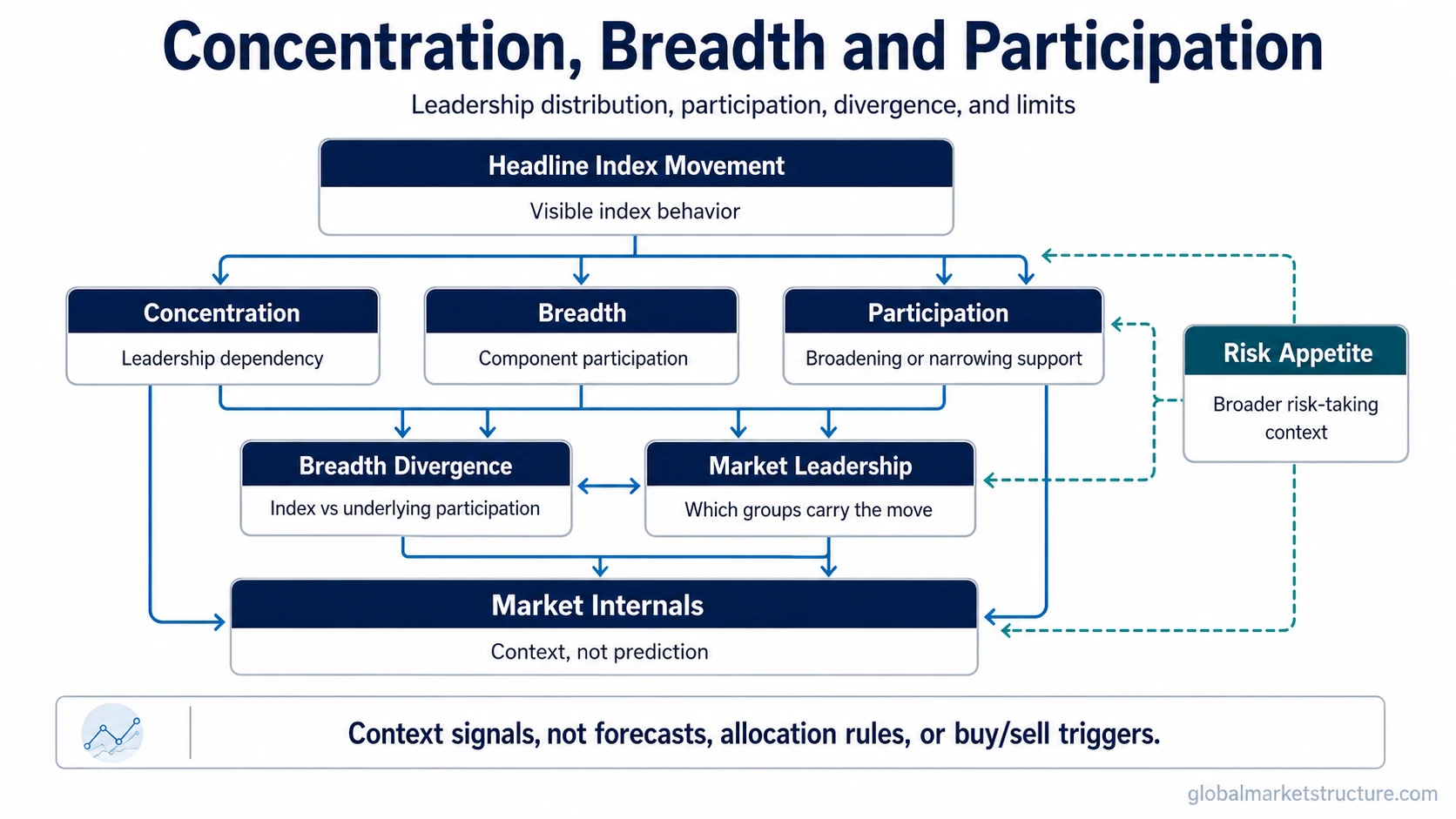

Concentration, breadth, and participation describe whether a market move is being carried by many securities, sectors, or regions, or by a narrow leadership group beneath the headline index. Concentration points to leadership dependency. Breadth measures how many components are moving with the index. Participation shows whether support is broadening or narrowing under the surface.

Core idea: headline index movement can hide the distribution of strength underneath it. A cap-weighted index may rise because a small group of large constituents is strong, while the average component, sector, or region shows weaker participation.

Key Points

- Concentration describes how dependent market performance is on a small group of leaders.

- Breadth describes how many underlying components are moving in the same direction as the broader market.

- Participation describes whether support is spreading across the market or narrowing into fewer areas.

- Breadth divergence appears when headline index behavior and underlying participation move in different directions.

- Market internals can add context, but they do not forecast future returns by themselves.

