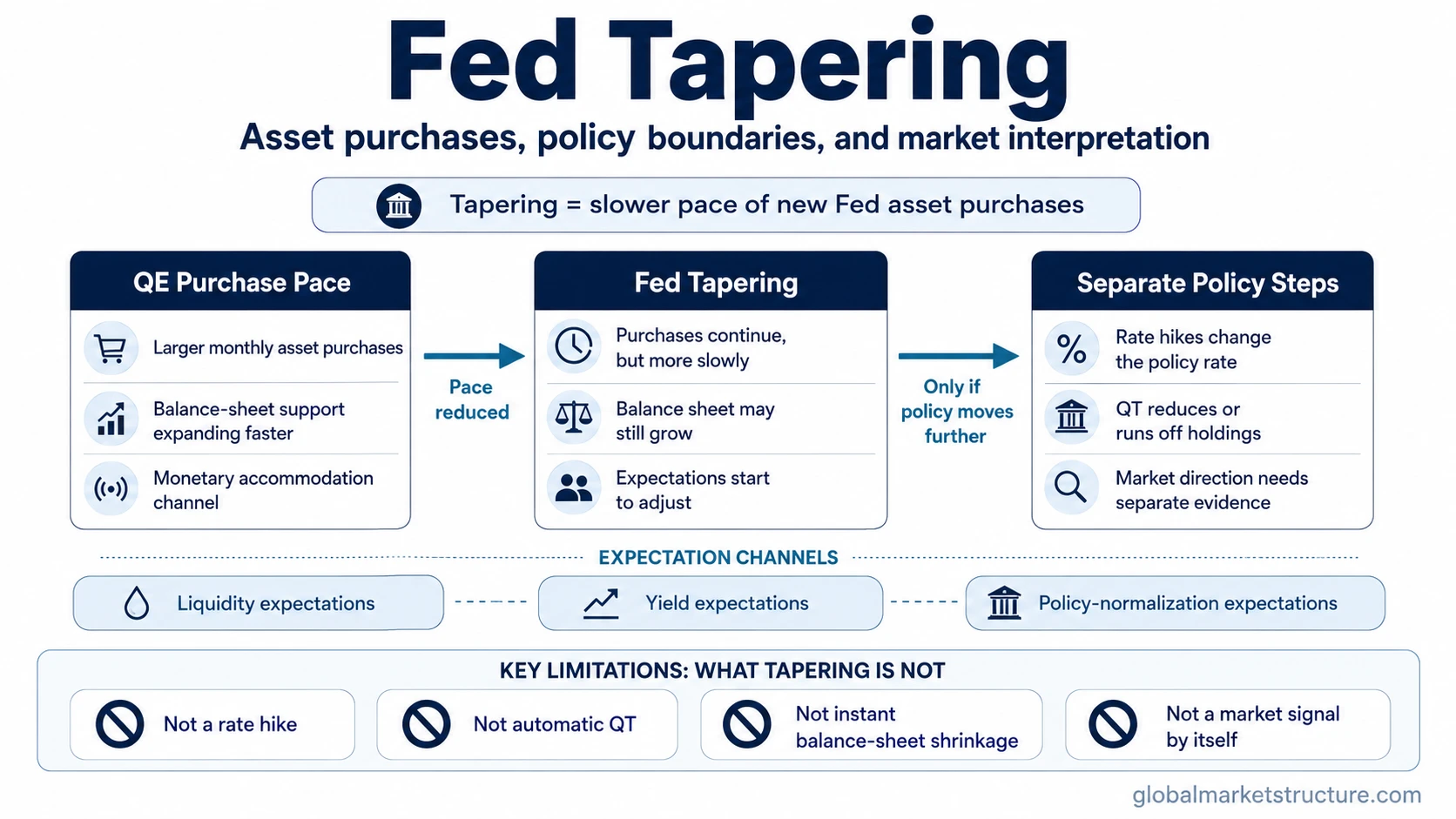

Fed tapering means the Federal Reserve is slowing the pace of asset purchases, usually after a period of quantitative easing. It can slow the growth of the Fed balance sheet and affect expectations for liquidity, yields, and future policy, but it is not automatically a rate hike, quantitative tightening, balance-sheet shrinkage, or a market-direction signal.

Definition: Fed tapering is a reduction in the pace of Federal Reserve asset purchases. The Fed may still be buying assets, but it is buying less than before.

Core boundary: tapering changes the speed of new purchases. It does not automatically reduce the existing balance sheet, raise the federal funds rate, or predict how stocks, bonds, credit, or the dollar will move.

Key Points

- Fed tapering usually follows QE because it reduces the monthly pace of asset purchases.

- The Fed balance sheet can still grow during tapering if purchases remain positive.

- Tapering differs from rate hikes because it concerns asset purchases, not the policy rate.

- Tapering differs from quantitative tightening because QT involves balance-sheet runoff or reduction.

How Fed Tapering Works

Fed tapering works through the purchase schedule. Under QE, the Federal Reserve buys assets such as Treasury securities or agency mortgage-backed securities to add monetary accommodation. When the Fed tapers, it reduces the pace of those purchases over time instead of stopping all policy support at once.

