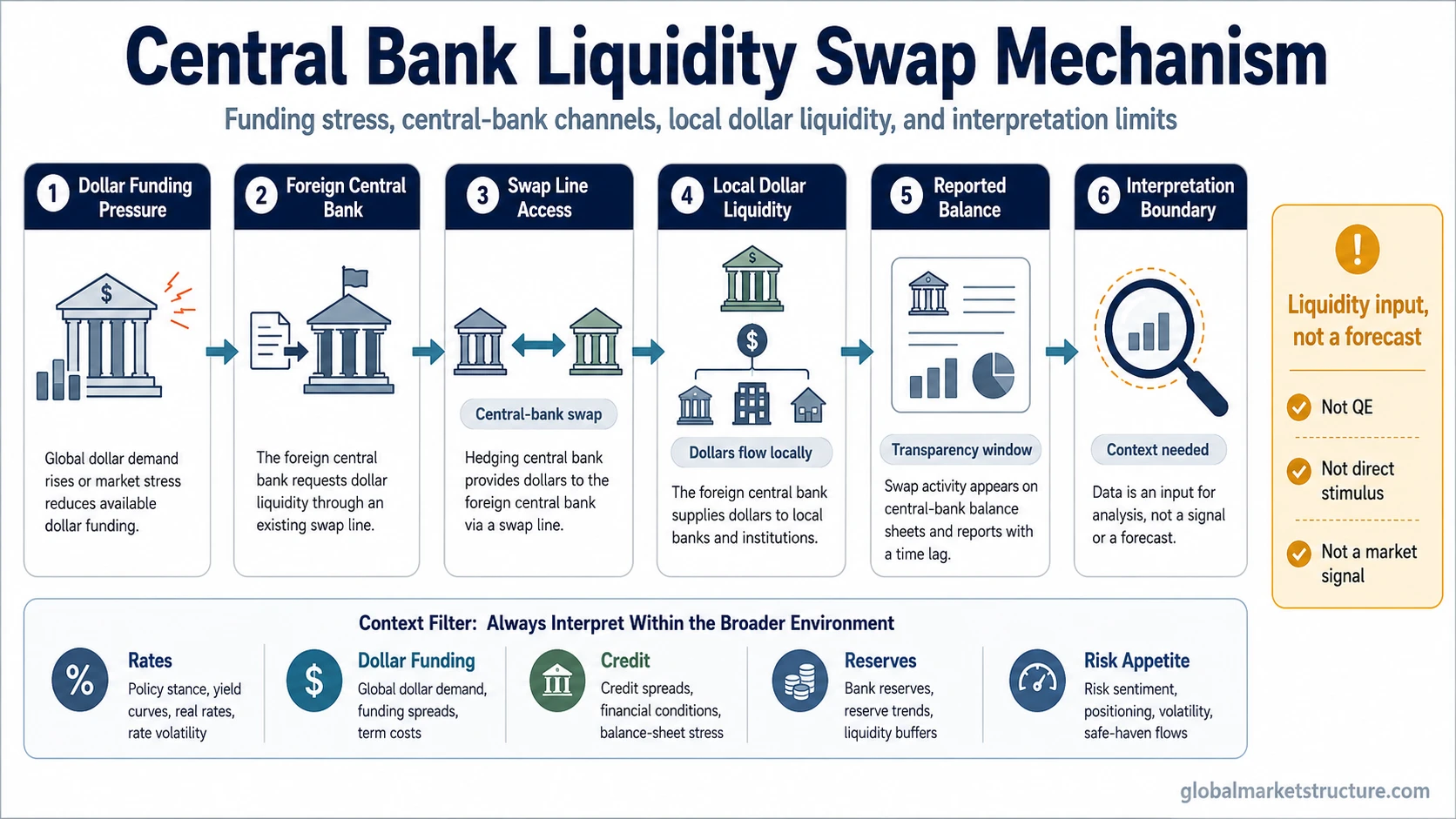

Central bank liquidity swaps are arrangements between central banks that provide foreign-currency liquidity, most often U.S. dollars, through a swap structure. They function as funding backstops during stress, not as quantitative easing, direct market stimulus, or standalone signals for asset prices.

Definition: A central bank liquidity swap is a central-bank-to-central-bank facility that allows one central bank to obtain foreign currency from another central bank and provide that liquidity within its own jurisdiction. The term is closely related to central bank swap lines, especially when markets discuss U.S. dollar funding stress.

Key Points

- Central bank liquidity swaps are official foreign-currency liquidity arrangements between central banks.

- They are commonly discussed as swap lines, especially when offshore dollar funding becomes strained.

- The facility can support funding conditions, but it does not work like QE.

- Swap-line activity is an input into liquidity analysis, not a market forecast or trading signal.

What Central Bank Liquidity Swaps Are Not

The main misunderstanding is treating swap lines as if they were a general liquidity signal for all markets. The facility is narrower: it addresses foreign-currency funding pressure through a central-bank channel.

| Misread | Cleaner interpretation |

|---|---|

| Swap lines are QE. | QE usually refers to asset purchases and balance-sheet policy. Liquidity swaps are foreign-currency funding arrangements between central banks. |

| Swap lines are open market operations. | Open market operations are domestic monetary operations. Liquidity swaps address cross-border foreign-currency funding pressure. |

| The Fed lends directly to foreign commercial banks. | The central-bank channel matters. A foreign central bank receives dollars and can then provide dollar liquidity within its own jurisdiction. |

| Swap activity guarantees risk-asset support. | Activity can point to funding demand or stress, but it does not guarantee a market direction. |

| Swap lines measure global liquidity by themselves. | They are one liquidity channel. Broader interpretation also depends on rates, credit, reserves, funding markets, dollar pressure, and risk appetite. |

Interpretation limit: swap-line availability or activity can matter for liquidity analysis, but it does not prove a crisis, predict equity direction, or replace official operation and balance-sheet data.

