Safe haven assets are assets that may attract demand during market stress because they are perceived as more resilient, liquid, stable, or less exposed to the dominant shock. In risk-on and risk-off analysis, they can help show when market behavior is shifting toward defense and caution. Safe haven does not mean risk-free, predictive, or guaranteed.

Direct definition: A safe haven asset is an asset category that investors and institutions may prefer when uncertainty rises, risk appetite weakens, and confidence in more cyclical or leveraged assets deteriorates.

Market role: Safe haven demand can be useful risk-environment evidence when it appears alongside broader stress conditions such as weaker breadth, wider credit spreads, tighter liquidity, or rising volatility.

Main limitation: A safe haven move by itself does not confirm a crash, a recession, a trading signal, or a complete risk-off regime.

What Are Safe Haven Assets?

Safe haven assets are commonly associated with defensive behavior during periods of market stress. They are not defined only by their label. Their safe-haven status depends on how market participants treat them when confidence falls, liquidity becomes more valuable, and exposure to riskier assets becomes less attractive.

The important distinction is between perceived safety and realized protection. An asset can be viewed as a safe haven because it has deep liquidity, high credit quality, strong collateral value, historical defensive associations, or lower exposure to a specific shock. That does not mean it will protect capital in every environment.

In market-structure analysis, safe-haven demand can reveal a defensive shift in market behavior. It is most useful when read together with broader risk appetite, credit, liquidity, rates, volatility, and cross-asset evidence.

