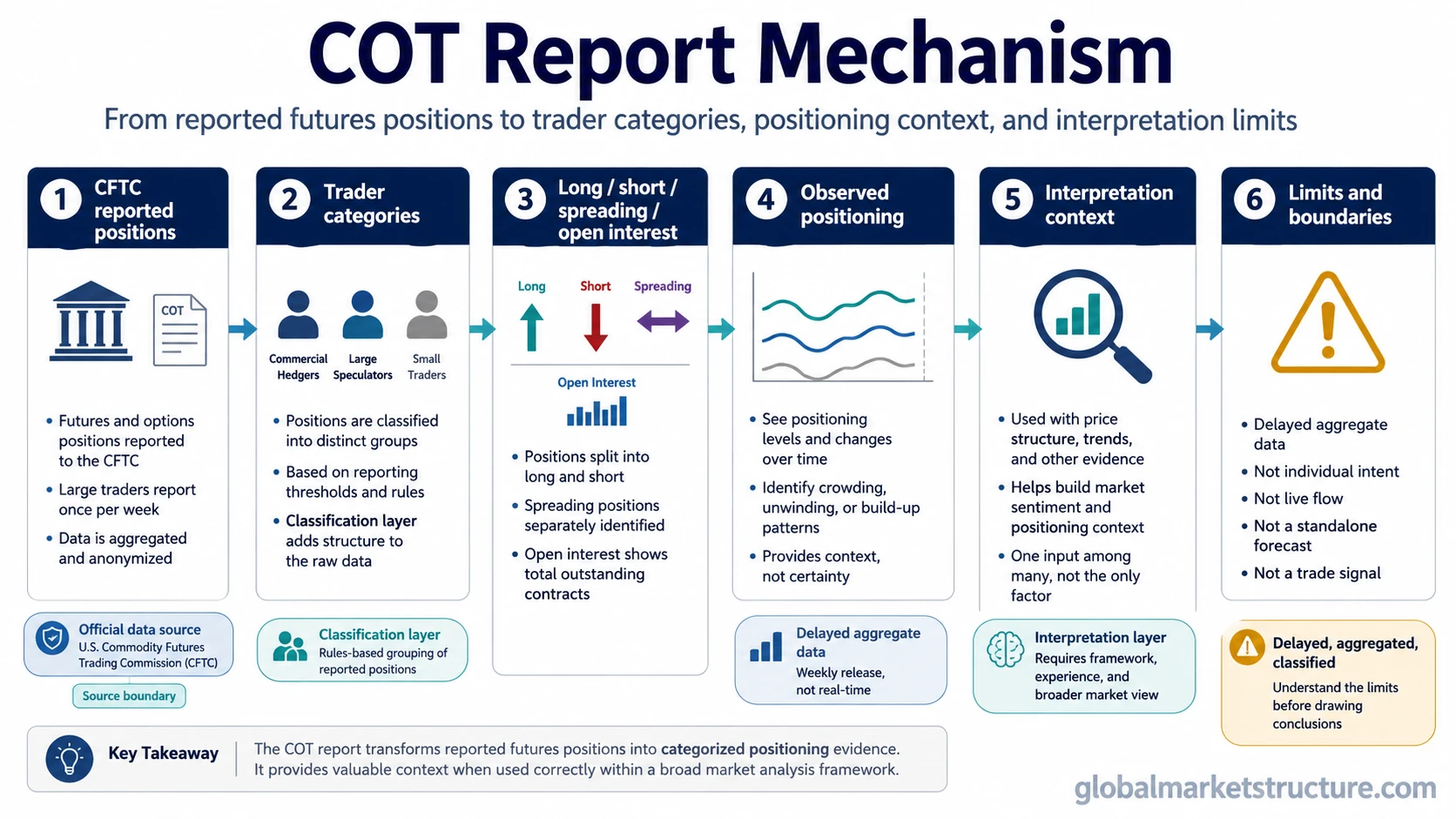

The Commitments of Traders report, often called the COT report, is a weekly CFTC report showing aggregate futures and options positioning by trader category. It helps interpret commercial and speculative positioning, open interest, and sentiment context, but the data is delayed from the reported position date and does not function as a standalone forecast or trade signal.

