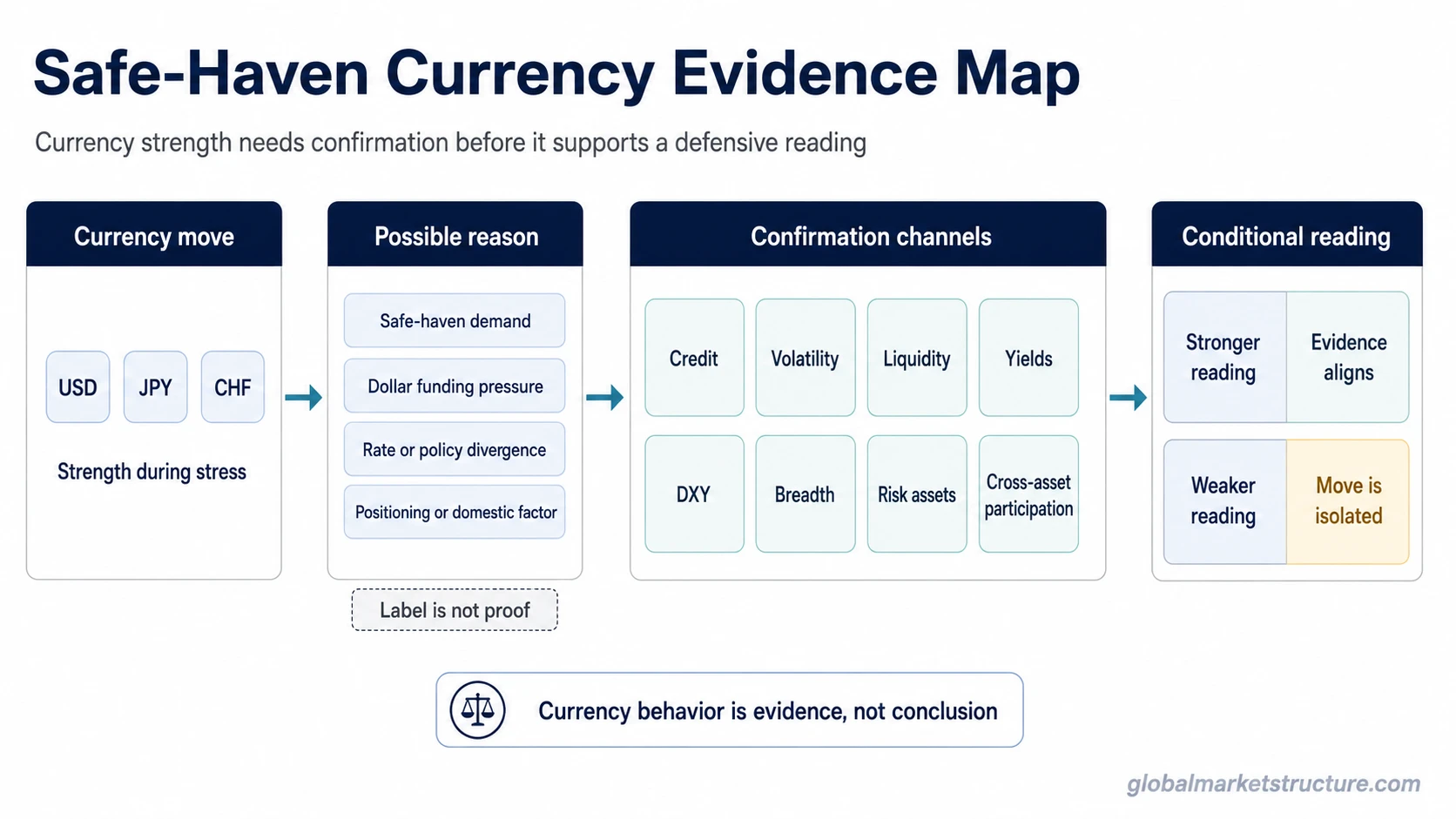

A safe-haven currency is a currency that investors and institutions may demand during market stress because it is perceived as liquid, resilient, or reliable. USD, JPY, and CHF are commonly cited examples, but their movement is not automatic proof of a defensive market regime. For USD especially, safe-haven demand must be separated from dollar funding stress, because a dollar move can reflect liquidity pressure as much as risk aversion.

