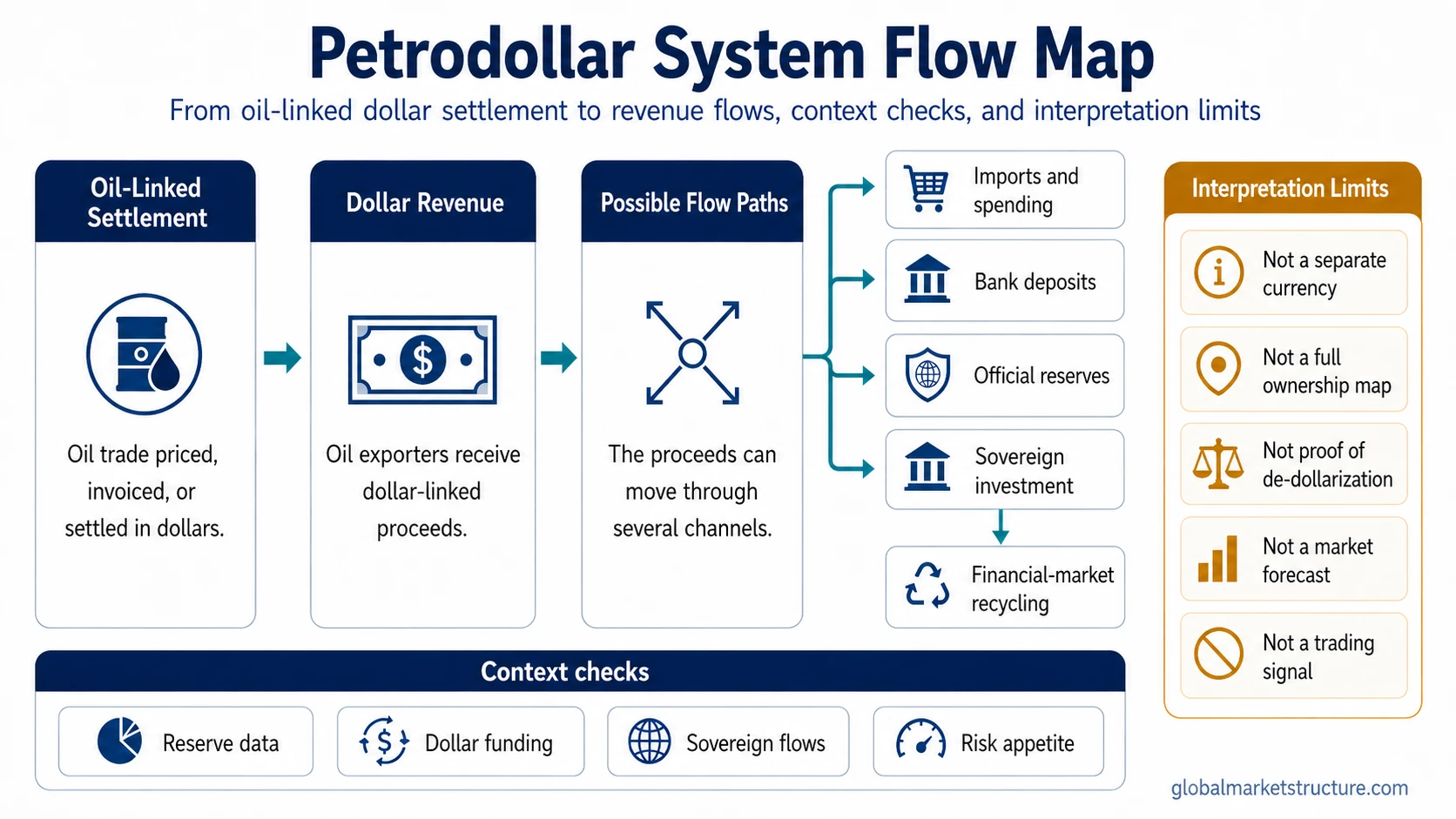

The petrodollar system is the use of U.S. dollars in oil-linked trade settlement and oil-export revenue flows, creating a connection between energy markets, reserve behavior, dollar liquidity, and sovereign capital flows. It should not be treated as a separate currency, a synonym for petrodollar recycling, a complete map of global dollar ownership, or a standalone signal for de-dollarization, yields, currencies, or risk assets.

Key Points

- The petrodollar system describes the dollar-centered role of oil trade, oil-export revenue, and related reserve or investment flows.

- Its market-structure relevance comes from the way oil-linked dollar receipts can interact with reserves, offshore dollar liquidity, capital recycling, and sovereign-flow behavior.

- Petrodollar recycling is related, but narrower. It focuses on how oil-export dollar proceeds are reinvested or recycled through financial markets.

- The concept should not be read as proof that the dollar must stay dominant, that de-dollarization is happening, or that a specific market move will follow.

