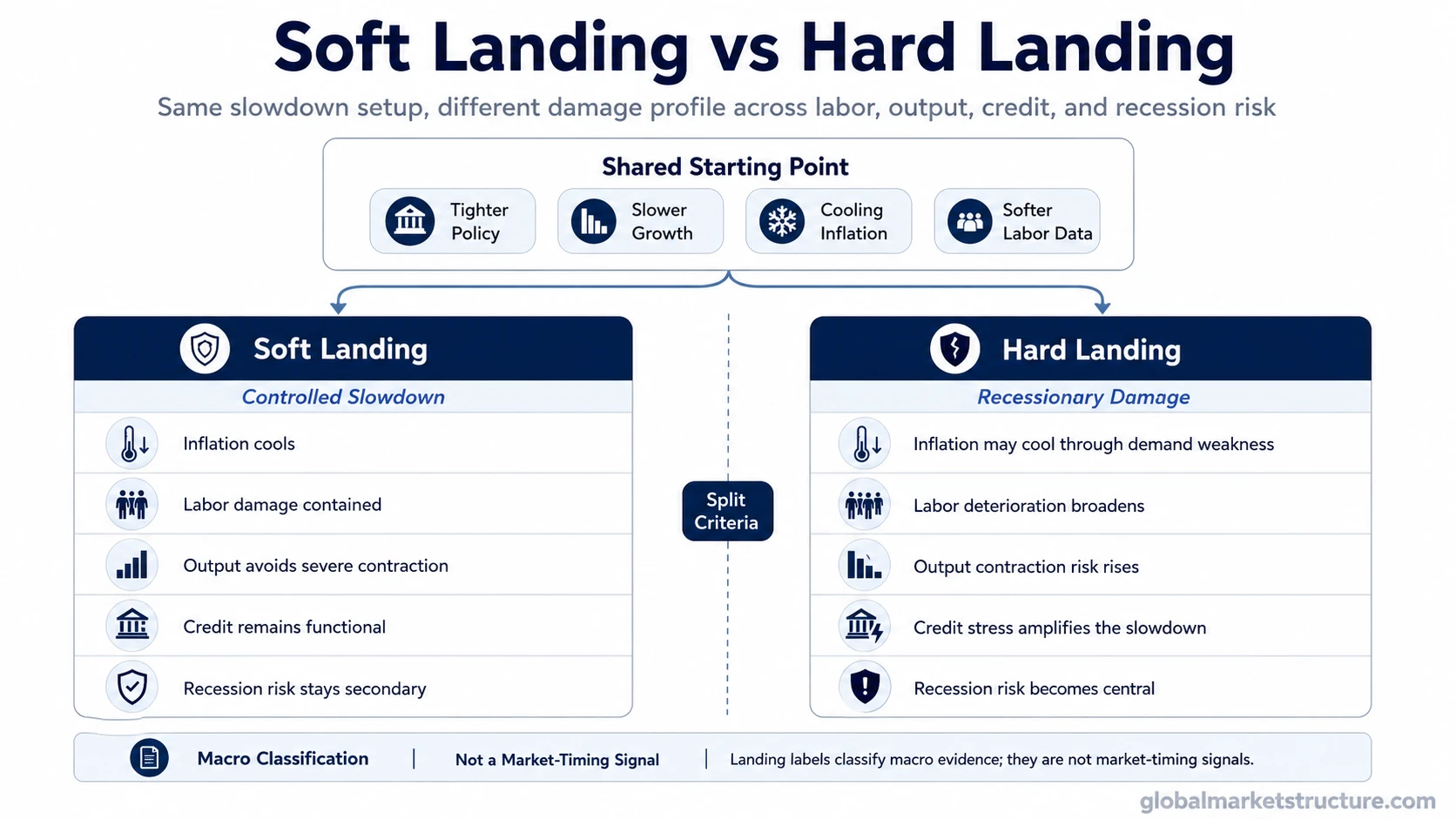

Soft landing and hard landing can begin from the same macro setup: inflation pressure, tighter policy, slower growth, and cooling labor data. The difference is whether the slowdown remains controlled or becomes recessionary. A soft landing keeps labor, credit, and output damage contained; a hard landing makes that damage central. Neither label is a confirmed market-timing signal while evidence remains mixed.

