Sterilized and unsterilized intervention are both categories of FX intervention, but they differ by what happens to the domestic liquidity effect after the FX transaction. If the central bank offsets the domestic money-market or monetary-base effect, the intervention is sterilized. If that effect is left in place, it is unsterilized. The classification is about the liquidity channel, not a guarantee of exchange-rate direction.

| Comparison point | Sterilized intervention | Unsterilized intervention |

|---|---|---|

| Starting FX action | Begins with a central-bank transaction in the FX market. | Begins with a central-bank transaction in the FX market. |

| Offset operation | The domestic liquidity effect is offset through another domestic operation. | The domestic liquidity effect is not offset. |

| Domestic money-market effect | The intended money-market impact is neutralized or contained. | Money-market conditions may change because the liquidity effect remains. |

| Monetary-base effect | The direct monetary-base effect is offset. | The monetary-base effect is allowed to remain. |

| Liquidity interpretation | Read as an FX operation with an offsetting domestic-liquidity check. | Read as an FX operation that also changes the domestic liquidity channel. |

| Common false reading | Assuming sterilized means irrelevant. | Assuming unsterilized means an automatic currency move. |

| Market-structure boundary | Can still matter through expectations, signaling, portfolio-balance effects, or credibility. | Can affect liquidity conditions, but does not become a standalone forecast. |

Why the same FX action can lead to two classifications

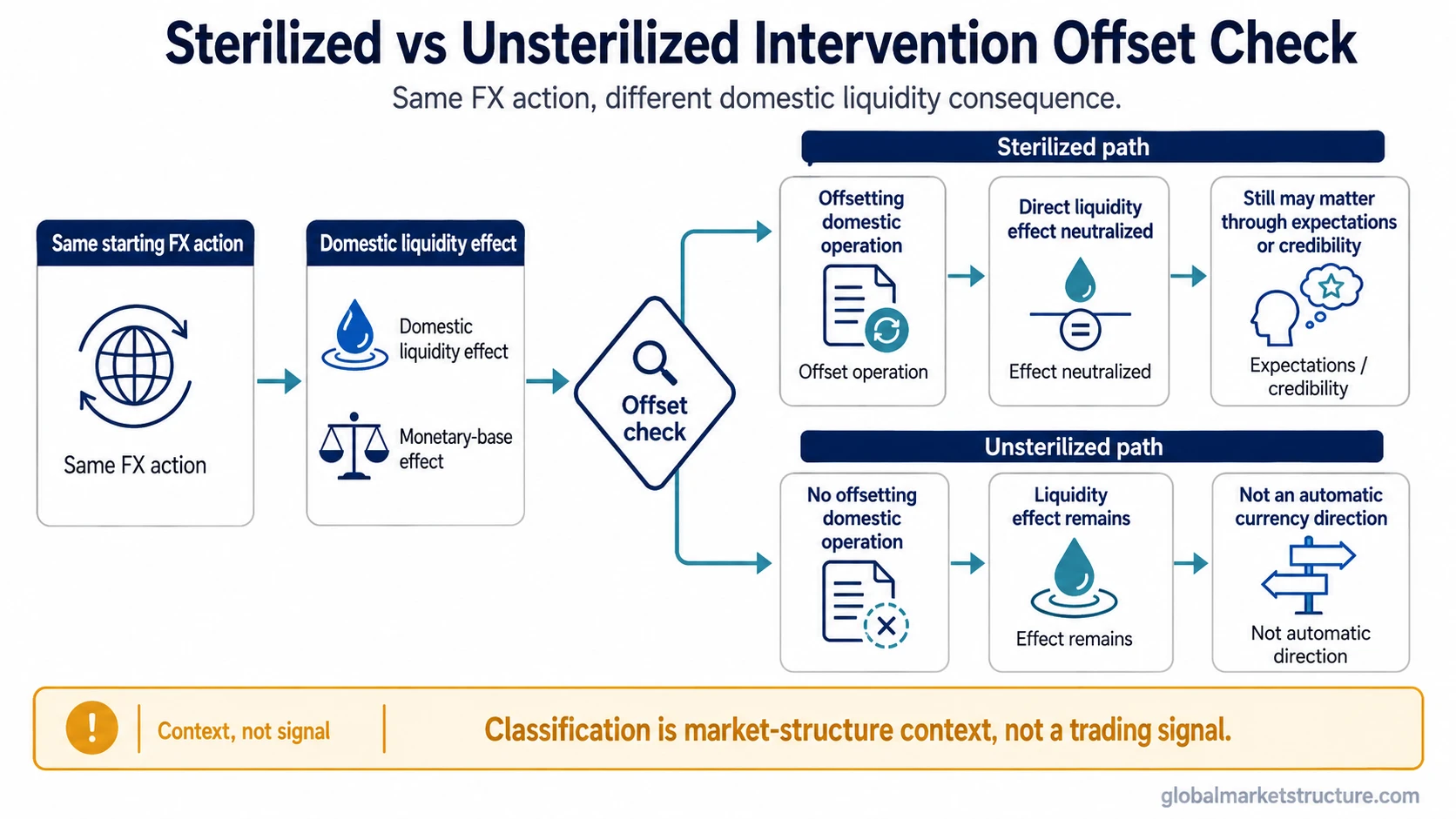

The first step can look identical. A central bank may enter the FX market to buy or sell currency. That action belongs to the broader category of foreign exchange intervention. The sterilized versus unsterilized label comes after that first step, when the domestic liquidity consequence is either offset or left in the system.