How Safe Haven Assets Behave During Market Stress

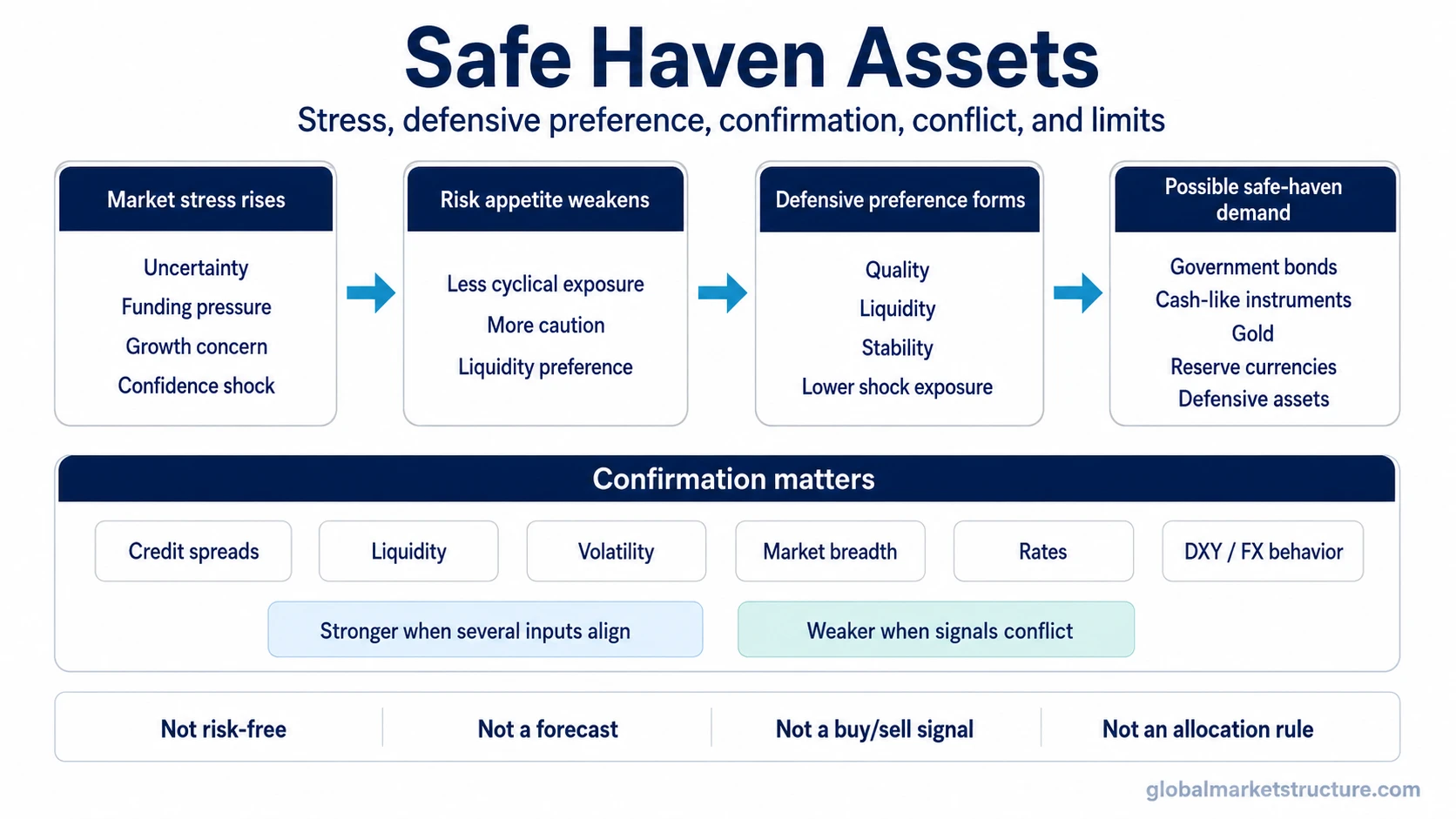

Safe haven behavior usually begins with a change in preference. As stress rises, some participants reduce exposure to assets that depend heavily on growth, leverage, funding availability, or confidence. Demand may then shift toward assets perceived as more liquid, higher quality, more stable, or less exposed to the immediate source of stress.

Basic mechanism:

- Market stress rises.

- Risk appetite weakens.

- Liquidity, quality, collateral confidence, or relative resilience becomes more valuable.

- Some safe-haven categories may attract demand or show relative strength.

- The interpretation becomes more credible only when broader market evidence confirms the defensive shift.

This is why safe-haven assets should be read as context, not as a standalone conclusion. A rise in one traditional safe-haven asset may reflect risk aversion, but it may also reflect rates, currency movements, inflation expectations, positioning, technical flows, or asset-specific demand.

Common Types of Safe Haven Assets

Safe haven assets are usually discussed by category rather than by a fixed universal list. The same category can behave defensively in one shock and poorly in another. The useful question is not which asset is always safe, but why a category might attract defensive demand under specific conditions.

| Category | Why it may be treated as a safe haven | Main caveat |

|---|---|---|

| Gold and precious metals | Often associated with store-of-value demand, currency concerns, and stress-period caution. | Can be affected by real yields, dollar strength, liquidity needs, positioning, and investor flows. |

| High-quality government bonds | May attract demand when investors prefer credit quality, deep liquidity, and duration exposure. | Can lose value when yields rise, inflation pressure increases, or duration risk dominates. |

| Cash and cash-like instruments | Can become attractive when liquidity, optionality, and capital preservation are prioritized. | Can lose purchasing power through inflation or weaken if the currency itself is under pressure. |

| Some currencies | May benefit when global investors prefer liquid funding, reserve, or current-account strength characteristics. | Currency behavior depends on rates, policy, funding stress, positioning, and the specific shock. |

| Defensive equities | May show relative resilience when investors prefer steadier earnings or less cyclical demand. | They remain equities and can fall during broad deleveraging or severe liquidity stress. |

Why Safe Haven Does Not Mean Risk-Free

The phrase “safe haven” can create a misleading impression. It does not mean an asset has no downside, no volatility, no liquidity risk, or no regime sensitivity. It means market participants may treat the asset as relatively more defensive under certain stress conditions.

Safe haven does not mean:

- risk-free;

- guaranteed to rise during stress;

- a forecast of a market crash;

- a buy signal;

- proof that a full risk-off regime has started.

The behavior depends on the type of shock. A growth scare, inflation shock, liquidity squeeze, banking stress, currency shock, or policy surprise can affect safe-haven categories differently. The same asset that looks defensive in one environment can underperform when a different risk dominates.

Rates and liquidity are especially important. High-quality bonds may be treated as safe havens when falling growth expectations dominate, but they can be vulnerable when rising yields or inflation pressure are the main problem. Gold may attract defensive demand in some stress periods, but it can also be pressured by real yields, dollar strength, or forced liquidity selling.

Safe Haven Assets vs Nearby Concepts

Safe haven assets are often confused with several related terms. The differences matter because each term describes a different layer of market interpretation.

| Concept | Meaning | How it differs from safe haven assets |

|---|---|---|

| Safe assets | Assets usually associated with low credit risk, liquidity, or institutional trust. | Safe asset is more about structural quality. Safe haven is more about stress-period behavior. |

| Safe-haven currencies | Currencies that may attract demand during global stress or funding pressure. | They are the FX subset of the broader safe-haven asset discussion. |

| Flight to quality | A behavioral shift toward assets perceived as higher quality or more liquid. | Flight to quality is the movement. Safe haven assets are possible destinations of that movement. |

| Risk-off assets | Assets or categories associated with defensive behavior in a broader risk-off environment. | Risk-off is a regime framing. Safe haven assets are one entity group inside that broader behavior. |

A clean interpretation separates the asset category from the market behavior. Safe haven assets may receive demand during stress, but the stress condition itself must be confirmed by wider evidence.