The shortest distinction is this: a soft landing describes a controlled slowdown where inflation cools without severe recessionary damage, while a hard landing describes a slowdown where recessionary damage becomes the dominant feature.

Key Points

- Both labels can start from similar macro conditions: tighter policy, slower activity, cooling inflation, and weaker forward expectations.

- The distinction depends on damage severity across labor, output, credit, and recession risk.

- Landing labels help classify the macro environment, but they do not create direct asset-price signals.

Soft Landing vs Hard Landing: Core Difference

A soft landing is a controlled deceleration. Growth slows, inflation pressure cools, and policy restraint works without causing broad economic damage. The economy may lose momentum, but the labor market, credit system, and output path remain stable enough to avoid a severe contraction.

A hard landing is a damaging deceleration. Policy restraint, weaker demand, or tighter financial conditions push the economy into a more recessionary pattern. Labor weakness becomes more visible, output risk rises, and credit conditions can turn from a background concern into a central stress point.

One-sentence distinction: A soft landing is slower growth with contained damage; a hard landing is slower growth where recessionary damage becomes the main interpretation.

Comparison Criteria

The difference is not decided by one data release. A cleaner comparison looks at whether several parts of the macro system are cooling in an orderly way or deteriorating together.

| Criterion | Soft landing interpretation | Hard landing interpretation |

|---|---|---|

| Growth | Growth slows but does not collapse into broad contraction. | Growth weakens enough that contraction risk becomes central. |

| Inflation | Inflation pressure cools without forcing severe economic damage. | Inflation may cool because demand is weakening sharply or stress is rising. |

| Policy | Policy restraint slows the economy without breaking key transmission channels. | Policy restraint or lagged tightening contributes to a more damaging slowdown. |

| Labor market | Hiring cools, wage pressure moderates, and unemployment damage stays limited. | Job losses, unemployment pressure, or labor weakness become harder to dismiss. |

| Output / GDP | Output growth may slow, but recessionary contraction is avoided or remains limited. | Output contraction or recessionary deterioration becomes a primary signal. |

| Credit conditions | Credit stays functional even if borrowing becomes more restrictive. | Credit stress, tighter lending, or wider risk premiums amplify the downturn. |

| Recession risk | Risk exists, but the evidence still supports controlled deceleration. | Recession risk moves from possible background risk to the central macro reading. |

| Market interpretation | The label can support a constructive macro reading, but it is not a buy signal. | The label can support a defensive macro reading, but it is not a sell signal. |

Why Both Can Look Similar at First

Soft and hard landings can look similar early because the same indicators often move first. Inflation may slow, growth data may cool, job openings may decline, and policy-sensitive sectors may soften. Those changes do not automatically prove that the economy is landing gently or breaking into recession.

The early phase is confusing because cooling is required for a soft landing, but excessive cooling can also be the start of a hard landing. The same slowdown can therefore carry two possible meanings until labor damage, credit stress, and output behavior provide clearer confirmation.

Interpretation boundary: A cooling economy is not enough by itself. The key question is whether the cooling remains orderly or starts to damage the parts of the economy that usually turn a slowdown into a recessionary process.

Same Scenario, Different Landing Reading

Consider a general scenario where inflation cools and growth slows after a period of tighter policy. In a soft-landing reading, the slowdown is visible but contained. Hiring moderates without a severe labor break, credit remains available, and output avoids recessionary contraction. The economy loses speed, but the damage does not become self-reinforcing.