Simple definition: a safe-haven currency is a currency that may attract demand when investors reduce risk and seek perceived liquidity, stability, or institutional depth.

Important limitation: safe-haven behavior is conditional. A currency can rise for reasons that have little to do with broad market stress.

What Is a Safe-Haven Currency?

A safe-haven currency is a currency that market participants may prefer when risk appetite falls. The demand usually comes from a search for liquidity, perceived stability, and the ability to move capital through deep financial markets during uncertain conditions.

The concept belongs to risk-environment interpretation, not to currency prediction. A safe-haven currency move can support a risk-off reading, but it should not define that reading by itself.

The useful distinction is that the currency move is evidence, not conclusion. The interpretation is more reliable when credit, volatility, rates, breadth, liquidity, and defensive cross-asset behavior point in the same direction.

Why Some Currencies Are Treated as Safe Havens

Currencies tend to receive safe-haven status when they are connected to deep markets, high liquidity, strong institutions, and credible policy frameworks. During stress, investors often prefer currencies that can absorb large flows without creating immediate convertibility or settlement concerns.

Several features can contribute to that perception:

- Liquidity: the currency can be traded and settled at scale.

- Market depth: the currency is connected to large bond, funding, or banking markets.

- Institutional credibility: investors trust the legal, monetary, or financial framework behind it.

- Policy credibility: the central bank and fiscal structure are viewed as relatively stable.

- Funding role: the currency may be important in global financing or collateral relationships.

None of these features make a currency permanently safe. They only explain why demand may appear during periods of uncertainty.

Common Safe-Haven Currency Examples

USD, JPY, and CHF are the most common examples in market education, but each one has a different reason for being watched. Their behavior should be interpreted through context rather than treated as a fixed rule.

| Currency | Why markets may treat it as defensive | Main caveat |

|---|---|---|

| USD | Deep markets, reserve-currency role, funding-market relevance, and demand for dollar liquidity during stress. | USD strength can reflect funding pressure or liquidity demand, not only classic safe-haven demand. |

| JPY | Often associated with defensive flows, funding-market behavior, and position unwinds during stress. | JPY behavior can also be affected by yield differentials, domestic policy expectations, and carry-position unwinds. |

| CHF | Often associated with perceived stability, institutional credibility, and defensive capital preservation behavior. | CHF movement can also be affected by policy decisions, valuation pressure, and domestic currency-management preferences. |

The useful question is not whether a currency has a safe-haven label. The useful question is whether its move aligns with the broader market environment.

How Safe-Haven Currency Behavior Appears During Risk-Off Conditions

During defensive market conditions, capital may move away from higher-risk assets and toward instruments perceived as more liquid or reliable. Currency demand can be one expression of that shift, especially when investors want flexibility, settlement certainty, or access to deep funding markets.

That behavior is closely related to flight to quality, where market participants move toward assets or currencies they view as more durable under stress. In currency markets, the flow can appear as demand for USD, JPY, CHF, or another currency viewed as relatively defensive in that specific context.

The signal carries more weight when several evidence channels agree:

- volatility is rising or staying elevated;

- credit spreads are widening or credit risk is being repriced;

- liquidity is deteriorating or funding pressure is increasing;

- yields are moving in a way consistent with growth fear or defensive demand;

- DXY behavior supports the broader currency-pressure picture;

- market breadth is weakening beneath headline indices;

- cross-asset participation shows defensive alignment rather than isolated currency noise.

USD Strength Needs a Special Caveat

USD strength deserves a separate interpretation because the dollar is not only a possible safe-haven currency. It is also closely tied to global funding, trade settlement, and liquidity demand. During stress, demand for dollars may rise because institutions need dollar liquidity, not simply because investors are choosing a defensive currency.

