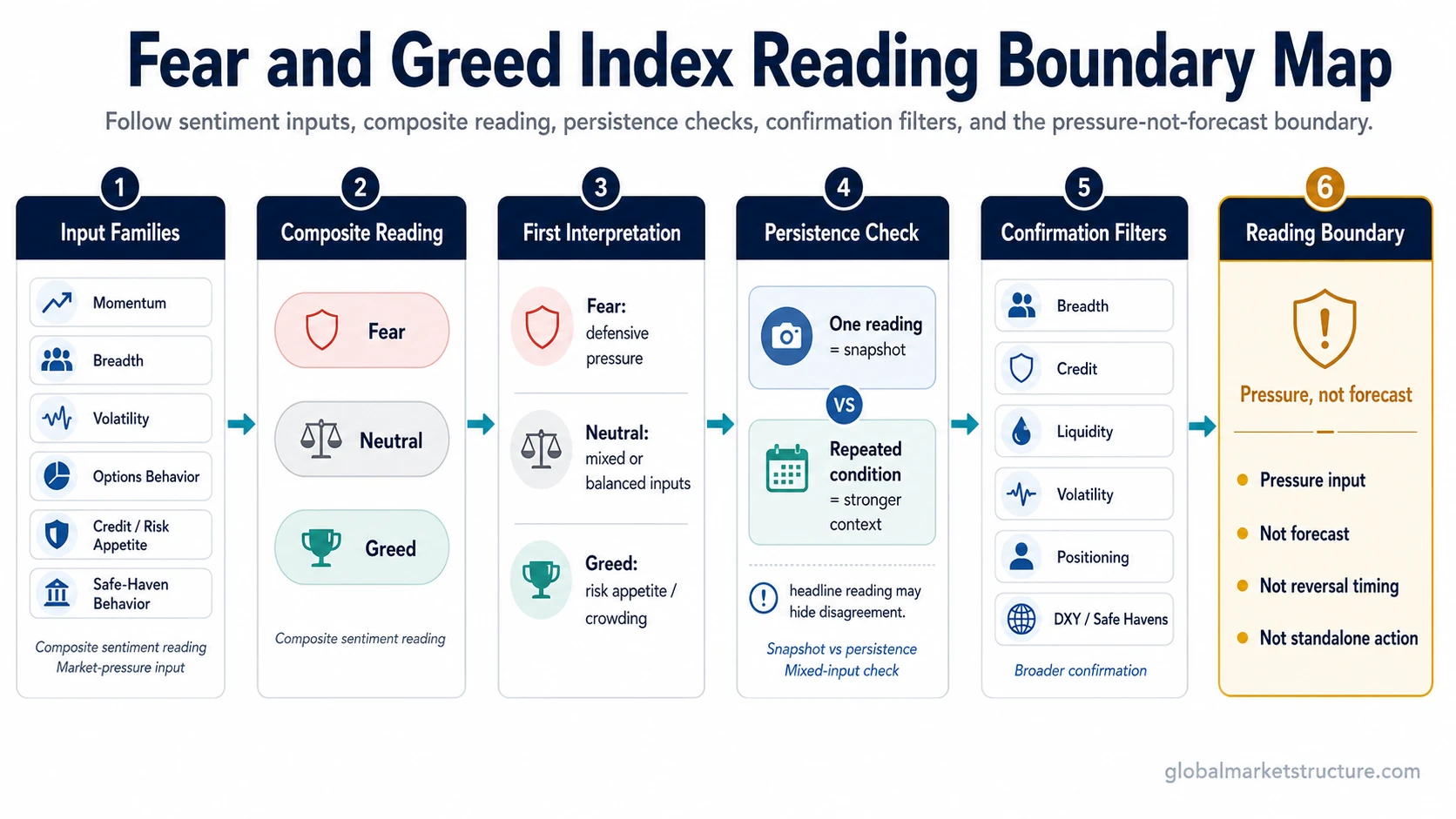

The Fear and Greed Index is a composite sentiment and market-pressure gauge that summarizes whether selected market inputs lean toward fear, neutrality, or greed. A fear or greed reading can help frame risk appetite, defensive pressure, or crowding, but it is not a forecast, not reversal timing, and not a standalone buy/sell signal.

| Question | Short answer |

|---|---|

| What is it? | A composite sentiment gauge that groups selected market inputs into a fear-to-greed reading. |

| What does it measure? | Market pressure, risk appetite, and sentiment conditions across several input categories. |

| What does fear suggest? | Defensive positioning, stress, risk aversion, or demand for safer assets. |

| What does greed suggest? | Risk appetite, confidence, momentum, or crowded optimism. |

| What can it not prove? | It cannot prove that a reversal is near, that a trend must continue, or that a market action should be taken. |

The live tool can show the current reading; the analytical value is understanding what that reading can and cannot mean inside a broader market-structure review.

