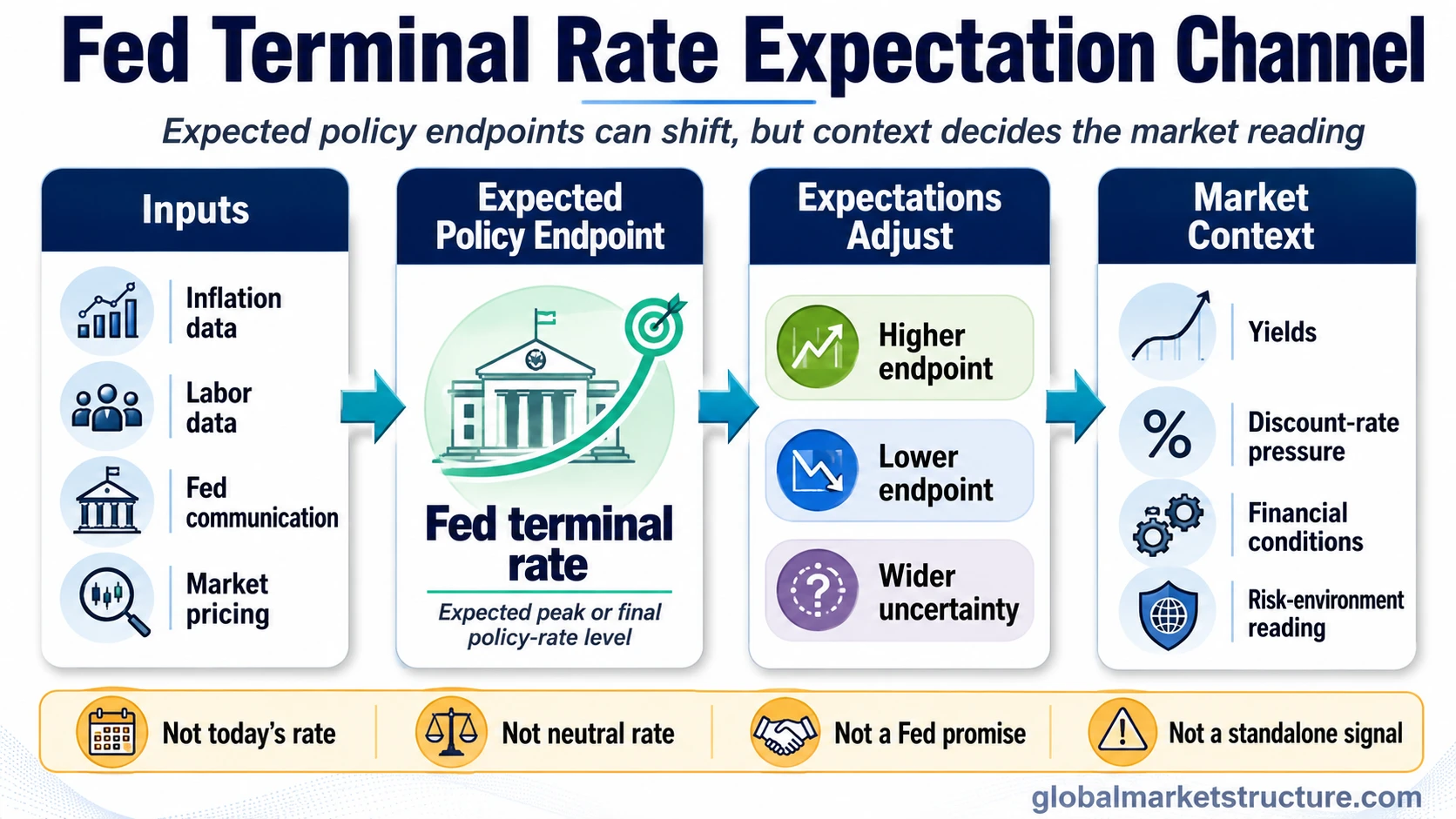

The Fed terminal rate is the expected peak or endpoint level of the federal funds rate in a policy cycle. It is a rate-path expectation, not the current Fed funds rate, not the neutral rate itself, not a Federal Reserve promise, and not a standalone signal for stocks, bonds, or risk assets.