- The useful reading is conditional: petrodollar flows matter most when they are interpreted alongside reserve changes, dollar funding pressure, sovereign capital behavior, and broader risk appetite.

What the Petrodollar System Means

The petrodollar system is a market-structure label for the role of U.S. dollars in oil-linked settlement and oil-export revenue flows. When oil trade is priced, invoiced, or settled in dollars, oil importers need dollars and oil exporters receive dollar revenues. Those revenues may then be held, spent, deposited, invested, or recycled through the global financial system.

The concept is most useful in capital-flow and reserve-flow analysis because it links energy trade to dollar liquidity, reserve management, offshore dollar demand, and sovereign capital behavior. It is less useful as a slogan about dollar power and more useful as a way to organize how energy-linked dollar flows can move through the financial system.

Definition: The petrodollar system refers to the dollar-centered structure around oil-linked trade settlement and oil-export revenue flows. It connects oil markets, dollar demand, reserve behavior, and sovereign capital-flow interpretation, but it does not by itself prove a market forecast or policy outcome.

What It Is and What It Is Not

The most common mistake is treating the petrodollar system as a single formal object. In practice, it is better understood as a system label for related flows, incentives, and balance-sheet choices around oil-linked dollar revenue.

| Question | Correct Interpretation | Limit |

|---|---|---|

| Is the petrodollar a separate currency? | No. It refers to dollars connected to oil trade and oil-export revenue flows. | Do not treat it as a currency distinct from the U.S. dollar. |

| Does it explain all dollar dominance? | No. It is one part of the broader dollar system, alongside reserves, funding markets, trade finance, debt markets, and institutional demand. | Oil-linked settlement alone does not explain the full global role of the dollar. |

| Is it the same as petrodollar recycling? | No. The system is the broader oil-dollar flow context. Recycling is the reinvestment or redeployment of oil-export dollar proceeds. | Do not turn this page into a full recycling article. |

| Does it prove de-dollarization? | No. Changes in oil settlement or reserve behavior may be relevant, but they need broader evidence. | No single headline, settlement change, or reserve move proves a structural dollar shift. |

How the Petrodollar System Works

The mechanism starts with the dollar role in oil-linked trade. If oil importers need dollars to settle energy purchases, demand for dollar funding can rise through trade finance, banking channels, or offshore dollar markets. Oil exporters then receive dollar revenues, which create a separate set of choices: hold the dollars, use them for imports, place them in deposits, accumulate reserve assets, invest through sovereign channels, or recycle them into financial markets.

Mechanism sequence:

- Oil importers need dollars for dollar-priced, dollar-invoiced, or dollar-settled oil trade.

- Oil exporters receive dollar revenues from energy sales.

- Those dollar revenues may be spent, held, deposited, invested, or recycled.

- Some flows may interact with reserve accumulation, sovereign investment behavior, Treasury demand, bank deposits, or offshore dollar liquidity.

- The market-structure interpretation depends on wider context, including dollar funding pressure, reserve behavior, risk appetite, and sovereign-flow conditions.

This sequence is useful because it separates observed flow mechanics from interpretation. Oil-linked dollar revenue can be a source of dollar liquidity in some conditions, but it can also sit inside reserves, move through banking systems, or be invested through sovereign channels. The same broad label can therefore describe several different balance-sheet outcomes.

Petrodollar System vs Petrodollar Recycling

The petrodollar system is the broader oil-dollar structure. Petrodollar recycling is the narrower process in which oil-export dollar proceeds are reinvested, redeposited, or otherwise routed back through financial markets.

Simple distinction: the petrodollar system explains why oil-linked dollar flows exist; petrodollar recycling explains what can happen to those dollar proceeds after oil exporters receive them.

This distinction matters because recycling is only one possible outcome. Some proceeds may support reserves, some may fund imports, some may move through banks, some may be invested through sovereign vehicles, and some may be used domestically. Treating every oil-export dollar as recycled into the same market creates a false precision that the concept does not support.

Why It Matters for Dollar Liquidity and Reserve Flows

The petrodollar system connects a real-economy commodity flow to dollar balance sheets. When oil-linked dollar revenues rise, the question is not only whether oil was sold in dollars. The more important question is where those dollars go next and whether they change liquidity, reserve, funding, or capital-flow conditions.