How Central Bank Liquidity Swaps Work

The mechanism is best understood as a funding channel. The facility does not begin with a direct purchase of risk assets. It begins with a foreign-currency liquidity need inside a financial system.

- Dollar funding pressure appears: banks or other institutions outside the United States may need dollar funding when private funding markets become strained.

- A foreign central bank accesses the swap line: the foreign central bank obtains dollars through an arrangement with the providing central bank.

- The swap structure is created: local currency is exchanged under the arrangement, and the transaction is later reversed according to the terms of the facility.

- Dollars move through the local central bank: the foreign central bank can lend dollars to eligible institutions in its jurisdiction.

- The facility is unwound: the arrangement is settled according to its official terms rather than through an open-ended asset purchase program.

- Outstanding amounts can appear in data: the amount outstanding may be visible in central-bank balance-sheet or official data series.

- Market interpretation remains conditional: the same observation needs surrounding funding, credit, rate, dollar, and liquidity context.

Data note: official central-bank releases, New York Fed operation pages, Federal Reserve balance-sheet releases, and FRED-style official data series are the proper sources for current swap usage levels. Any current value should be dated and sourced because reported balances can change with weekly reporting and operation activity.

Why Swap Lines Matter During Dollar Funding Stress

Dollar funding stress can become a global market-structure issue because the U.S. dollar is widely used in cross-border borrowing, trade finance, reserve management, and institutional funding. When private dollar funding becomes harder to obtain, the pressure can spread beyond one domestic market.

Central bank liquidity swaps can reduce that pressure by creating an official backstop. The important plumbing detail is the first recipient of liquidity: the dollars move through the foreign central bank, not directly into asset markets. That distinction keeps the interpretation anchored in funding conditions rather than in a simple asset-price conclusion.

A swap line can therefore matter even when it does not create a clean market signal. It can show that policymakers are supporting a funding channel, but the market response still depends on whether funding stress eases, credit conditions stabilize, dollar pressure changes, and risk appetite improves.

How To Read Swap Activity Without Overclaiming

The useful distinction is observed facility activity versus inferred market stress. The observation can be real while the interpretation remains uncertain.

| Observation | Possible interpretation | Cannot infer from that alone |

|---|---|---|

| A swap line exists. | Central banks have a channel available for foreign-currency liquidity support. | That markets are currently in crisis or that risk assets must react in one direction. |

| Outstanding swaps increase. | Demand for official foreign-currency liquidity may be increasing. | That the facility is the only driver of market behavior. |

| Outstanding swaps decline. | Demand for the facility may be easing, or private funding conditions may have improved. | That all liquidity stress has disappeared. |

| The reported balance is low. | Institutions may not need the facility, or funding stress may be appearing through other channels. | That global liquidity conditions are automatically healthy. |

| Operation access expands. | Central banks may be increasing access to foreign-currency liquidity channels. | That the action is equivalent to broad monetary stimulus or QE. |

Swap data becomes more useful when compared with other funding and risk indicators. Dollar strength, cross-currency funding pressure, credit spreads, money-market conditions, Treasury-market functioning, and central-bank balance-sheet changes can all alter the interpretation.

A Practical Dollar Funding Scenario

Offshore institutions need dollars to meet funding obligations, but private dollar funding becomes more expensive or harder to access. The local central bank has access to a dollar swap line and can obtain dollars through the central-bank arrangement. Those dollars can then be provided locally to reduce pressure in the domestic banking system.

The market reading remains conditional. The observation supports a funding-stress interpretation more than a direct asset-price forecast. A stronger case would require surrounding evidence that funding conditions are strained and that the swap channel is being used to relieve that pressure. A weaker case appears when activity is small, temporary, or not confirmed by wider funding-market stress.

Central Bank Liquidity Swaps and Nearby Concepts

Central bank liquidity is the broader condition that includes balance-sheet channels, reserves, facilities, and policy operations. Liquidity swaps are one specific cross-border foreign-currency funding mechanism within that larger liquidity environment.

Open market operations are different because they are domestic operating tools used to implement monetary policy and manage reserves. Liquidity swaps address foreign-currency funding pressure across central-bank balance sheets.

Quantitative easing, quantitative tightening, central-bank balance-sheet changes, dollar liquidity, and global liquidity can interact with the same market environment, but they should not be collapsed into the same concept. The cleaner reading separates the tool, the institution receiving liquidity first, the funding channel affected, and the market inference being made.

FAQ

Are central bank liquidity swaps the same as swap lines?

They are closely related terms in market discussion. Swap lines usually refer to the standing or temporary arrangements that allow central banks to exchange currencies and provide foreign-currency liquidity through the central-bank channel.

Are central bank liquidity swaps QE?

No. QE usually involves asset purchases and balance-sheet policy. Central bank liquidity swaps are foreign-currency funding arrangements that help a central bank provide liquidity within its own jurisdiction.

Does rising swap activity predict markets?

No. Rising activity can be relevant to funding-stress analysis, but it does not predict market direction by itself. Interpretation still depends on dollar funding conditions, credit, rates, liquidity, and risk appetite.