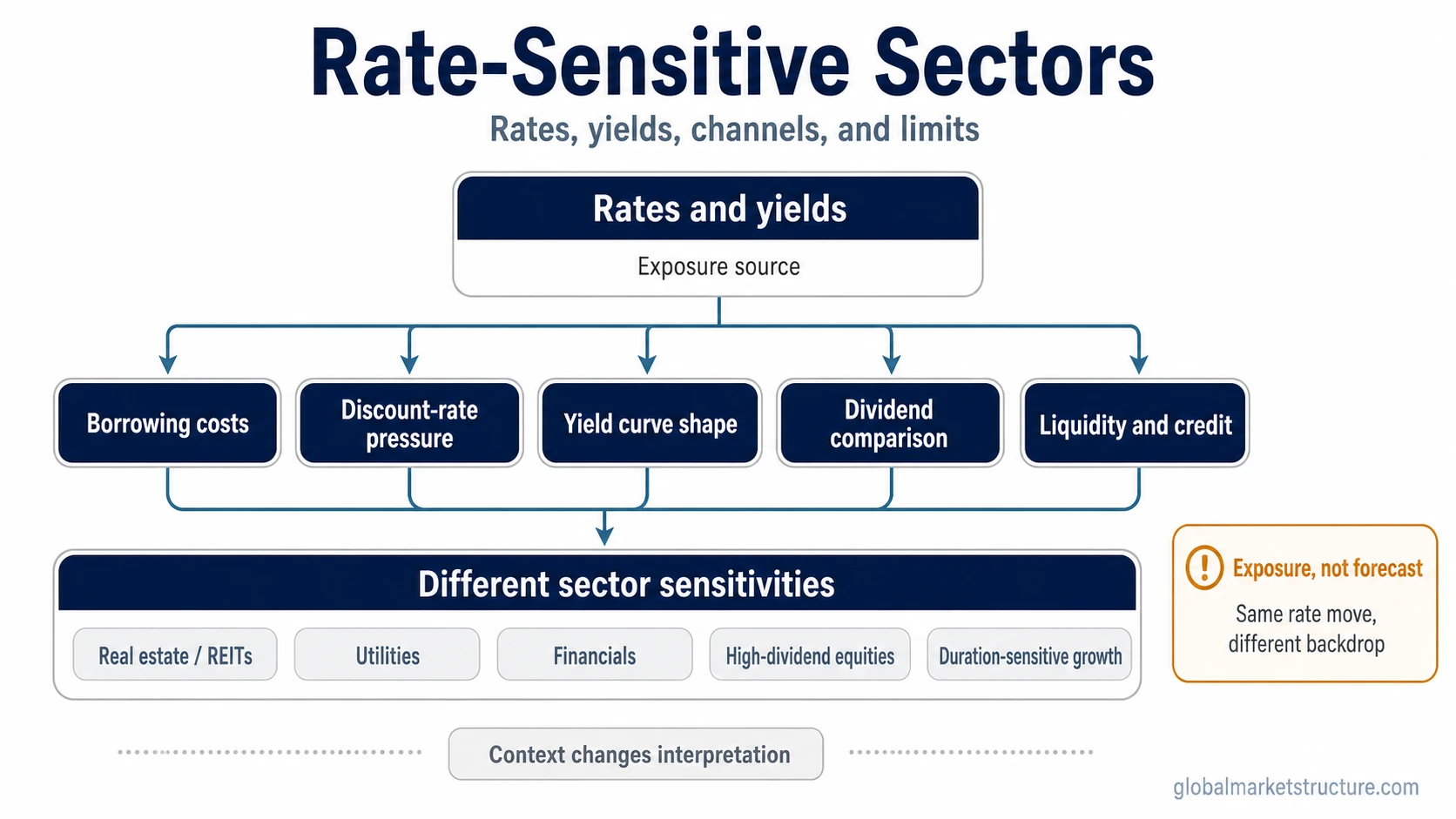

Rate-sensitive sectors are equity sectors or groups whose market behavior is unusually affected by interest rates, yield expectations, financing costs, or discount-rate pressure. Real estate, utilities, financials, high-dividend equities, leveraged companies, and duration-sensitive growth groups can all be rate-sensitive, but not in the same way. The label describes exposure, not a forecast, allocation rule, or buy/sell signal.