The balance-sheet distinction matters. If the Fed is still buying assets, the central-bank balance sheet may continue to expand, but at a slower rate. Balance-sheet shrinkage requires a different step, such as allowing assets to mature without full reinvestment or actively reducing holdings.

Markets pay attention because tapering can change expectations. A slower purchase pace can affect how investors think about liquidity support, long-term yields, future policy normalization, and risk appetite. Those effects are conditional. The same tapering language can be interpreted differently depending on inflation, growth, credit conditions, market liquidity, and the expected path of interest rates.

Fed Tapering vs Related Policy Terms

Fed tapering is easiest to interpret when it is separated from nearby policy terms. The confusion usually comes from treating every reduction in support as the same action.

| Policy term | What changes | What it does not mean by itself |

|---|---|---|

| Quantitative easing | The Fed buys assets to add monetary accommodation. | It does not guarantee stronger growth, higher asset prices, or lower volatility. |

| Fed tapering | The Fed slows the pace of asset purchases. | It does not automatically mean rate hikes, balance-sheet shrinkage, or a market selloff. |

| Rate hike | The Fed raises its policy-rate target. | It is not the same as changing the asset-purchase schedule. |

| Quantitative tightening | The Fed allows holdings to run off or reduces the balance sheet. | It is not the same as merely slowing new purchases. |

Why Tapering Affects Expectations

Tapering can affect markets because asset purchases influence expectations about liquidity support and policy direction. A slower purchase pace may lead investors to reassess how much support remains in the system and how quickly policy could normalize later.

The expectation channel is different from a mechanical market signal. Tapering may matter more when investors were expecting continued accommodation, when inflation pressure is changing the policy path, or when yields and credit conditions are already sensitive to policy shifts.

It may matter less when the change is widely expected, gradual, and already reflected in yields, positioning, and risk assets. The interpretation depends on the broader macro regime, not on the word “tapering” alone.

Fed Tapering and the Balance Sheet

The Fed balance sheet does not automatically shrink during tapering. If the Fed reduces monthly purchases from a higher amount to a lower amount, it is still adding assets as long as purchases remain positive.

Simple distinction: tapering slows the rate of balance-sheet expansion. Quantitative tightening changes the direction of the balance-sheet process by reducing holdings or allowing them to run off without full replacement.

This is why tapering can be described as a bridge between full QE and later policy normalization. It may come before rate hikes or QT, but it does not automatically cause either one.

Fed Tapering vs Taper Tantrum

Fed tapering is the policy action. A taper tantrum is a market reaction to the possibility or announcement of reduced asset purchases. The two terms should not be treated as interchangeable.

A taper tantrum can involve sudden changes in yields, risk appetite, or positioning, but that reaction depends on expectations, communication, inflation conditions, and investor positioning. Tapering itself only describes the reduced pace of purchases.

Common Misreadings of Fed Tapering

A common mistake is to treat tapering as an immediate tightening event in every market. The policy is less accommodative than full QE, but the Fed may still be adding support if purchases continue.

Another mistake is to assume tapering automatically predicts the direction of stocks, bonds, the dollar, or credit spreads. Markets respond to the full policy mix, the inflation and growth backdrop, liquidity conditions, valuation, positioning, and how much of the change was already priced in.

A third mistake is to treat tapering as the same as QT. Quantitative tightening is a separate balance-sheet process. Tapering comes earlier in the sequence because it slows new purchases before a later runoff or reduction phase can begin.

Example Scenario

Suppose the Fed has been buying assets each month under QE and later announces that future monthly purchases will be smaller. Policy support has not disappeared, but the pace of new support has been reduced.

If purchases continue, the balance sheet can still expand. If purchases end and holdings later begin to mature without full replacement, the policy has moved beyond tapering into a different balance-sheet phase.

How to Read Fed Tapering Language

Fed tapering language often focuses on pace. Phrases such as “reduce the pace of purchases,” “slow asset purchases,” “lower monthly purchases,” or “wind down purchases over time” usually point to tapering rather than immediate balance-sheet reduction.

The surrounding message changes the interpretation. A tapering announcement paired with cautious language may signal gradual normalization. A faster tapering path paired with inflation concern may shift expectations toward tighter policy later. The taper itself is one part of the policy signal, not the entire signal.

FAQ

What is Fed tapering?

Fed tapering is the Federal Reserve slowing the pace of asset purchases, usually after quantitative easing. The Fed may still be buying assets, but at a lower monthly pace.

Is Fed tapering the same as raising interest rates?

No. Fed tapering concerns asset purchases. Raising interest rates changes the policy-rate target. The two can be related in expectations, but they are different policy actions.

Does Fed tapering shrink the Fed balance sheet?

Not automatically. If the Fed is still buying assets, the balance sheet can keep growing at a slower rate. Shrinkage requires runoff or reduction in holdings.

Is Fed tapering the same as quantitative tightening?

No. Tapering slows new asset purchases. Quantitative tightening reduces or runs off the balance sheet after purchases have ended or after reinvestment policy changes.

Does Fed tapering predict market direction?

No. Fed tapering can affect expectations for liquidity, yields, and future policy, but market direction depends on broader conditions and how much of the taper was already expected.