This is why a dollar rally can carry a different message from a CHF or JPY move. USD strength may reflect risk aversion, but it may also reflect funding stress, offshore dollar pressure, margin demand, balance-sheet constraints, or a rush for liquidity.

Interpretation rule: dollar strength should not be read as automatic risk-off confirmation. The cleaner reading appears when dollar behavior aligns with credit stress, volatility, liquidity pressure, weaker breadth, and defensive cross-asset participation.

What Weakens a Safe-Haven Currency Reading?

A safe-haven currency move becomes weaker when it is isolated from the rest of the market. Currency strength can come from domestic policy, interest-rate differentials, positioning, funding mechanics, or central-bank behavior rather than broad risk aversion.

| Condition | Why it weakens the reading |

|---|---|

| The currency move is isolated | Other markets are not confirming defensive behavior. |

| Credit spreads remain calm | Risk pricing may not be showing broad stress. |

| Volatility is falling | The move may not reflect rising uncertainty. |

| Yield differentials explain the move | Rate advantage may be more important than safe-haven demand. |

| Domestic policy dominates | Currency behavior may reflect local central-bank or fiscal expectations. |

| Positioning is crowded | The move may reflect unwind mechanics rather than a clean macro signal. |

| Risk assets remain broadly supported | The broader market may not be confirming a defensive regime. |

The false-reading risk is highest when a currency label replaces evidence. A safe-haven currency can support interpretation, but it cannot carry the whole regime reading alone.

Safe-Haven Currency vs Safe-Haven Assets

A safe-haven currency is a currency-specific expression of defensive demand. Safe-haven assets are a broader category that may include assets such as government bonds, gold, cash-like instruments, or other instruments perceived as more resilient during stress.

The difference matters because currencies can move for reasons that are specific to funding markets, policy expectations, and exchange-rate mechanics. A broader safe-haven asset reading usually needs a wider set of asset-class evidence.

Safe-Haven Currency vs Hard Currency

A hard currency is usually a broader term for a currency that is widely accepted, relatively stable, and trusted for international use. A safe-haven currency is more specific: it describes how a currency may behave or be demanded during periods of market stress.

The overlap can create confusion. A currency may be widely trusted without always acting as a safe haven, and a currency may show defensive demand in one stress episode without being a permanent shelter in every environment.

Practical Scenario

A cleaner safe-haven currency reading can appear when global equities weaken, credit spreads widen, volatility rises, and market breadth deteriorates while a commonly cited safe-haven currency also strengthens. In that setting, the currency move is not carrying the interpretation alone. It is one part of a broader defensive pattern.

The reading is weaker when the currency strengthens while credit remains calm, volatility falls, breadth is stable, and the move can be explained by interest-rate differentials. That situation may still matter for FX markets, but it is not enough by itself to label the broader environment as risk-off.

Related Concepts

Safe-haven currency behavior is easiest to understand inside the broader risk-on/risk-off framework. A risk-on environment usually reflects stronger risk appetite, while risk-off conditions reflect more defensive positioning, weaker risk appetite, or rising stress.

The closest related concepts are risk-off, flight to quality, and safe-haven assets. Together, they help separate the currency move, the broader defensive flow, and the wider asset-class response.

FAQ

What is a safe-haven currency?

A safe-haven currency is a currency that may attract demand during market stress because investors perceive it as liquid, resilient, or reliable. USD, JPY, and CHF are common examples, but their movement still needs broader market confirmation.

Is USD always a safe-haven currency?

No. USD can behave defensively during stress, but it can also strengthen because of dollar funding pressure, liquidity demand, interest-rate expectations, or positioning. The reason for the move matters.

Does a safe-haven currency confirm risk-off?

No. A safe-haven currency move can support a risk-off reading, but it does not confirm it alone. The reading is stronger when credit, volatility, liquidity, yields, breadth, and cross-asset behavior align.

What can weaken a safe-haven currency reading?

The reading weakens when the currency move is isolated, credit remains calm, volatility falls, risk assets stay supported, or the move is better explained by yields, policy, positioning, or funding mechanics.