For official-sector analysis, the concept overlaps with foreign-exchange reserves when oil-export revenues are held or managed as official reserve assets. For market interpretation, the flow becomes more relevant when it coincides with reserve accumulation or drawdown, offshore dollar stress, sovereign capital recycling, or changes in global risk appetite.

| Observable Context | Possible Interpretation | Required Limitation |

|---|---|---|

| Oil-export revenue increases | Dollar receipts may rise for some exporters. | This does not prove where the dollars are invested or held. |

| Official reserves increase | Some dollar revenues may be retained in reserve assets. | Reserve changes can reflect many causes, not only oil flows. |

| Dollar funding pressure rises | Oil-linked settlement demand may become more visible in offshore dollar conditions. | Funding stress cannot be attributed to petrodollars alone. |

| Sovereign flows into dollar assets increase | Oil-export proceeds may be one possible flow source. | Do not infer direct causality without flow evidence. |

Common Misreadings of the Petrodollar System

A common misreading is that the petrodollar system mechanically guarantees dollar dominance. That is too strong. Oil-linked dollar settlement can support dollar demand under some conditions, but the dollar system also depends on Treasury market depth, global funding markets, trade finance, reserve management, institutional behavior, legal infrastructure, and network effects.

Another misreading is that any move away from dollar settlement in some oil trade proves de-dollarization. Settlement changes may be relevant, but the stronger question is whether they scale across trade, reserves, debt issuance, funding markets, collateral systems, and institutional portfolios. Without that wider evidence, the claim remains incomplete.

False reading to avoid: The petrodollar system should not be used as a single-cause explanation for dollar moves, Treasury yields, oil prices, equity risk appetite, or reserve shifts. It is a conditional input for market-structure interpretation, not a complete causal model.

A Practical Market-Structure Scenario

Consider a generic oil-exporting economy during a period of strong oil-export revenue. It receives more dollar income from energy sales. Some of those dollars may be used for imports, some may remain in bank deposits, some may be added to official reserves, and some may be invested through sovereign channels. The petrodollar system helps organize that flow path, but it does not prove the final destination of every dollar.

The interpretation becomes more useful if the same period also shows reserve accumulation, calmer offshore dollar funding conditions, or visible sovereign demand for dollar assets. It becomes weaker if reserve data is mixed, dollar funding stress is coming from unrelated banking pressure, or oil-export proceeds are being used mainly for domestic fiscal needs rather than external asset accumulation.

Illustrative scenario: Oil-linked dollar revenue may support dollar liquidity if the proceeds are deposited, invested, or accumulated in reserve assets. The same revenue may have a different market effect if it is spent on imports, used to stabilize domestic balances, or held outside observable market channels. The concept is useful only when the flow path is interpreted with other evidence.

What the Petrodollar System Can and Cannot Tell You

The petrodollar system can help explain why oil-linked trade has mattered as one input in dollar demand, reserve behavior, and sovereign capital-flow analysis. It can also help frame why energy exporters, reserve managers, banks, and sovereign investors may affect offshore dollar liquidity under some conditions.

By itself, the concept does not determine whether the dollar will rise or fall, whether Treasury yields will move in a specific direction, whether oil prices will change, or whether risk assets will rally or decline. It also cannot establish policy intervention, de-dollarization, or the end of dollar dominance without stronger supporting evidence.

| It Can Help With | It Cannot Prove Alone |

|---|---|

| Understanding oil-linked dollar settlement and revenue flows. | A complete map of global dollar ownership. |

| Framing reserve and sovereign-flow context. | That a reserve change came from oil revenues. |

| Connecting energy trade to dollar liquidity conditions. | A forecast for DXY, yields, equities, gold, oil, or crypto. |

| Separating flow mechanics from market narratives. | That de-dollarization is happening from one settlement headline. |

Related Concepts

The closest related concept is petrodollar recycling, which focuses on how oil-export dollar proceeds may be reinvested or redeployed after they are received. That topic is narrower than the full petrodollar system because it starts after the dollar revenue has already been earned.

Foreign-exchange reserves are the other core related concept. They explain the official reserve-asset side of the structure, including how central banks and monetary authorities may hold and manage foreign-currency assets. The petrodollar system can feed into that reserve context, but it should not replace a dedicated reserve analysis.

FAQ

What is the petrodollar system?

The petrodollar system is the dollar-centered structure around oil-linked trade settlement and oil-export revenue flows. It connects oil markets, dollar demand, reserve behavior, and sovereign capital flows, but it is not a separate currency or a market forecast.

Is the petrodollar system the same as petrodollar recycling?

No. The petrodollar system is the broader oil-dollar settlement and revenue-flow structure. Petrodollar recycling is the narrower process in which oil-export dollar proceeds are reinvested, redeposited, or routed back through financial markets.

Does the petrodollar system prove dollar dominance?

No. It can help explain one source of dollar demand, but dollar dominance also depends on funding markets, reserve management, trade finance, debt markets, institutional behavior, legal infrastructure, and network effects.

Does a change in oil settlement prove de-dollarization?

No. A settlement change may be relevant, but de-dollarization requires broader evidence across trade, reserves, debt, funding markets, collateral systems, and institutional portfolios. One headline is not enough.

Can the petrodollar system predict markets?

No. It is not a trading signal and does not predict DXY, Treasury yields, equities, oil, or risk assets by itself. It is a conditional market-structure input that must be interpreted alongside other evidence.