Concentration, Breadth and Participation at a Glance

| Concept | What it describes | Useful question | What it does not prove |

|---|---|---|---|

| Market concentration | How much leadership or index influence comes from a smaller group of securities, sectors, or regions. | Is the market dependent on a narrow leadership group? | High concentration does not automatically mean weakness or reversal. |

| Market breadth | How many underlying components are participating in a move. | Is strength or weakness widespread? | Strong breadth does not guarantee future gains. |

| Market participation | Whether support is expanding across more areas or narrowing into fewer areas. | Is the move becoming broader or more selective? | Participation does not remove the need for liquidity, credit, rate, and regime context. |

| Breadth divergence | A mismatch between headline index behavior and underlying participation. | Is the index masking weakness or improvement beneath the surface? | Divergence can persist and is not a timing signal by itself. |

| Market leadership | Which securities, sectors, styles, or regions are carrying the move. | Is leadership broad, rotating, or concentrated? | Leadership alone does not define the full macro regime. |

| Risk appetite | Whether markets are rewarding risk exposure or favoring caution. | Does participation align with broader risk-taking behavior? | Risk appetite can shift before or after breadth measures change. |

Which Concept Answers Which Question?

| Market question | Best next concept | Why it fits | Avoid this mistake |

|---|---|---|---|

| Can an index rise while many stocks fail to participate? | Market breadth | Breadth looks beneath the index level and checks how many components are moving with it. | Do not treat index strength as proof that the whole market is strong. |

| Is market performance dependent on a small leadership group? | Market concentration | Concentration focuses on dependency, weight, and leadership distribution. | Do not assume concentration is automatically negative. |

| Is support spreading into more areas or narrowing? | Market participation | Participation describes whether more securities, sectors, or regions are joining the move. | Do not use participation as a standalone forecast. |

| Is headline price action disagreeing with internal behavior? | Breadth divergence | Divergence captures the mismatch between index behavior and underlying participation. | Do not treat every divergence as an immediate reversal warning. |

| How can advancing and declining components be tracked? | Advance Decline Line | The advance-decline line tracks whether more components are rising or falling over time. | Do not rely on one breadth indicator without context. |

| Which areas are actually leading the market? | Narrow market leadership | Leadership analysis separates headline strength from the groups carrying that strength. | Do not confuse leadership with a complete regime signal. |

| Does the participation picture match broader risk behavior? | Risk appetite | Risk appetite connects breadth behavior with broader willingness to hold risk assets. | Do not ignore credit, liquidity, volatility, and rates. |

Route note: market participation is treated here as a concept within the breadth and leadership family. If a dedicated market participation URL is approved later, the row can be linked directly during final CMS cleanup.

How These Concepts Connect

Concentration and breadth often describe two sides of the same internal market structure. Concentration asks whether performance is carried by a small set of leaders. Breadth asks whether the move is supported by many components. Participation adds the direction of change: support may be spreading, fading, rotating, or staying confined to a narrow group.

A cap-weighted index can create confusion because the largest components have more influence over the headline level. If those leaders rise while many smaller components lag, the index can look stronger than the average underlying security. If participation broadens, the market move becomes less dependent on the largest leaders, although that still does not guarantee future returns.

Headline index versus underlying participation: the index level answers what the benchmark did. Breadth and participation ask how widely that move was supported.

Common Interpretation Patterns

| Generic pattern | Possible interpretation | Main limitation |

|---|---|---|

| Headline index strong and breadth strong | Strength is more broadly supported across underlying components. | Broad support still needs confirmation from liquidity, credit, rates, and volatility conditions. |

| Headline index strong and breadth weak | Leadership may be narrow, with the index depending on a smaller group of large components. | Narrow breadth can persist for long periods and is not an immediate reversal signal. |

| Index flat and participation improving | Underlying support may be broadening even before the headline index reflects it clearly. | Improving participation can fail if liquidity or risk appetite deteriorates. |

| Concentration high and participation broadening | Large leaders may still matter, but support is spreading into more areas. | The market can remain leader-dependent even while participation improves. |

| Concentration high and participation weakening | The market may be more dependent on narrow leadership while fewer components confirm the move. | This is a cautionary context, not a complete forecast or trade signal. |

What Breadth and Participation Do Not Prove

- Narrow breadth can persist: concentrated leadership can continue when dominant companies, sectors, or regions have stronger earnings, liquidity access, or investor preference.

- Broad participation is not a return guarantee: wider support can strengthen the interpretation of a move, but it does not remove valuation, liquidity, credit, or policy risk.

- Concentration is not automatically fragile: concentration can reflect real cash-flow, earnings, balance-sheet, or structural advantages.

- One breadth measure is not enough: advance-decline data, stocks above moving averages, new highs and lows, sector participation, and equal-weight behavior can disagree.

- Regime context still matters: liquidity, rates, credit spreads, volatility, and broader risk behavior can change the meaning of breadth signals.

Related Market Structure Concepts

- Market breadth explains the participation depth behind headline index movement.

- Market concentration explains leadership dependency and index-weight distortion.

- Breadth divergence explains mismatches between price and internal participation.

- Advance Decline Line shows one common way to track advancing versus declining components.

- Narrow market leadership explains concentrated leadership patterns.

- Risk appetite connects participation behavior with the broader willingness to hold risk exposure.