In a hard-landing reading, the same starting point develops differently. Labor weakness accelerates, credit becomes harder to access, output contracts, and risk appetite deteriorates because the slowdown is no longer just controlled cooling. The label changes because the damage profile changes.

Practical distinction: Cooling inflation and slower growth can fit either label at the start. The interpretation depends on whether labor, credit, and output remain resilient or begin confirming recessionary deterioration.

Common False Readings

A single CPI print does not prove a soft landing. A single weak payroll report does not prove a hard landing. A rally in equities, a drop in yields, or a short-term move in credit spreads can all be part of a larger interpretation, but none of them is enough to settle the landing label alone.

The mistake is treating the label as a signal instead of a macro classification. Landing language is useful when it organizes evidence across growth, labor, policy, credit, and output. It becomes risky when it is used as a shortcut for market timing or portfolio action.

Common mistake: Reading one strong or weak data point as final proof. Landing outcomes are judged by a pattern of evidence, not by one release or one market reaction.

What Changes the Interpretation

The interpretation moves closer to a soft landing when inflation cools while labor damage stays contained, credit continues functioning, and output avoids broad contraction. In that setting, tighter policy may have slowed demand without causing a deeper recessionary break.

The interpretation moves closer to a hard landing when labor deterioration broadens, credit conditions tighten, output contracts, and policy lags keep pressure on the economy after the slowdown is already visible. Cross-asset behavior can add context when credit, yields, equity leadership, and risk appetite begin telling the same story, but that still does not convert the label into a mechanical trading signal.

| Signal area | Why it matters | Interpretation limit |

|---|---|---|

| Labor deterioration | It shows whether slower growth is starting to damage household income and demand. | One weak labor report can be noise unless the weakness broadens. |

| Credit stress | It shows whether financing conditions are amplifying the slowdown. | Credit signals need context because risk premiums can move for several reasons. |

| Output contraction | It separates mild deceleration from more recessionary behavior. | Initial output data can be revised and should not be read in isolation. |

| Policy lag | It explains why damage can appear after tightening has already slowed activity. | Lagged effects are uncertain in timing and magnitude. |

| Inflation persistence | It affects how much policy flexibility may exist during the slowdown. | Inflation cooling alone does not prove growth resilience. |

Where No Landing Fits

No landing is an adjacent label, not a substitute for the soft-versus-hard distinction. It usually refers to a situation where growth remains firmer than expected and the economy does not slow enough to fit either a clear soft landing or a clear hard landing. It matters because it can delay the landing debate or change the policy path, but it should not blur the core distinction between controlled slowdown and recessionary damage.

How the Comparison Should Be Interpreted

The useful way to use the comparison is to separate starting conditions from final damage. Inflation pressure, tighter policy, and slower activity describe the setup. Labor damage, output behavior, credit stress, and recession risk decide which label becomes more defensible.

That separation keeps the comparison from turning into a market call. A soft landing can still contain risks if inflation persists or policy stays restrictive. A hard landing can still be uncertain if credit remains stable and labor weakness does not broaden. The label should summarize a pattern of evidence, not replace the evidence.

FAQ

Is a soft landing the opposite of a hard landing?

Yes, but only in a controlled macro sense. A soft landing means the slowdown stays contained, while a hard landing means recessionary damage becomes central. Both can begin from similar conditions.

Can markets rise during a hard-landing debate?

They can, especially if investors focus on policy relief, lower yields, or future recovery. That does not prove the economy avoided hard-landing risk. Market reactions and macro outcomes are related, but they are not the same thing.

Does one weak data release prove a hard landing?

No. One weak release can raise concern, but a hard-landing interpretation needs broader confirmation across labor, output, credit, and recession-risk evidence.

Does cooling inflation prove a soft landing?

No. Cooling inflation is helpful for a soft-landing interpretation, but it is not enough by itself. The key issue is whether inflation cools without severe damage to labor, output, and credit conditions.