A crowded trade is a market condition where many participants hold similar positions, exposures, or strategies. The risk is not popularity by itself, but concentration relative to liquidity and exit capacity. A crowded trade can become fragile if many holders try to reduce exposure at the same time, but crowding alone does not predict a reversal.

Definition: A crowded trade means similar market exposure is held by a large number of participants, or by participants large enough to matter for liquidity. The exposure may be a direct position, a factor bet, a strategy, a sector preference, a macro theme, or a consensus risk allocation.

Boundary: Crowded does not automatically mean wrong, bearish, overvalued, or near a turning point. It means the position may become more sensitive to liquidity, flows, catalysts, and exit pressure.

Key Points

- A crowded trade is about concentration of exposure, not only about opinion or popularity.

- The main structural risk is that exit demand can become large relative to available liquidity.

- Crowded trades can keep working when flows, trend, fundamentals, policy, or liquidity still support them.

- Crowding becomes more fragile when many holders react to the same catalyst or risk-control trigger.

- A crowded trade is not a buy signal, sell signal, or complete market forecast.

Why crowded trades matter

Crowded trades matter because market prices are affected not only by views, but also by how much exposure already exists and how easily that exposure can be changed. When many participants are positioned the same way, the next stage depends on whether liquidity can absorb new buying, selling, hedging, or de-risking without large price impact.

The pressure is conditional. If liquidity is deep, holders are patient, and new buyers continue to absorb supply, a crowded exposure can remain stable. If liquidity thins or a catalyst forces many participants to adjust together, the same exposure can become more unstable.

The useful question is not simply whether a trade is popular. The better question is whether the size and similarity of the exposure have become large relative to the market’s ability to absorb exits.

How a trade becomes crowded

A trade can become crowded when different participants reach similar conclusions, use similar models, follow similar benchmarks, or respond to the same performance pressure. The crowding may be visible in direct positioning data, but it can also appear through correlated behavior across strategies and assets.