Definition: The COT report is a CFTC positioning report that summarizes how different groups of futures and options traders were positioned at a reported point in time. It is evidence of reported positioning, not real-time order flow or individual trader intent.

What it shows: Reported futures and options positioning, trader classifications, long and short exposure, spreading activity, open interest, and week-to-week changes.

What it does not show: Live order flow, individual motives, guaranteed price direction, or a direct instruction to take market exposure.

Key Points

- The COT report is published by the U.S. Commodity Futures Trading Commission.

- It summarizes reportable futures and options positions across trader classifications.

- The usual release uses previous Tuesday positioning data and is normally published later in the week.

- Commercial, non-commercial, managed-money, and other classifications vary by report type.

- COT data can support positioning and sentiment analysis, but it does not predict price direction by itself.

What the Commitments of Traders Report Shows

The COT report shows how open interest is distributed across trader groups in covered futures and options markets. The core information is not a market opinion. It is a categorized snapshot of reported positions: long exposure, short exposure, spreading activity, changes from prior reports, and the share of open interest represented by each category.

The official source is the CFTC Commitments of Traders report. Educational tools, charting platforms, and data vendors can make the information easier to visualize, but the CFTC remains the official source for the raw report family.

The positioning information is useful because futures markets often include different participants with different motives. A producer, swap dealer, asset manager, leveraged fund, and smaller trader may all appear in the same market, but their reported categories do not reveal the exact reason for each position. The report provides a structured starting point for interpretation, not a complete explanation of intent.

| Reported item | What it means | Interpretation boundary |

|---|---|---|

| Long positions | Reported exposure that benefits from a higher futures price, before considering hedges or broader portfolio context. | A large long position is not automatically bullish if it is crowded, hedged, or already reflected in price. |

| Short positions | Reported exposure that benefits from a lower futures price, before considering commercial hedging or spread structures. | A large short position is not automatically bearish if it reflects hedging, inventory, or risk management. |

| Spreading | Positions involving offsetting long and short exposure across related contracts or maturities. | Spread activity may reflect curve, basis, or relative-value positioning rather than a simple directional view. |

| Open interest | The total number of outstanding contracts represented in the report. | Open interest gives scale, but it does not show whether new exposure will keep expanding or unwind. |

| Changes from the prior report | Week-to-week movement in reported positions. | Changes are delayed and should be compared with price, liquidity, volatility, and broader positioning context. |

How Trader Categories Work

Trader categories are the main reason COT data is useful, and also the main reason it is often misread. The categories group traders by reporting classification, not by a perfect map of motive or forecasting skill. Commercial traders often have business or hedging exposure. Non-commercial and managed-money groups can show speculative exposure. Non-reportable positions represent smaller positions below reporting thresholds.

That distinction matters for market sentiment because positioning can reveal whether exposure is concentrated, stretched, or shifting. The safer interpretation is conditional: category behavior becomes more useful when it is compared with price response, volatility, liquidity, and broader risk appetite.

| Trader category | Typical role | Interpretation boundary |

|---|---|---|

| Commercial | Often linked to producers, merchants, processors, users, dealers, or hedging activity, depending on report type. | Commercial positioning should not be simplified into automatic smart-money direction. |

| Non-commercial | Often associated with larger speculative participants in legacy reports. | Speculative exposure can be informative, but it can also become crowded or late. |

| Managed Money | A category used in disaggregated reporting that can include commodity trading advisors, commodity pool operators, and similar money-management activity. | Managed-money positioning can show speculative concentration, not a guaranteed future price path. |

| Swap Dealers | A disaggregated category often connected with swap-related activity and client-facing risk transfer. | Dealer positioning can reflect intermediation and hedging rather than a simple directional view. |

| Other Reportables | Large reportable traders that do not fit the more specific disaggregated categories. | The category can contain mixed motives, so it should be read cautiously. |

| Non-reportable | Positions below reportable thresholds. | This category is aggregated residual positioning, not a precise map of small-trader intent. |