- Fed terminal rate refers to the expected endpoint of the Fed’s policy-rate path in a tightening or easing cycle.

- It can change as inflation data, labor data, Fed communication, and market expectations change.

- It is different from the current federal funds rate, which describes where policy is set now.

- It is different from the neutral rate of interest, which is an estimate of where policy may be neither restrictive nor stimulative.

- Markets watch terminal-rate expectations because they can affect yield, discount-rate, and financial-conditions interpretation, but they do not determine asset direction by themselves.

Quick definition: Fed terminal rate means the expected final or peak policy-rate level that the Federal Reserve may reach before stopping, pausing, or later reversing a policy cycle. The useful reading is the expectation path, not a fixed number in isolation.

Fed Terminal Rate Is / Is Not

The fastest way to avoid confusion is to separate the terminal rate from nearby Fed concepts. The phrase describes where the policy-rate path is expected to end, not where the rate is today or what the Fed has guaranteed.

| Fed terminal rate is | Fed terminal rate is not |

|---|---|

| An expected endpoint or peak for the federal funds rate in a policy cycle. | The current federal funds rate or today’s policy setting. |

| A rate-path expectation that can move as data and Fed communication change. | A fixed promise that the Federal Reserve must deliver. |

| One input into how markets interpret policy restrictiveness, yields, and financial conditions. | A complete market-regime reading by itself. |

| A concept that can be influenced by projections, inflation trends, labor-market data, and market pricing. | The same thing as the neutral rate or a precise forecast of future asset returns. |

How Terminal-Rate Expectations Form

Terminal-rate expectations usually form through a mix of economic data, Federal Reserve communication, and market pricing. Inflation data can affect how restrictive markets think policy may need to become. Labor-market data can affect whether investors expect the Fed to keep rates higher, pause earlier, or eventually ease policy.

Fed communication also matters because the expected policy-rate destination is part of the broader monetary policy path. Speeches, meeting statements, press conferences, and Summary of Economic Projections material can all shape how markets think about the policy-rate destination.

- Economic data changes: inflation, employment, growth, and financial conditions alter the expected policy backdrop.

- Fed communication is interpreted: statements, projections, press conferences, and speeches can make the expected path sound more restrictive, more patient, or more open to easing.

- Expectations adjust: markets revise where they think the policy-rate path may peak or end.

- Cross-market interpretation shifts: yields, the curve, risk appetite, and financial conditions may reprice around the new expected path.

The terminal rate is therefore best read as a conditional expectation. It can rise, fall, or become more uncertain without turning into a guaranteed policy setting.

Fed Terminal Rate vs Current Rate, Neutral Rate, and Dot Plot

Several Fed-related terms can appear in the same discussion, but they answer different questions. Mixing them together can make the terminal rate sound more certain than it is.

| Concept | What it describes | Main confusion to avoid |

|---|---|---|

| Fed terminal rate | The expected endpoint or peak of the federal funds rate path in a policy cycle. | Do not treat it as today’s rate or a guaranteed future setting. |

| Current federal funds rate | The current policy-rate setting or effective federal funds rate environment observed now. | Do not confuse the current setting with the expected end point of the rate path. |

| Neutral rate of interest | An estimate of the rate level that may be neither stimulative nor restrictive for the economy. | Do not assume the terminal rate equals neutral; terminal can sit above or below neutral depending on the cycle. |

| Fed dot plot | A projection display inside the Fed’s Summary of Economic Projections, showing policymakers’ individual rate projections. | Do not treat dots as promises; they are conditional projections that can influence expectations. |

A terminal-rate discussion can include hawkish or dovish policy language, but the term itself is narrower. A hawkish policy tone may push markets to consider a higher or later endpoint, while a softer tone may reduce that expectation. The final interpretation still depends on data, credibility, financial conditions, and market pricing.

