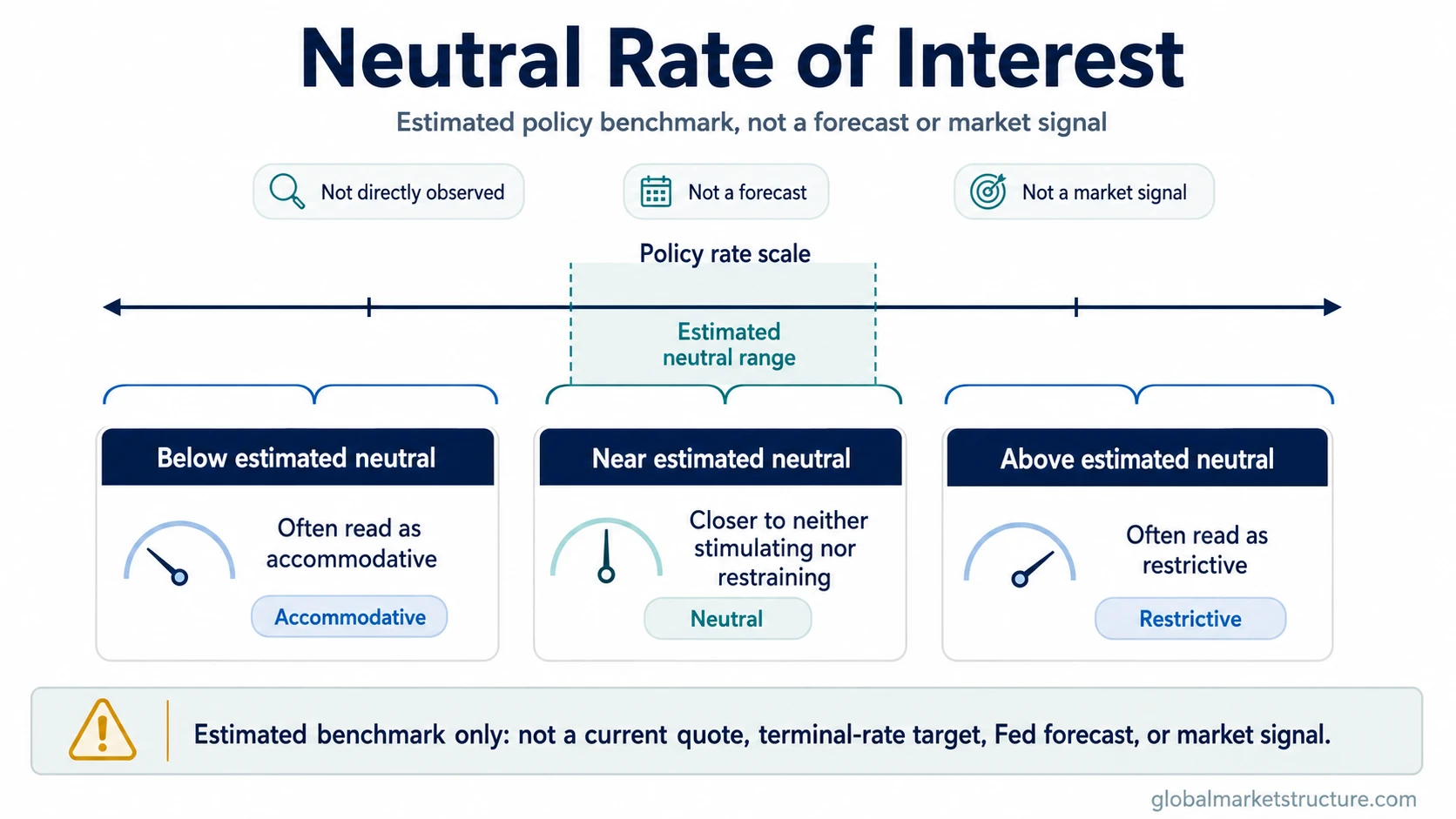

The neutral rate of interest is an estimated policy-rate benchmark, also called the natural rate of interest or r-star, used to judge whether monetary policy is accommodative, neutral, or restrictive. It is not directly observed in markets. It is not a Fed forecast, a terminal-rate target, or a market-direction signal.

The concept matters because a policy rate can look high or low only relative to the economic environment around it. If the policy rate is estimated to be above neutral, policy is usually interpreted as restrictive. If it is estimated to be below neutral, policy is usually interpreted as accommodative. The word “estimated” is essential because the neutral rate is inferred from models, data, assumptions, and changing economic conditions.

Direct definition: the neutral rate of interest is the estimated interest rate consistent with an economy operating near its potential, with inflation stable and policy neither stimulating nor restraining activity.

Why the Neutral Rate Is Estimated, Not Observed

The neutral rate is not a quoted market price. It cannot be read directly from the federal funds rate, Treasury yields, inflation data, or a central-bank statement. Economists estimate it from relationships among output, inflation, productivity, savings, investment demand, demographics, risk preferences, and financial conditions.

This is why r-star estimates can differ across models and institutions. A model can suggest where neutral may be, but it cannot remove uncertainty. Different estimates can still be useful when they show that the neutral rate is better understood as a range of uncertainty than as a single precise point.

Interpretation boundary: a neutral-rate estimate is a policy benchmark, not a live instrument. It helps frame whether policy may be tight or easy, but it does not produce a precise market instruction.