Main Types of COT Reports

COT reporting is not a single uniform table. The report family includes different formats that classify markets and traders in different ways. The right format depends on whether the question is about legacy commercial versus non-commercial exposure, commodity-market disaggregation, financial futures, or commodity index participation.

| Report type | What it covers | Useful for |

|---|---|---|

| Legacy | Traditional futures-only and futures-and-options combined reports with commercial, non-commercial, and non-reportable classifications. | Broad comparison of commercial and speculative exposure across long-running report history. |

| Supplemental | Additional commodity index trader information for selected agricultural markets. | Context where index-linked commodity exposure is relevant. |

| Disaggregated | Commodity market reports with more detailed categories such as Producer/Merchant/Processor/User, Swap Dealers, Managed Money, and Other Reportables. | Separating hedging, dealer, and managed-money behavior more carefully than legacy categories allow. |

| Traders in Financial Futures | Financial futures categories such as Dealer/Intermediary, Asset Manager/Institutional, Leveraged Funds, and Other Reportables. | Reading positioning in rates, currencies, equity index futures, and other financial futures contexts. |

How COT Fits Positioning and Sentiment

COT data fits a positioning and sentiment workflow because it shows how large groups of participants were exposed in futures and options markets. It can help identify whether speculative positioning is one-sided, whether commercial hedging is expanding, whether open interest is rising or falling, and whether a market move is occurring with crowded exposure or cleaner positioning.

Positioning context is not the same as a market decision. A market can remain strong while speculative exposure is already elevated. A market can also remain weak even after bearish exposure appears crowded. The useful question is whether reported exposure aligns or conflicts with liquidity, volatility, price acceptance, and broader cross-asset conditions.

The same logic applies to crowded trade risk. Crowding can matter when many participants are exposed in the same direction, but the timing and effect depend on absorption, liquidity, positioning history, and whether the market is forced to adjust.

Observed data: Reported positions by trader category, long and short exposure, spreading, open interest, and weekly changes.

Interpretation layer: Possible positioning pressure, speculative crowding, hedging activity, or sentiment context.

Not observed: Individual trader motives, live orders, intraday flow, future price direction, or a complete market-timing signal.

Observed Data vs Interpretation

The strongest use of COT is separating what the report actually records from what an analyst may infer from it. That separation prevents the common mistake of treating a reported category as a forecast. COT data can support a market view, but the market view still needs confirmation from price behavior, liquidity, volatility, and other positioning evidence.

| Layer | What COT provides | What still needs judgment |

|---|---|---|

| Reported data | Trader-category positions, open interest, long exposure, short exposure, spreads, and weekly changes. | Whether the data is already priced in or still changing market behavior. |

| Classification | Commercial, non-commercial, managed-money, dealer, asset-manager, and other categories depending on report type. | Whether a category reflects hedging, speculation, intermediation, or mixed motives. |

| Positioning context | Evidence that exposure may be concentrated, shifting, or diverging from price behavior. | Whether positioning is early, crowded, neutralized by hedges, or vulnerable to unwind. |

| Market interpretation | A structured input for sentiment and exposure analysis. | Whether price, liquidity, volatility, macro conditions, and cross-asset confirmation support the same reading. |

| Action boundary | No direct action instruction. | Any portfolio or trading decision would require a separate process, risk framework, and current data check. |

What COT Can and Cannot Tell You

COT can help explain positioning background. It can show whether a market has large speculative exposure, whether commercial positioning is changing, whether open interest is expanding, and whether categories are moving differently from price. These are useful inputs for market-structure interpretation.