Compact definition: Rate-sensitive sectors are market groups whose valuations, earnings expectations, financing conditions, or relative appeal can change meaningfully when rates, bond yields, or financial conditions shift.

For market-cycle interpretation, rate sensitivity is most useful as a classification lens. It helps identify which parts of equity leadership may be responding to yield pressure, financing costs, curve shape, liquidity, or discount-rate changes.

The key limitation is that rate sensitivity does not tell the direction of future returns. The same fall in yields can mean easier financial conditions, weaker growth expectations, rising credit stress, or a defensive bid, and each backdrop can affect sector behavior differently.

What makes a sector rate-sensitive

A sector becomes rate-sensitive when interest-rate changes can affect its valuation, earnings path, balance-sheet pressure, investor demand, or relative yield appeal. The connection can come through borrowing costs, discount rates, refinancing risk, dividend comparison, net interest margins, or broader financial conditions.

Rate sensitivity is not limited to one official sector label. It can describe a formal sector, a sub-industry, a style group, or a group of companies with similar exposure to rates and yields.

- Borrowing costs: higher financing costs can pressure companies that rely heavily on debt or refinancing.

- Discount-rate pressure: higher yields can reduce the present value investors assign to long-duration cash flows.

- Yield competition: higher bond yields can reduce the relative appeal of dividend-heavy or bond-proxy equities.

- Yield curve shape: banks and lenders may react differently to parallel rate moves, steepening curves, and flattening curves.

- Liquidity conditions: rate changes often interact with credit availability, risk appetite, and funding conditions.

Common rate-sensitive sector groups

Several groups are commonly described as rate-sensitive, but the reason differs by business model. A clean classification separates the exposure channel from the expected outcome.

| Group | Why rates matter | Key caveat |

|---|---|---|

| Real estate and REITs | Property values, refinancing costs, cap rates, and dividend comparisons can be sensitive to bond yields. | Lower yields do not automatically help if credit availability weakens, debt maturities become restrictive, or property fundamentals deteriorate. |

| Utilities | Utilities often carry meaningful debt and may be compared with bond-like income alternatives. | Defensive demand does not remove rate sensitivity; regulation, debt costs, and bond-yield competition still matter. |

| Financials | Banks, insurers, and lenders can be affected by rate levels, curve shape, deposit costs, credit demand, and asset yields. | Higher rates are not automatically positive. A flatter curve, deposit pressure, or credit stress can offset the benefit of higher asset yields. |

| High-dividend and bond-proxy equities | The relative appeal of dividend income can change when safer bond yields rise or fall. | Dividend yield alone does not define safety, valuation quality, or future return. |

| Leveraged companies | Debt-heavy businesses can face higher interest expense, refinancing risk, and tighter financial flexibility. | The effect depends on maturity schedules, fixed versus floating debt, pricing power, and credit access. |

| Growth and duration-sensitive equities | Companies whose expected cash flows sit further in the future can be more exposed to discount-rate changes. | Strong earnings growth can offset some valuation pressure, while rising real yields can still compress multiples. |

| Housing-sensitive and selected small-cap groups | Mortgage rates, consumer financing, and credit availability can affect demand and funding costs. | Rate sensitivity varies widely by balance sheet, business model, and end-market exposure. |

Main channels of rate sensitivity

Rate-sensitive sectors do not respond to rates through a single channel. A better reading separates the specific transmission path from the broader market environment.

- Borrowing cost channel: higher policy rates and market yields can raise interest expense, refinancing costs, and the hurdle rate for new projects.

- Discount-rate channel: higher yields can lower the valuation assigned to future cash flows, especially when cash-flow expectations are long-duration.

- Yield curve channel: the shape of the curve can matter as much as the level of rates, especially for lenders and financial intermediaries.

- Dividend comparison channel: income-oriented equities can face competition from bonds when safer yields rise.

- Liquidity and financial-conditions channel: rates interact with credit spreads, funding markets, lending standards, and risk appetite.

The discount-rate channel is especially important for duration-sensitive equity groups. When real yields rise, valuation pressure can increase even if nominal growth still looks healthy. When nominal yields fall because growth expectations are weakening, the valuation benefit may be offset by weaker earnings expectations.

Why rate-sensitive sectors do not all move the same way

The phrase “rate-sensitive” identifies exposure, not a single market reaction. Two sectors can both be sensitive to rates while responding differently to the same yield move.

