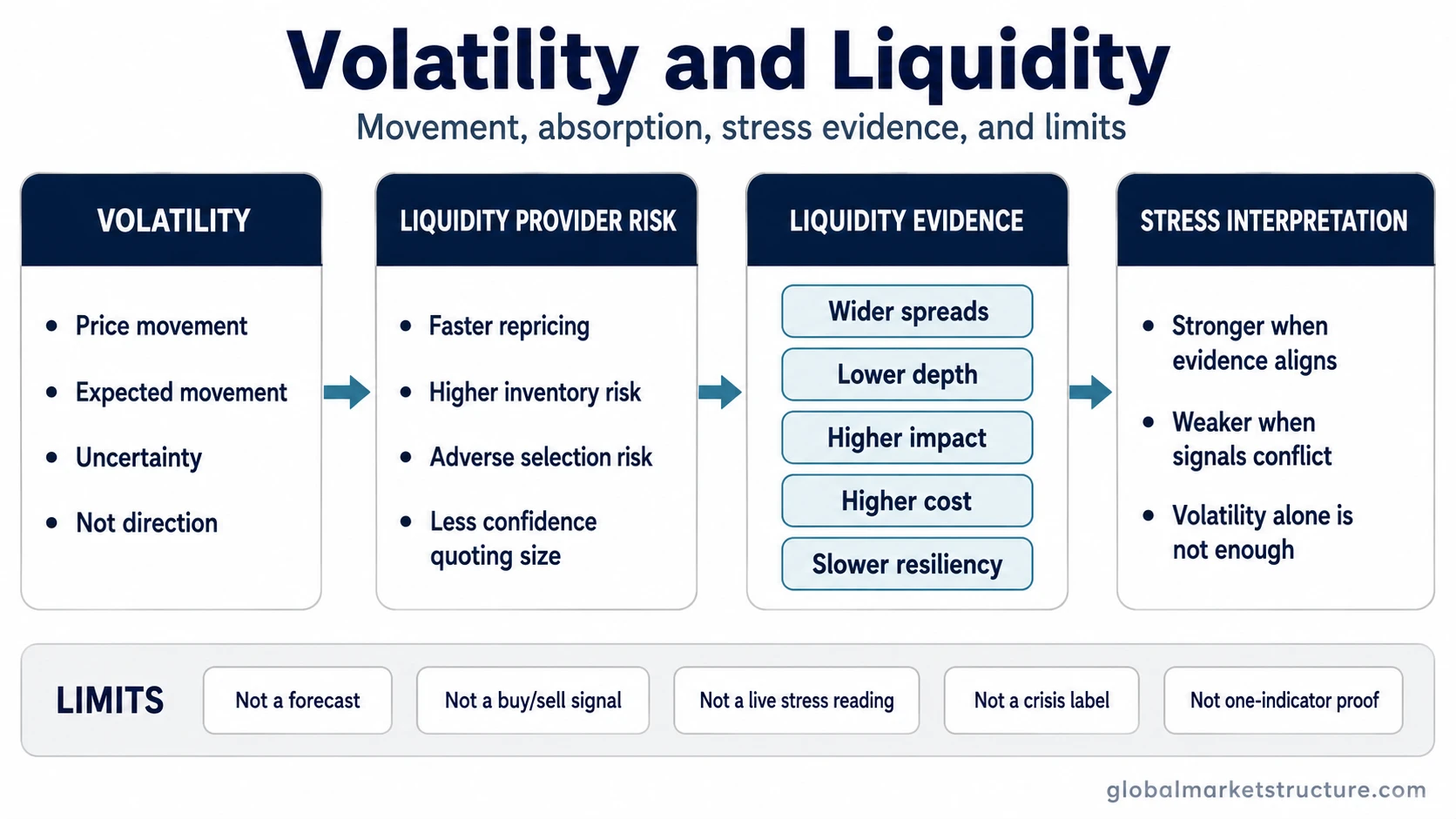

Volatility and liquidity are related, but they are not the same condition. Volatility describes movement or uncertainty. Liquidity describes how easily a market can absorb trading without large cost or price impact. High volatility becomes stronger liquidity evidence only when spreads widen, depth falls, market impact rises, cost-to-trade increases, or resiliency weakens.

Direct answer: high volatility does not automatically mean low liquidity. The reading becomes more useful when price movement is confirmed by weaker trading conditions: wider bid-ask spreads, thinner order-book depth, larger price impact, higher transaction cost, or slower recovery after order flow shocks.

What Volatility and Liquidity Measure Differently

Volatility measures how much prices move over a period of time or how much movement the market expects. It is about movement magnitude and uncertainty, not trading capacity.

Liquidity measures whether buyers and sellers can transact without forcing large price changes or paying unusually high execution costs. A liquid market can absorb orders with relatively limited price impact. A less liquid market may move sharply because fewer participants are willing or able to take the other side.

The useful distinction is movement versus absorption. Volatility tells you that prices are moving. Liquidity evidence helps judge whether the market is still absorbing trading normally or whether the movement is being amplified by weaker market depth and higher transaction cost.