Limitation: COT is delayed, aggregated, and classified. It does not show current intraday flow, individual motives, hidden hedges, option structures outside the report view, or future price direction. Strong interpretation requires context beyond the report.

The reporting lag matters because markets can move meaningfully between the position date and the release. A reading that looked extreme on the reported date may already have changed by the time the report is published. That does not make the data useless, but it changes the role of the data from immediate signal to positioning evidence.

Aggregation also matters. A category can contain participants with different reasons for holding exposure. Commercial shorts in a commodity market may reflect hedging against production or inventory. Leveraged-fund longs in a financial future may reflect trend exposure, relative-value positioning, or broader portfolio construction. The category is a starting point, not a complete motive map.

Common COT Report Misuses

Common mistake: Treating commercial traders as automatically correct and speculative traders as automatically late. The categories can be useful, but they do not rank participants by forecasting ability.

Another mistake is reading net positioning as automatically bullish or bearish. Net long exposure can be supportive in one environment and crowded in another. Net short exposure can show pessimism, hedging, or pressure, but it does not guarantee a reversal. Interpretation depends on whether the market is absorbing the exposure, rejecting it, or forcing it to unwind.

A third mistake is isolating COT from other sentiment tools. A sentiment index can summarize mood, while COT shows reported futures and options positioning. The Fear and Greed Index belongs to a different evidence family because it combines sentiment inputs rather than reporting trader classifications from the futures market.

COT Report Example in Positioning Context

Speculative positioning in a futures market may rise for several weeks while price continues to advance. That can suggest trend-following exposure is building, but it does not prove that the move is near exhaustion. The interpretation changes if open interest is expanding, liquidity is deep, volatility remains contained, and price continues to hold accepted levels.

The same positioning becomes more fragile if price stops responding to additional speculative exposure, volatility rises, liquidity thins, and later attempts to hold the prior range fail. In that setting, COT helps identify crowding risk, while market absorption and price response determine whether the positioning pressure is becoming visible.

The distinction is practical: COT identifies reported exposure, while the market confirms or rejects the interpretation through later behavior. Positioning evidence is more useful when it is part of a broader positioning and sentiment framework rather than a single-line conclusion.

Where to Find Official COT Data

The official source is the CFTC. The CFTC publishes the report family, release schedule, explanatory notes, and current or historical report files. Data platforms and charting tools can help visualize the same information, but official data should be checked when accuracy, report type, category definition, or date-specific positioning matters.

The official CFTC source is especially important for current readings. Any statement about current COT positioning needs the exact report date, market, report type, and source. Without those details, the safer treatment is conceptual: explain how the report works, how categories are interpreted, and where the limitations sit.

Related Positioning Concepts

COT belongs inside capital flows and positioning because it connects trader exposure with broader market interpretation. It is most useful beside other evidence rather than as a replacement for it.

Market sentiment can show the emotional or behavioral backdrop. Crowded positioning can show concentration risk. Sentiment indexes can summarize multi-input fear or greed conditions. COT adds a different lens by showing reported futures and options positioning across trader classifications.

FAQ

What is the COT report?

The COT report is a weekly CFTC report showing aggregate futures and options positioning by trader category. It helps interpret positioning and sentiment context, but it does not show real-time flow or future price direction.

Who publishes the Commitments of Traders report?

The U.S. Commodity Futures Trading Commission publishes the Commitments of Traders report family, including report files, release schedules, and explanatory material.

Why is COT data delayed?

COT data is based on reported positions for a prior reporting date and is normally released later in the week. The delay means the data is better suited for positioning context than real-time market timing.

What is the difference between commercial and non-commercial traders in COT?

Commercial traders are often linked to business, dealer, or hedging activity, while non-commercial traders are often associated with larger speculative exposure in legacy reports. The distinction is useful, but it does not reveal exact motives or forecasting ability.

Does the COT report predict price direction?

No. The COT report can support positioning and sentiment analysis, but it does not predict price direction by itself. Price behavior, liquidity, volatility, and broader market context still matter.