What the Fear and Greed Index measures

The Fear and Greed Index is best understood as a summary layer. Instead of treating one market input as the whole story, it combines several sentiment-sensitive inputs into one reading. Many Fear and Greed Index presentations use a 0 to 100 style scale, where lower readings represent fear, middle readings represent neutral conditions, and higher readings represent greed. The exact provider methodology should be checked at the source before relying on a specific component formula.

The number matters less than the condition behind it. A fearful reading may reflect defensive behavior, elevated volatility, rising credit pressure, or stronger demand for safer assets. A greedy reading may reflect risk appetite, strong momentum, or a greater willingness to hold risky assets.

Sentiment describes the tone of market behavior; positioning asks how participants are actually placed. The two can align, but they are not the same signal.

Different providers can define sentiment inputs differently, so the safest interpretation is to treat the index as a broad composite reading rather than a complete formula. The component categories below show the kinds of market evidence that can shape a fear-or-greed interpretation without treating any single input as decisive.

| Input category | What it can reveal | Why it needs context |

|---|---|---|

| Momentum | Whether price behavior is leaning toward strength or weakness. | Momentum may persist and does not identify exhaustion by itself. |

| Breadth | Whether participation is broad or concentrated. | A strong index can hide weak participation beneath the surface. |

| Volatility | Whether markets are pricing more uncertainty or calm. | Volatility can rise for different reasons, not only panic. |

| Options behavior | Whether hedging or speculative demand is becoming more visible. | Options flows may reflect hedging, speculation, or positioning adjustment. |

| Credit and risk appetite | Whether investors are more willing or less willing to hold risky credit. | Credit stress matters more when it aligns with liquidity and breadth weakness. |

| Safe-haven behavior | Whether defensive assets are attracting demand. | Safe-haven demand may reflect temporary hedging or a broader risk-off shift. |

How fear, neutral, and greed readings should be interpreted

A fear reading usually means the selected inputs lean defensive. That can happen when volatility is elevated, breadth is weak, hedging demand rises, or investors prefer safer assets. Fear can reflect stress, but it can also reflect protection after a market decline has already occurred.

A neutral reading usually means the inputs are mixed or balanced. Neutral does not mean risk is absent. It may simply mean that bullish and bearish pressures are offsetting each other inside the composite.

A greed reading usually means the selected inputs lean toward risk appetite. That can happen when momentum is strong, volatility is calm, breadth is supportive, or investors show greater willingness to hold risky assets. Greed can reflect confidence, but it can also reflect crowding if the same behavior becomes one-sided.

| Reading | Possible interpretation | Common mistake |

|---|---|---|

| Fear | Risk aversion, stress, defensive pressure, or protection demand. | Assuming fear automatically means a reversal is near. |

| Neutral | Balanced or mixed inputs without a clear sentiment extreme. | Assuming neutral means nothing important is happening. |

| Greed | Risk appetite, confidence, momentum, or crowded optimism. | Assuming greed automatically means a market top is near. |

Why the Fear and Greed Index is not a forecast

The Fear and Greed Index describes pressure. It does not forecast the next price move. Fear can persist in weak market regimes, and greed can persist in strong liquidity or momentum environments. A high or low reading can matter, but the reading needs confirmation from other market-structure evidence.

Reading boundary

The index can help identify a sentiment condition, but it does not define timing, direction, trade quality, or risk management. It should not be used as a standalone market call.

The most useful question is not whether the reading is fearful or greedy. The stronger question is whether the reading agrees with breadth, credit, liquidity, volatility, positioning, and price structure.

Persistence and crowding matter more than one reading

One reading can be noisy. A repeated fear condition can show that defensive pressure is becoming more durable. A repeated greed condition can show that confidence or crowding is becoming more established. Persistence helps separate a temporary snapshot from a broader sentiment environment.