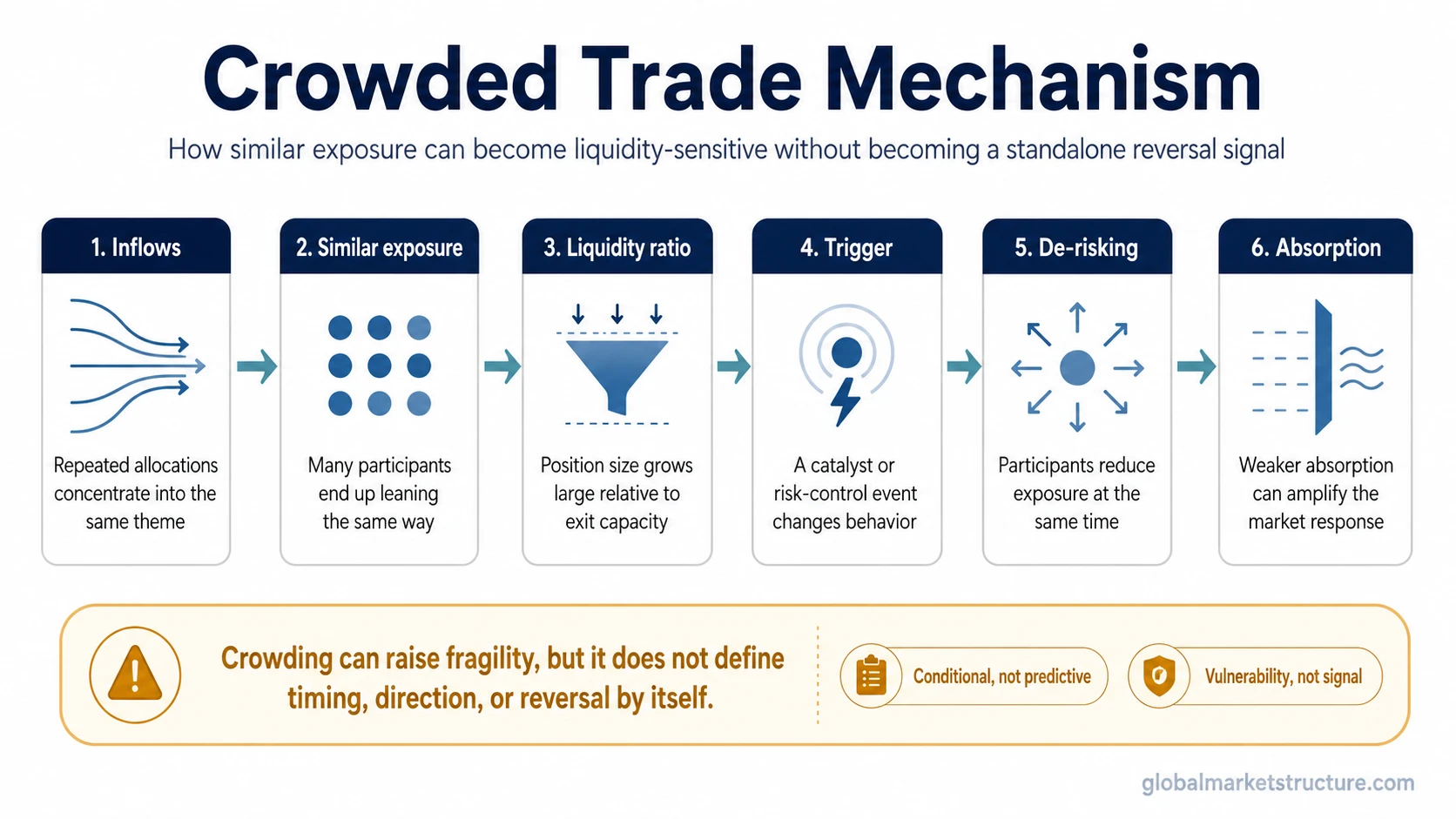

Common crowding path:

- A theme, factor, asset, or strategy attracts repeated inflows.

- Many participants build similar exposure.

- The exposure becomes large relative to normal liquidity or exit capacity.

- A catalyst, risk limit, funding pressure, or volatility shock forces adjustment.

- Many holders try to reduce similar exposure in the same window.

- Market absorption weakens, so price response can become nonlinear.

- The interpretation remains conditional because crowding alone does not define direction or timing.

Crowding can come from trend following, benchmark pressure, leverage, volatility targeting, macro consensus, factor concentration, sector leadership, or narrative agreement. None of those inputs proves that an unwind must happen. They only help explain why the exposure may become more sensitive if conditions change.

Crowded trade vs market sentiment vs contrarian signal

A crowded trade is often confused with market sentiment, but the two are not identical. Sentiment describes the broad mood or expectation set. Crowding describes the concentration of actual or implied exposure.

| Concept | What it describes | Main risk of misreading it |

|---|---|---|

| Crowded trade | Many participants hold similar exposure, or exposure is large relative to liquidity and exit capacity. | Assuming crowding automatically means reversal. |

| Market sentiment | The broader mood, confidence, or expectation set across investors and traders. | Confusing opinion with actual positioning. |

| Sentiment extreme | An unusually stretched optimism or pessimism condition. | Assuming stretched sentiment must immediately unwind. |

| Contrarian signal | An interpretation that one-sided sentiment or positioning may create risk in the opposite direction. | Treating the signal as automatic rather than conditional. |

| Positioning framework | A broader evidence structure for comparing positioning, flows, liquidity, and market context. | Relying on one crowding clue instead of a broader evidence set. |

The distinction matters because a crowded exposure can exist even when public sentiment is mixed. The opposite can also happen: sentiment can look extreme while actual position concentration is less clear.

