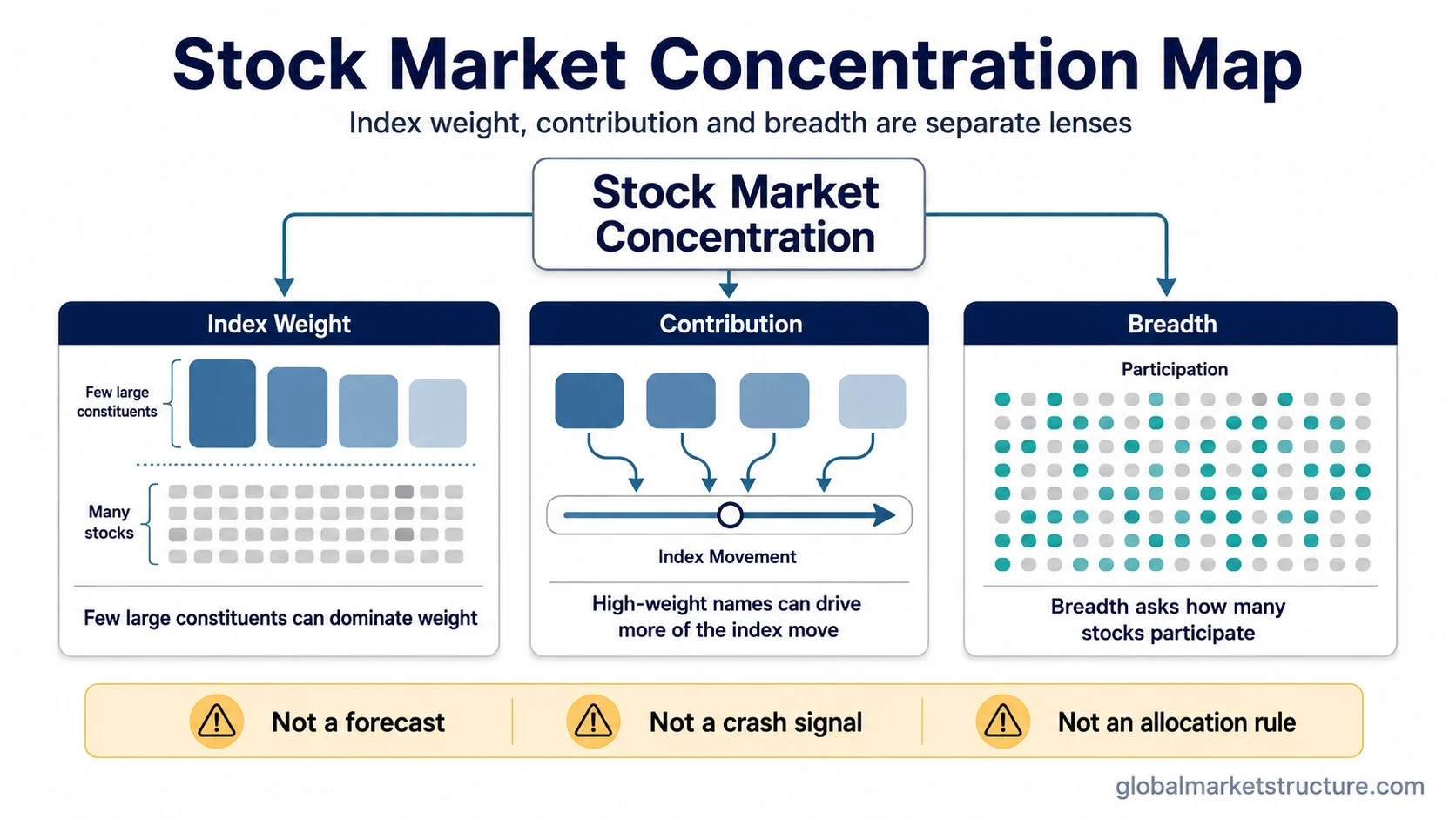

Stock market concentration describes how much of a stock market or index is dominated by a small number of large companies. In a market-cap-weighted index, the largest companies can carry more index weight and contribute more to index-level movement. Concentration is not, by itself, a forecast, a crash signal, or proof that the broader market is weak.

In one sentence: stock market concentration is a top-heavy stock or index structure where a small group of large companies has an outsized influence on market weight, index movement, or both.

- It measures dominance, not participation.

- It is usually most visible in market-cap-weighted indexes.

- It is different from industrial market concentration, where a few companies dominate an industry or product market.

- It is not portfolio advice, a timing signal, or a complete market-regime diagnosis.

How Stock Market Concentration Appears

Stock market concentration usually appears when the largest companies become a large share of total market value or index weight. In a market-cap-weighted index, larger companies receive larger weights, so their price movements can have more influence on the index than the movements of smaller constituents.

A concentrated market can still include many listed stocks. The issue is not the number of securities in the market. The issue is how much of the market’s weight, return contribution, earnings contribution, or investor attention is carried by a smaller leadership group.

That makes concentration a market-structure condition. It helps describe who is carrying the index, but it does not explain every reason the leadership group became large. The cause can involve earnings, valuation, liquidity, sector leadership, index construction, investor positioning, or several of those forces at once.