How the Neutral Rate Relates to Policy Stance

The main use of the neutral rate is policy-stance interpretation. A central bank may compare the actual policy rate with an estimated neutral rate to judge whether policy is leaning restrictive, neutral, or accommodative.

| Policy rate relative to estimated neutral | Common interpretation | Important limitation |

|---|---|---|

| Above estimated neutral | Policy may be restrictive because borrowing conditions are tighter than the estimated neutral benchmark. | The degree of restriction depends on inflation, growth, credit, expectations, and model uncertainty. |

| Near estimated neutral | Policy may be closer to neither stimulating nor restraining the economy. | “Near neutral” is still an estimate, not a precise point. |

| Below estimated neutral | Policy may be accommodative because borrowing conditions are easier than the estimated neutral benchmark. | Markets may still tighten through credit spreads, liquidity stress, or risk aversion. |

The neutral rate therefore helps describe policy stance, but it does not describe the entire transmission path. Inflation expectations, term premiums, credit conditions, bank lending, liquidity, and global capital flows can all change how a given policy rate affects the economy and markets.

What the Neutral Rate Is and Is Not

The neutral rate is useful only when its boundaries are clear. It is a conceptual benchmark for policy interpretation, not a promise about future interest rates.

| The neutral rate is | The neutral rate is not |

|---|---|

| An estimated benchmark for judging policy stance. | A directly observable market price. |

| A model-based concept used in policy discussion. | A precise current number that settles policy debate. |

| A way to discuss whether policy may be restrictive or accommodative. | A Fed forecast or official promise of where rates will go. |

| A long-run concept that can shift as the economy changes. | The same thing as the terminal rate, dot plot, or market-implied rate path. |

What Can Move Neutral-Rate Estimates

Neutral-rate estimates can change because the economy’s underlying structure changes. A higher expected return on investment, stronger productivity growth, larger fiscal borrowing needs, or shifts in savings behavior can affect where economists estimate neutral to be. Demographics, global capital flows, inflation expectations, and risk preferences can also matter.

These drivers do not move the neutral rate mechanically or instantly. They affect the assumptions used in models and the broader interpretation of whether a given policy rate is restraining or supporting activity.

Important nuance: a higher neutral-rate estimate does not automatically mean rates must rise. A lower estimate does not automatically mean cuts are coming. Policy still depends on inflation, employment, financial conditions, and the central bank’s reaction function.

Common False Reading: Neutral Rate as a Market Signal

A frequent mistake is treating the neutral rate as if it directly predicts bonds, equities, currencies, or commodities. It does not. The neutral rate helps frame policy conditions, but markets also respond to earnings expectations, real yields, liquidity, credit spreads, risk appetite, positioning, and valuation.

For example, if investors believe the neutral rate is higher than previously assumed, they may reassess how restrictive a given policy rate really is. That can affect the interpretation of real yields and financial conditions. But the neutral-rate estimate alone still does not say whether risk assets should rise or fall.

Market-use limitation: neutral-rate analysis is context, not a trade signal. It belongs inside a broader policy, liquidity, and risk-environment framework.

Neutral Rate vs Related Concepts

The neutral rate is often confused with nearby rate-policy concepts. The distinctions matter because each concept answers a different question.

| Concept | What it means | How it differs from the neutral rate |

|---|---|---|

| Real interest rate | An interest rate adjusted for inflation. | It can be observed or estimated from nominal rates and inflation measures, while the neutral rate is a model-based policy benchmark. |

| Fed terminal rate | The expected peak policy rate in a tightening cycle. | The terminal rate is cycle-specific, while the neutral rate is a broader estimate of neither-stimulative-nor-restrictive policy. |

| Fed dot plot | A summary of individual Federal Reserve policymakers’ rate projections. | The dot plot is a projection surface, while the neutral rate is an estimated policy benchmark. |

| Dovish / hawkish | Language describing easier-policy or tighter-policy bias. | Policy tone can change even when neutral-rate estimates are uncertain or unchanged. |

Illustrative Scenario

Assume a central bank’s policy rate is 5%, while several model estimates place the neutral rate somewhere around 3% to 4%. In that scenario, policy may be described as restrictive because the actual rate sits above the estimated neutral range. That description still does not prove that inflation will fall quickly, that the central bank will cut rates, or that markets will rally.

The same policy rate can have different effects depending on credit growth, inflation persistence, labor-market strength, financial conditions, and global liquidity. The neutral rate helps organize the question, but it does not answer every market or policy question by itself.

FAQ

What is the neutral rate of interest?

The neutral rate of interest is the estimated interest rate consistent with stable inflation and an economy operating near potential, where policy is neither stimulating nor restraining activity.

Is the neutral rate directly observable?

No. The neutral rate is inferred from models, data, and assumptions. It is not directly visible in market prices or central-bank statements.

Is the neutral rate the same as r-star?

In many policy discussions, r-star refers to the neutral real interest rate. The terms are closely related, but usage can vary depending on whether the discussion focuses on nominal or real rates.

Is the neutral rate the same as the terminal rate?

No. The terminal rate refers to the expected peak policy rate in a specific tightening cycle. The neutral rate is a broader estimated benchmark for policy stance.

Does the neutral rate predict Fed policy?

No. Neutral-rate estimates can inform policy discussion, but they should not be treated as an official Fed forecast, a rate target, or a promise of future policy action.

Does a high neutral rate predict market direction?

No. A neutral-rate estimate can help frame policy conditions, but market direction depends on many other variables, including growth, inflation, credit, liquidity, earnings expectations, and positioning.