What can make crowded trades fragile

A crowded trade becomes more fragile when the same-side exposure is large and the market has limited ability to absorb exits. Fragility does not require every holder to sell. It can appear when a small but important group needs to reduce risk quickly and other participants are unwilling to absorb the flow at previous prices.

| Fragility driver | How it can affect the trade | Important limitation |

|---|---|---|

| Thin liquidity | Orders have more price impact because less depth is available. | Liquidity can vary by time, asset, venue, and volatility regime. |

| Same-side de-risking | Many participants try to reduce similar exposure at the same time. | Not all holders have the same horizon, leverage, or risk constraints. |

| Funding or margin pressure | Leveraged holders may need to cut exposure even if their long-term view has not changed. | Funding pressure must be supported by evidence before being claimed in a real case. |

| Hedging flows | Risk management activity can reinforce price moves during stress. | The effect depends on positioning, instruments, and market depth. |

| Weaker marginal demand | New buyers or absorbers become less responsive after a crowded move. | Demand can return if liquidity, valuation, policy, or fundamentals improve. |

What a crowded trade does not tell you

A crowded trade does not tell you exact timing, direction, or outcome. It does not identify who is trapped. It does not prove that buyers are gone. It does not show whether the next move must be higher or lower.

The same crowded exposure can produce different outcomes under different conditions. If liquidity stays supportive and flows continue, crowding can persist. If liquidity weakens and many participants need to reduce risk together, the same condition can become more unstable.

A cleaner interpretation is to treat crowding as a vulnerability condition. It can raise sensitivity to catalysts and liquidity shocks, but it should not be treated as a standalone contrarian signal.

Simple illustrative scenario

Imagine a broad market theme attracts steady inflows for several months. Managers, systematic strategies, and discretionary investors all build similar exposure because the theme keeps performing. While liquidity is strong, the trade can continue even though it is crowded.

The risk changes if volatility rises, liquidity thins, and some holders must reduce exposure at the same time. The sequence moves from inflow to concentration, then from thinner liquidity to simultaneous de-risking and weaker absorption. In that situation, the issue is not that the original idea was automatically wrong. The issue is that similar positioning can create exit pressure faster than the market can absorb it.

This is an illustrative scenario, not a historical claim. It shows why crowding should be read through liquidity, flows, and exit capacity rather than through a simple reversal assumption.

How to interpret crowding without turning it into a signal

Crowding is most useful when it is treated as one input inside a broader positioning and liquidity review. A stronger interpretation usually separates four questions:

- Exposure: Are many participants positioned in a similar way?

- Liquidity: Is the exposure large relative to normal market depth and exit capacity?

- Trigger: Is there a catalyst, risk limit, funding pressure, or volatility shift that could force adjustment?

- Absorption: Are other participants still willing and able to take the other side?

That structure keeps the concept from becoming a shortcut. A crowded trade may be resilient, vulnerable, or irrelevant depending on the surrounding evidence.

Related positioning concepts

Crowding becomes clearer when exposure concentration is separated from mood, contrarian interpretation, and the broader evidence set. A positioning dashboard framework can organize crowding evidence alongside flows, liquidity, sentiment, and risk conditions.

The core distinction is simple: sentiment describes what participants broadly think or feel, while crowded positioning describes how much similar exposure may already exist. A contrarian reading may use that information, but it should remain conditional rather than automatic.

FAQ

Does a crowded trade always reverse?

No. A crowded trade can keep working if liquidity, flows, trend, fundamentals, or policy conditions still support the exposure. Crowding raises sensitivity to exits and catalysts, but it does not define timing or direction by itself.

Is a crowded trade the same as market sentiment?

No. Market sentiment is the broader mood or expectation set. A crowded trade is about concentration of similar exposure. Sentiment can be positive without positioning being highly concentrated, and positioning can be crowded even when public sentiment is mixed.

Why can crowded trades unwind quickly?

They can unwind quickly when many holders need to reduce similar exposure during a period of weaker liquidity. The move can become sharper if other participants are not willing or able to absorb the flow at previous prices.

Can crowding be a false signal?

Yes. Crowding can look risky too early, especially when the underlying trend remains supported by liquidity, flows, earnings, policy, or macro conditions. A crowding signal is weak if it is not connected to exit pressure, liquidity, and a plausible catalyst.