyond energy itself.

When Oil Prices Become a Stronger Inflation Signal

An oil move becomes more useful for inflation interpretation when it lasts long enough to affect pricing behavior and when related channels confirm the pressure. A short-lived move can change a monthly reading without changing the broader inflation path.

| Condition | Why It Matters | Inflation Reading |

|---|---|---|

| Sustained oil move | Temporary moves fade more easily. | Stronger if the move persists long enough to affect pricing behavior. |

| Refined-product pass-through | Consumer fuel costs depend on more than crude oil alone. | Stronger when gasoline, diesel, or heating fuel move with crude. |

| Transport and food-cost spillover | Energy can affect shipping, logistics, farming, and distribution. | Stronger when pressure reaches broader goods or food-cost channels. |

| Inflation expectations | Expectations can affect wage demands and pricing behavior. | Stronger when households and firms treat the move as persistent. |

| Wage and pricing behavior | Second-round effects matter more than the first energy move. | Stronger when firms pass costs through and workers seek compensation. |

| Policy backdrop | Policy reaction differs between temporary energy volatility and broad inflation. | Stronger when oil pressure complicates real income, growth, or policy expectations. |

| Demand vs supply driver | The reason for the oil move changes its macro meaning. | Demand-led strength can signal activity pressure; supply-led strength can act like a cost shock. |

Oil Can Be Cause, Symptom, or Common-Shock Marker

Oil is sometimes a direct inflation cause because it raises energy and transport costs. It can also be a symptom of a stronger demand environment, where activity, wages, commodities, and pricing power are already firm. In other cases, oil and inflation move together because both are reacting to a broader shock, such as supply disruption, currency weakness, or wider commodity pressure.

The inflation question is not only whether oil moved. It is whether oil is the direct driver, a response to stronger demand, or one part of a broader shock affecting commodities, currency, supply chains, or expectations.

This distinction prevents a common false reading. A higher oil price does not automatically prove that oil is the main reason inflation is rising. A lower oil price does not automatically prove that inflation pressure is over. The reading is stronger when driver, duration, pass-through, expectations, and policy context point in the same direction.

Where the Oil-Inflation Reading Can Mislead

A standalone oil move is a weak inflation signal. A sharp oil increase can be temporary, supply-specific, or offset by weaker demand elsewhere. A sharp oil decline can reduce headline inflation while services inflation, wages, rents, or expectations remain sticky.

A safer reading separates the observed oil move from the interpretation. The observed fact is the price change. The interpretation depends on whether that move reaches consumer fuel costs, business input costs, expectations, and policy reaction.

Oil Prices vs Oil Shock

A normal oil-price move is not automatically an oil shock. Oil prices can rise or fall without becoming a broad macro event.

An oil shock is a stronger classification. It implies that the oil move is large or disruptive enough to affect inflation, growth, supply conditions, real income, policy expectations, or market risk conditions. The boundary is not the direction of oil alone. The boundary is whether the move changes the broader macro environment.

How to Interpret Oil Prices in an Inflation Framework

Start with the driver of the oil move, then test the pass-through channel. A demand-led increase, a supply-led increase, and a currency-led increase can all raise oil prices, but they do not carry the same inflation meaning.

Next, separate headline inflation from broader inflation pressure. Direct energy effects can move headline inflation quickly. Broader inflation pressure requires evidence that energy costs are spreading into other prices, expectations, wages, or policy reaction.

Finally, compare oil with related inflation signals rather than treating it as a standalone answer. Oil is more useful when it agrees with other commodity pressure, expectations, wage behavior, and policy constraints. It is less useful when it moves alone or when the driver is temporary.

Related Concepts

Use the broader inflation framework for price-level interpretation, the expectations channel for second-round effects, and the oil-shock framework when an energy move becomes large enough to affect the wider macro environment.