Why Volatility Can Pressure Liquidity

Volatility can pressure liquidity because uncertainty changes the risk faced by liquidity providers. When prices move faster, quoting a tight bid and ask becomes more difficult. The participant providing liquidity faces more inventory risk, adverse selection risk, and uncertainty about the next price adjustment.

Mechanism sequence:

- Volatility rises and short-term price uncertainty increases.

- Liquidity providers face greater risk when quoting prices.

- Bid-ask spreads can widen to compensate for that risk.

- Quoted depth can fall because participants reduce displayed size.

- Larger orders can move price more because less depth is available.

- If the market recovers slowly after order flow shocks, volatility can begin to reinforce liquidity stress.

This sequence is conditional. A market can become volatile because new information is being repriced, while liquidity still remains functional. The liquidity reading is stronger only when the movement is accompanied by clear deterioration in trading conditions.

Evidence Needed Before Reading Volatility as Liquidity Stress

The evidence-before-interpretation test separates ordinary repricing from a weaker market-liquidity environment. Market liquidity is not defined by one metric alone. The reading is stronger when several liquidity dimensions deteriorate together.

| Liquidity evidence | What it can suggest | Why it matters | Limitation |

|---|---|---|---|

| Wider bid-ask spreads | Higher cost to transact | Liquidity providers may require more compensation for taking the other side | Spreads can widen temporarily around news without lasting liquidity stress |

| Lower quoted depth | Less displayed capacity to absorb orders | Smaller orders may move prices more than usual | Displayed depth does not capture all hidden or off-book liquidity |

| Higher market impact | Orders move price more aggressively | Absorption is weaker when trades create larger price changes | Impact depends on order size, market structure, and asset class |

| Higher cost-to-trade | Trading becomes more expensive even before direction is clear | Transaction cost can rise when spreads, slippage, or impact worsen | Cost changes need context across normal conditions for that market |

| Weaker resiliency | The market recovers more slowly after order flow shocks | Slow recovery can show that liquidity is not replenishing efficiently | One short dislocation does not prove a persistent liquidity problem |

| Funding pressure | Leveraged participants may reduce risk or pull back from liquidity provision | Funding constraints can turn market-liquidity weakness into broader stress | Funding liquidity is a related but separate concept and needs separate evidence |

When High Volatility Does Not Mean Low Liquidity

Common false reading: high volatility alone is not proof that liquidity has disappeared. Price movement can rise because the market is rapidly repricing information, not because participants cannot transact.

A liquid market can still move sharply when new information changes expected cash flows, policy expectations, positioning, or risk appetite. In that case, volatility reflects repricing. Liquidity stress is a stronger interpretation only if the market also shows wider spreads, thinner depth, larger market impact, higher transaction cost, or weak recovery after order flow.

The reverse can also matter. Liquidity can weaken before headline volatility fully reflects the change. If depth falls and spreads widen while realized price movement still looks contained, the market may be more fragile than volatility alone suggests.

Illustrative Scenario: Repricing Versus Liquidity Breakdown

A market reacts sharply to unexpected news. Prices move quickly for several minutes, but bid-ask spreads remain within a normal range, depth returns after the first adjustment, and large trades do not create unusually large price impact. That looks more like information repricing than a liquidity breakdown.

A different reading develops if the same volatility comes with wider spreads, disappearing depth, higher transaction cost, and slow recovery after order flow. In that case, the movement is no longer only about price uncertainty. It is also showing weaker absorption capacity.

This scenario is illustrative, not a historical case. It is useful because it separates two conditions that can look similar on a price chart but mean different things for market-structure interpretation.

How Volatility, Market Liquidity, Funding Liquidity, and Liquidity Risk Differ

Volatility describes movement. Market liquidity describes the ability to transact without excessive cost or price impact. Funding liquidity describes whether participants can obtain or maintain financing. Liquidity risk describes the risk that liquidity deteriorates when it is needed, often when uncertainty or stress is already rising.

| Concept | Main question | What not to assume |

|---|---|---|

| Volatility | How much are prices moving or expected to move? | Do not assume movement alone proves liquidity stress |

| Market liquidity | Can the market absorb trading without large cost or price impact? | Do not reduce liquidity to volume alone |

| Funding liquidity | Can participants finance positions and meet collateral needs? | Do not treat it as identical to market depth |

| Liquidity risk | Could liquidity become harder to access when conditions worsen? | Do not treat it as a forecast by itself |

How to Read the Relationship Safely

The safest reading starts with the question: did only price movement change, or did the market’s ability to absorb trading also weaken? Volatility becomes more useful as a stress-context signal when liquidity evidence deteriorates at the same time.

The interpretation strengthens when wider spreads, weaker depth, higher market impact, higher cost-to-trade, and slower resiliency align. The interpretation weakens when price movement rises but liquidity evidence remains functional or quickly normalizes.

In market-structure analysis, volatility and liquidity work best as a paired diagnostic. Volatility identifies movement and uncertainty. Liquidity evidence helps judge whether that movement is being absorbed normally or amplified by weaker market structure.