Mixed inputs also matter. A headline score can hide disagreement underneath. For example, momentum may look strong while breadth weakens, or volatility may appear calm while credit conditions deteriorate. In those cases, the composite reading should be treated as incomplete until the underlying evidence is checked.

Crowding is different from optimism. Optimism describes tone. Crowding describes how one-sided behavior may have become. Greed becomes more important when it is supported by evidence that many participants are leaning the same way.

How to confirm a Fear and Greed Index reading

Confirmation should come from independent inputs. A fear reading is more meaningful when breadth weakens, credit spreads widen, liquidity conditions tighten, volatility rises, and defensive assets attract demand. A greed reading is more meaningful when participation is broad, credit conditions are calm, liquidity is supportive, volatility is contained, and risk assets show broad strength.

| Confirmation area | What to check | Interpretation value |

|---|---|---|

| Breadth | Participation across stocks, sectors, or markets. | Shows whether the reading is broad or concentrated. |

| Credit | Risk appetite in corporate credit and spread behavior. | Helps identify whether stress is visible outside equities. |

| Liquidity | Funding, market depth, and broader liquidity conditions. | Shows whether sentiment pressure has structural support. |

| Volatility | Whether uncertainty is rising, falling, or staying contained. | Helps separate calm confidence from fragile complacency. |

| Positioning | Whether participants appear one-sided or balanced. | Helps identify crowding rather than sentiment alone. |

| DXY and safe havens | Dollar pressure, defensive demand, and risk-off behavior. | Helps connect sentiment to the broader cross-asset environment. |

The strongest interpretation usually appears when several independent inputs point in the same direction. If the index says greed but breadth is narrowing and credit is deteriorating, the reading is less clean. If the index says fear but credit is calm and breadth is improving, the fear reading may describe caution rather than deep market stress.

Example of a safe interpretation

A practical scenario is a market with a greed reading, strong headline index momentum, and calm volatility. That condition can look constructive at first. The interpretation changes if participation narrows, credit spreads stop confirming, and safe-haven demand begins to rise. In that case, the greed reading may still describe risk appetite, but the surrounding structure warns that the reading is less broad than it looks.

The same logic works in the other direction. A fear reading can look severe, but if breadth begins stabilizing, credit stops deteriorating, and volatility cools, the fear condition may be losing pressure. The index alone cannot prove that shift; it only gives a sentiment starting point.

Fear and Greed Index versus market sentiment

The Fear and Greed Index is one way to summarize market sentiment. Market sentiment is the broader category. It includes the tone, risk appetite, confidence, caution, and emotional pressure visible across markets.

The index is narrower because it turns selected inputs into a composite reading. That makes it useful for quick orientation, but it should not replace a fuller sentiment review.

Fear and Greed Index versus positioning data

Positioning data shows how participants are actually exposed. A sentiment index shows how selected market inputs lean emotionally or behaviorally. Sentiment can shift before positioning changes, but positioning can also reveal crowded exposure that a sentiment reading does not fully capture.

That distinction matters because sentiment and positioning can diverge. A market can feel fearful while some participants are already heavily hedged. A market can feel greedy while positioning is not yet crowded. For a more direct positioning lens, the Commitments of Traders report is a separate data source rather than a composite sentiment index.

Common mistakes when reading the Fear and Greed Index

- Treating fear as an automatic bullish reversal signal.

- Treating greed as an automatic bearish reversal signal.

- Ignoring whether the reading is persistent or only a one-day snapshot.

- Using the headline reading without checking mixed underlying inputs.

- Reading sentiment without breadth, credit, liquidity, volatility, positioning, and safe-haven confirmation.

- Confusing a composite sentiment gauge with a complete market regime model.

FAQ

What does the Fear and Greed Index mean?

It means selected market inputs are being summarized into a composite sentiment reading that leans toward fear, neutrality, or greed. The reading helps describe the current sentiment condition, not forecast the next market move.

Is the Fear and Greed Index a buy or sell signal?

No. It is not a standalone buy or sell signal. Fear does not automatically mean a rebound is near, and greed does not automatically mean a decline is near.

Can fear or greed readings last for a long time?

Yes. Fear and greed readings can persist when the underlying market environment continues to support them. Persistence matters because one reading may be noise, while repeated readings can describe a more durable sentiment condition.

What should confirm a Fear and Greed Index reading?

Useful confirmation can come from breadth, credit conditions, liquidity, volatility, positioning, safe-haven behavior, and price structure. The reading is stronger when several independent inputs point in the same direction.