Common Measurement Lenses

No single measure captures stock market concentration perfectly. Each lens answers a different question, and each lens has a different limitation.

| Measurement lens | What it captures | What it does not prove |

|---|---|---|

| Largest-stock share | How much of an index or market is represented by the biggest single company. | It does not prove that the largest company is the best performer or that the market is unhealthy. |

| Top-10 share | How much index weight is held by the ten largest companies. | It does not prove a bubble, crash risk, or imminent broadening by itself. |

| Herfindahl-Hirschman Index | How concentrated weights are across constituents using a squared-weight approach. | It does not explain whether concentration is supported by earnings, valuation, or sector structure. |

| Cap-weight versus equal-weight behavior | Whether the largest-weighted stocks are driving more of the index result than the average constituent. | It does not mean equal-weight exposure is better or that allocation should change. |

| Contribution to index return | How much of an index move comes from a smaller group of high-weight companies. | It does not mean those companies had the highest percentage returns. |

| Earnings contribution versus market-cap weight | Whether large market weights are roughly matched by earnings contribution or other fundamental support. | It does not eliminate valuation risk or guarantee that concentration will persist. |

The useful approach is to treat these lenses as context, not as a single verdict. A market can look concentrated by index weight, less extreme by earnings contribution, and mixed by participation at the same time.

Concentration Is Not the Same as Market Breadth

Stock market concentration and market breadth answer different questions. Concentration asks how much market or index weight is carried by a small group. Breadth asks how widely participation is spread across many securities.

A market can be concentrated while breadth is still acceptable, especially if many stocks are participating but the largest companies have grown even faster. A market can also show strong index performance while participation underneath is weaker. That second condition is closer to breadth divergence, not concentration by itself.

The distinction matters because a top-heavy index does not automatically mean the whole market is weak. It means index-level movement may be more dependent on the behavior of a smaller leadership group.

What Stock Market Concentration Can and Cannot Show

Stock market concentration can show that index behavior is being carried by fewer large companies. It can also help explain why a broad index may move differently from the average stock inside that index.

False readings to avoid:

- High concentration is not a crash signal by itself.

- It does not prove that the market is in a bubble.

- It does not prove that participation across the broader market is weak.

- The largest index weights are not always the highest-returning stocks.

- Concentration can persist longer than expected.

- Concentration does not provide an allocation or rebalancing instruction.

Concentration becomes more useful when it is compared with other evidence. Breadth, earnings contribution, valuation, liquidity, sector leadership, and market regime can all change the interpretation. The same concentration level can mean different things depending on whether leadership is supported by fundamentals, crowded positioning, easy liquidity, or defensive narrowing.

Why Timing Is Uncertain

High concentration does not contain its own timing mechanism. A concentrated market can resolve in several ways, and none of those paths is guaranteed by concentration alone.

One path is leadership weakness, where the largest weights begin to decline and pull the index lower. Another path is broader catch-up, where more stocks participate and concentration becomes less extreme without the largest stocks collapsing. A third path is earnings catch-up, where fundamentals grow into a larger market weight. A fourth path is valuation compression, where large companies remain important but their multiples adjust. Concentration can also persist without a clean turning point.

That is why concentration works better as classification evidence than as a timing tool. It can describe market structure, but it cannot decide the next phase of the cycle without supporting evidence.

A Practical Scenario

Imagine a cap-weighted index rising while a few large companies contribute most of the index gain. The headline index looks strong, but many smaller constituents are flat or mixed. That situation shows concentration because index movement is being carried by a smaller leadership group.

The interpretation improves only after checking participation, earnings support, valuation context, liquidity conditions, and regime evidence. Without those checks, the same observation could be mistaken for broad strength, broad weakness, a bubble signal, or a timing signal.

Treat the situation as a generic illustration, not as a specific market episode, current index condition, or recommended action.

Related Concepts

Stock market concentration should be read alongside nearby concepts, but each one answers a different market-structure question.

- Market breadth focuses on participation across many securities, not dominance by a few large weights.

- Breadth divergence focuses on separation between index-level behavior and underlying participation.

- Concentration and index risk focuses on the benchmark and diversification implications created by top-heavy index structure.

Keeping these concepts separate prevents one common mistake: treating every top-heavy market as a full market-health diagnosis. Concentration is one evidence layer. It becomes stronger when it is read alongside participation, fundamentals, valuation, and regime context.

FAQ

Is stock market concentration the same as market breadth?

No. Stock market concentration measures dominance by a smaller group of large companies. Market breadth measures participation across many securities. A market can be concentrated and still have decent breadth, or it can be concentrated while participation underneath the index is weak.

Does high stock market concentration predict a crash?

No. High concentration can make index behavior more dependent on a smaller leadership group, but it does not predict a crash by itself. The interpretation depends on breadth, earnings support, valuation, liquidity, positioning, and broader regime evidence.

Can stock market concentration stay high for a long time?

Yes. Concentration can persist when large companies keep gaining weight, when fundamentals support leadership, or when index construction continues to amplify the largest market-cap names. Persistence does not remove risk, but it does weaken simple timing conclusions.