Why Markets Watch Terminal-Rate Expectations

Markets watch terminal-rate expectations because the expected policy endpoint can influence how investors read yields, discount rates, financing conditions, and risk appetite. A higher expected endpoint can make policy look more restrictive. A lower expected endpoint can make policy look less restrictive. Neither reading is complete without the surrounding macro and market-structure context.

The relationship is especially important for rate-sensitive markets because terminal-rate repricing can affect the front end of the rate curve and the broader yield curve. Even then, the curve’s message depends on more than the terminal-rate estimate alone. Growth expectations, inflation risk, term premium, liquidity conditions, and credit stress can all change the market reading.

Limitation: Terminal-rate expectations are useful for interpreting the expected policy path. They do not prove what the Fed will do, and they do not provide a direct answer for whether equities, bonds, the dollar, or risk assets should rise or fall.

Illustrative Scenario: Terminal-Rate Repricing

A common scenario is that inflation or labor-market data comes in stronger than expected. Markets may then raise the expected terminal rate because investors think the Fed may need to keep policy tighter for longer or move the projected path endpoint higher than previously expected.

That repricing does not mean the Fed has promised the new endpoint. It also does not decide market direction by itself. The same upward shift in terminal-rate expectations can be interpreted differently depending on whether growth remains resilient, credit conditions stay calm, liquidity tightens, or risk appetite deteriorates.

The practical value is the sequence: data changes expectations, expectations change the perceived policy path, and the policy path changes how markets interpret rates and financial conditions. The terminal-rate estimate is one part of that chain.

Common Mistakes When Reading the Fed Terminal Rate

| Mistake | Better interpretation |

|---|---|

| Treating the terminal rate as the current Fed funds rate. | The current rate describes today’s policy setting; the terminal rate describes the expected end point of the rate path. |

| Treating the terminal rate as the neutral rate. | Neutral is an equilibrium-rate estimate; terminal is a cycle-specific policy-rate expectation. |

| Treating the dot plot as a promise. | Dot plot projections can influence expectations, but they remain conditional and can change. |

| Reading terminal-rate repricing as a market signal. | Terminal-rate expectations need confirmation from yields, credit, liquidity, growth, inflation, and risk-environment context. |

| Using one terminal-rate estimate without checking uncertainty. | The distribution of expectations can matter as much as the headline level, especially when data is mixed. |

Related Concepts

The Fed terminal rate sits inside the rates and policy-expectations layer of market structure. Monetary policy explains the broader stance, the Fed dot plot shows a projection format, the neutral rate describes an estimated equilibrium rate, and the yield curve shows how rate expectations appear across maturities.

Use the terminal-rate concept when the question is about the expected endpoint of the policy-rate path. Use the dot plot when the question is about the Fed projection display. Use the neutral rate when the question is about the estimated equilibrium rate. Use the yield curve when the question is about how rate expectations appear across maturities.

FAQ

What is the Fed terminal rate?

The Fed terminal rate is the expected peak or endpoint level of the federal funds rate in a policy cycle. It is a rate-path expectation, not a fixed promise or today’s policy rate.

Is the Fed terminal rate the same as the current Fed funds rate?

No. The current Fed funds rate describes where policy is set now. The Fed terminal rate describes where markets or policymakers may expect the policy-rate path to end in the current cycle.

Is the terminal rate the same as the neutral rate?

No. The neutral rate is an estimate of the rate that may be neither restrictive nor stimulative. The terminal rate is a cycle-specific expectation for the endpoint or peak of the Fed’s policy-rate path.

Does the Fed dot plot promise the terminal rate?

No. The dot plot can influence terminal-rate expectations because it shows individual policy-rate projections, but those projections are conditional and can change as economic data changes.

Can the Fed terminal rate predict stocks or bonds?

No. Terminal-rate expectations can affect how markets interpret yields, discount rates, and financial conditions, but they are not a standalone forecast for stocks, bonds, or other assets.