Core distinction: the comparison is not about whether reserves are involved and not about whether the exchange rate moves. It is about whether the central bank offsets the domestic money-market or monetary-base effect created by the intervention.

An FX operation can affect two channels at once. One channel is the exchange-rate or reserve channel. The other is the domestic money-market channel. Sterilization is the attempt to separate those channels by neutralizing the domestic liquidity effect.

The offset check is the main separation point

A sterilized intervention normally includes an offsetting domestic operation. For example, if an FX purchase adds domestic liquidity, a separate domestic operation may withdraw liquidity so that money-market conditions are not changed in the same way. The FX operation still happened, but its direct domestic-liquidity effect has been neutralized.

An unsterilized intervention leaves that domestic effect in place. The FX transaction can then influence the monetary base, bank reserves, or money-market conditions, depending on the operating framework. That does not mean the exchange rate must move in a fixed direction. It means the intervention has not been separated from the domestic liquidity channel.

Money-market criterion: in a modern operating framework, the practical question is often whether the intervention changes domestic money-market conditions or short-term rate pressure after any offsetting operation. A simple reserve-only reading can miss that operating distinction.

Same-scenario comparison

Starting scenario: a central bank buys foreign currency and sells domestic currency.

Sterilized path: the central bank offsets the domestic liquidity effect through a separate domestic operation. The FX transaction remains part of reserve and exchange-rate management, but the direct monetary-base or money-market effect is neutralized.

Unsterilized path: the central bank does not offset the domestic liquidity effect. The domestic liquidity impact remains, so money-market conditions or the monetary base may change as part of the intervention’s transmission.

The same initial action cannot be classified from the FX transaction alone. The classification depends on what happens next in domestic operations.

Why sterilized intervention can still matter

Sterilized intervention does not mean the market should ignore the operation. It means the direct domestic liquidity effect has been offset. The intervention may still matter through signaling, expectations, portfolio-balance effects, or the credibility of the policy action.

The safer reading is narrow: sterilization limits one transmission channel, but it does not remove every possible market channel. A sterilized operation can still change how participants interpret the policy stance, reserve-management intent, or the authorities’ willingness to act.

Interpretation boundary: sterilized intervention is not “no market effect.” It is “no direct unoffset domestic liquidity effect.” That difference protects the analysis from treating a technical classification as proof that the operation cannot influence expectations or asset allocation.

Why unsterilized intervention is not an automatic currency forecast

Unsterilized intervention leaves the domestic liquidity effect in place, so it can be more directly connected to money-market conditions or the monetary base. That makes the liquidity channel more relevant, but it still does not create a mechanical exchange-rate forecast.

The exchange-rate response can depend on credibility, scale, timing, market positioning, policy consistency, reserve capacity, capital-flow pressure, and the broader macro environment. The classification identifies which channel remains open. It does not prove that the currency must rise or fall.

False-reading warning: unsterilized intervention is not a trading signal. It is a classification of how the intervention interacts with domestic liquidity and money-market conditions.

Common mistakes when reading the distinction

| Mistake | Cleaner reading |

|---|---|

| Sterilized means no effect. | Sterilized means the direct domestic liquidity effect is offset. Other channels may still matter. |

| Unsterilized means the exchange rate must move. | Unsterilized means the domestic liquidity effect remains. Exchange-rate direction still depends on broader conditions. |

| Reserve movement alone proves the classification. | The classification depends on the offset and domestic money-market consequence, not reserves alone. |

| Intervention type is a market signal. | The type is market-structure context. It needs policy, liquidity, positioning, and macro confirmation before interpretation. |

How reserves fit into the comparison

Foreign-currency assets and reserve operations can be part of the intervention process, but reserve involvement is not the same as the sterilized versus unsterilized distinction. The broader role of foreign exchange reserves is to show the official asset base available for external liquidity, intervention capacity, and sovereign-flow context.

Reserve involvement is secondary to the offset check. The classification turns on whether the authority neutralizes the money-market or monetary-base effect, or allows that domestic liquidity effect to remain.

FAQ

Does sterilized intervention mean there is no market impact?

No. Sterilized intervention means the direct domestic liquidity or monetary-base effect is offset. The operation can still matter through signaling, expectations, portfolio-balance effects, or policy credibility.

Can the same FX intervention be sterilized or unsterilized?

Yes. The same initial FX action can receive either classification depending on whether the domestic money-market or monetary-base effect is offset after the transaction.

Is unsterilized intervention a trading signal?

No. Unsterilized intervention leaves the domestic liquidity effect in place, but it does not automatically determine currency direction or create a standalone market signal.

Is the difference based only on foreign exchange reserves?

No. Reserves can be involved in intervention, but the sterilized versus unsterilized distinction depends on the offset operation and the domestic liquidity consequence.