Curve shape is one reason. A broad decline in yields can support long-duration valuations, but a flattening curve may pressure parts of financials if lending spreads and deposit dynamics weaken. A steepening curve can carry a different message depending on whether it reflects stronger growth expectations, inflation pressure, or rising term premium.

Real yields and nominal yields also need separation. Nominal yields include inflation expectations, while real yields more directly affect discount-rate pressure after inflation adjustment. Growth-oriented equities may react more to real-yield pressure than to the headline yield level alone.

Credit conditions can change the interpretation. Lower yields caused by easier liquidity can be supportive for some rate-sensitive groups. Lower yields caused by recession fear or widening credit stress can point to a more defensive environment, even if the direction of yields appears favorable at first glance.

Rate-sensitive sectors vs nearby concepts

Rate-sensitive sectors overlap with other market-cycle categories, but they are not the same concept. The distinction matters because each label describes a different exposure.

| Concept | Main question | Difference from rate-sensitive sectors |

|---|---|---|

| Rate-sensitive sectors | Which groups are unusually exposed to rates, yields, financing costs, or discount-rate pressure? | The focus is rate exposure, not broad economic sensitivity or leadership timing. |

| Cyclical sectors | Which groups are more exposed to economic expansion and contraction? | A cyclical sector can be rate-sensitive, but cyclicality is mainly about economic demand sensitivity. |

| Defensive sectors | Which groups tend to have more stable demand across the business cycle? | A defensive group can still be rate-sensitive if valuation, debt cost, or dividend comparison is tied to yields. |

| Sector rotation | Which sectors are gaining or losing leadership as the market cycle changes? | Rate sensitivity can help explain one driver of leadership change, but it is not the full rotation framework. |

| Style rotation | How does leadership shift between styles such as growth and value? | Rate sensitivity can affect duration-sensitive growth and value-oriented income groups, but style leadership also depends on earnings, valuation, breadth, and risk appetite. |

Rate-sensitive sectors example in context

A common scenario is that yields fall while different rate-sensitive groups behave differently. Real estate and utilities may receive support from lower discount-rate pressure, while financials may not respond the same way if the yield curve flattens or credit concerns rise.

The useful interpretation is not that one group must outperform. The useful interpretation is that the reason yields are moving changes the meaning of the sector response. Falling yields driven by easier liquidity can send a different message than falling yields driven by growth fear.

Interpretation rule: Rate-sensitive sectors should be read with the reason for the rate move, not just the direction of the rate move.

Common mistake and limitation

The common mistake is treating rate sensitivity as a simple rule: rates down means all rate-sensitive sectors rise, and rates up means all rate-sensitive sectors fall. That shortcut ignores curve shape, real yields, credit conditions, earnings expectations, and risk appetite.

Financials show the problem clearly. Higher rates may increase asset yields, but they may also pressure deposits, loan demand, funding costs, or credit quality. Utilities and real estate show a different problem. Lower yields may reduce discount-rate pressure, but weaker growth or tighter credit can still damage fundamentals.

Key limits of the label

- Rate sensitivity identifies exposure, not future return.

- The same sector can react differently to nominal yields, real yields, and curve shape.

- Lower rates are not automatically bullish if they reflect growth stress or credit stress.

- The label does not prove the current market-cycle phase.

- The label does not create a sector allocation rule or trading signal.

FAQ

Which sectors are usually considered rate-sensitive?

Common examples include real estate, REITs, utilities, financials, high-dividend equities, leveraged companies, housing-sensitive groups, and duration-sensitive growth equities. The exact exposure depends on the business model, balance sheet, yield curve, credit conditions, and investor demand.

Are rate-sensitive sectors the same as defensive sectors?

No. Defensive sectors are usually defined by more stable demand across the business cycle. Rate-sensitive sectors are defined by exposure to rates, yields, financing costs, or discount-rate pressure. A defensive sector such as utilities can still be rate-sensitive.

Do lower rates mean rate-sensitive sectors should outperform?

No. Lower rates can help some rate-sensitive groups, but the reason rates are falling matters. Falling yields caused by easier liquidity can carry a different message than falling yields caused by recession fear, credit stress, or weaker earnings expectations.

Why can financials react differently from other rate-sensitive sectors?

Financials are affected by rate levels, yield curve shape, deposit costs, loan demand, credit quality, and funding conditions. Higher rates may help some income streams, but a flatter curve, rising credit risk, or deposit pressure can weaken the interpretation.