A Simple Safe-Haven Scenario

A common scenario starts with weakening equity participation. Market breadth deteriorates, volatility rises, and credit conditions begin to look less stable. At the same time, demand increases for assets perceived as more liquid, higher quality, or less exposed to the immediate stress source.

That combination can make safe-haven demand more meaningful. It suggests that the move is not just an isolated asset reaction, but part of a broader defensive shift. The interpretation weakens if credit remains calm, liquidity is stable, volatility is contained, and risk assets continue to show broad participation.

Practical reading: Safe-haven demand is strongest as evidence when it appears alongside multiple stress inputs. It is weaker when one defensive asset moves alone while the rest of the market still behaves normally.

How to Interpret Safe-Haven Demand

Safe-haven demand becomes more useful when it is placed inside a broader risk-environment framework. The question is not whether one asset is labeled safe, but whether market behavior is shifting toward defense across several dimensions.

| Signal area | What to check | Interpretation risk |

|---|---|---|

| Credit | Whether spreads are widening or credit-sensitive assets are weakening. | Credit can move for sector-specific reasons or liquidity conditions rather than broad stress alone. |

| Liquidity | Whether market depth, funding conditions, or cash preference are changing. | Liquidity stress can force selling even in assets normally considered defensive. |

| Volatility | Whether implied or realized volatility is rising across markets. | Volatility spikes can be short-lived and may not confirm a durable regime shift. |

| Market breadth | Whether fewer assets are participating in risk exposure. | Weak breadth can be temporary or concentrated in specific sectors. |

| Rates and currencies | Whether bond yields, real yields, reserve currencies, and funding currencies support the defensive interpretation. | Rates and FX can reflect policy expectations, inflation, or positioning rather than simple risk aversion. |

The strongest reading appears when safe-haven demand, weaker risk appetite, tighter liquidity, wider credit spreads, and defensive cross-asset behavior point in the same direction. Mixed signals require a more cautious interpretation.

Common Mistakes When Reading Safe Haven Assets

Mistake 1: Treating safe haven as a permanent label.

An asset can be defensive in one regime and vulnerable in another. The label should not replace context.

Mistake 2: Assuming safe-haven demand confirms a full risk-off regime.

One asset move is not enough. Broader confirmation from credit, volatility, liquidity, breadth, rates, and currencies matters.

Mistake 3: Ignoring why the asset is moving.

Gold, bonds, currencies, and defensive equities can move for reasons unrelated to broad market fear. Rates, inflation expectations, policy, positioning, and liquidity flows can all matter.

Mistake 4: Confusing defensive preference with guaranteed protection.

Safe haven assets can still decline, become volatile, or fail to offset losses elsewhere.

Safe Haven Assets in Risk-On and Risk-Off Analysis

Safe haven assets matter most when the market is shifting from risk-seeking behavior toward defensive behavior. In a risk-on environment, investors generally accept more uncertainty and prefer assets tied to growth, credit expansion, liquidity, and confidence. In a risk-off environment, defensive preference becomes more important.

Safe-haven demand can support a risk-off interpretation when other evidence agrees. That evidence may include weaker cyclical assets, wider credit spreads, higher volatility, pressure in funding-sensitive markets, falling breadth, or stronger demand for liquidity and perceived quality.

Even then, safe-haven demand is still only one input. It helps describe market behavior, but it does not produce a forecast, ranking, allocation rule, or trading instruction.

FAQ

Are safe haven assets risk-free?

No. Safe haven assets can still lose value, become volatile, or underperform. The term means they may be perceived as more defensive during certain stress conditions, not that they guarantee protection.

What are common examples of safe haven assets?

Common categories include gold and precious metals, high-quality government bonds, cash or cash-like instruments, some currencies, and selected defensive equities. Each category has caveats and can behave differently depending on the shock.

Is gold always a safe haven asset?

No. Gold is often treated as a traditional safe-haven category, but its behavior can be affected by real yields, the dollar, liquidity needs, positioning, and investor flows.

Are safe haven assets the same as safe-haven currencies?

No. Safe-haven currencies are a subset of the broader safe-haven asset discussion. Safe haven assets can include metals, bonds, cash-like instruments, currencies, and other categories that may attract defensive demand.

Can safe haven assets predict a market crash?

No. Safe-haven demand can be a warning or confirmation clue when broader stress conditions align, but it does not predict a crash by itself and should not be treated as a standalone forecast.