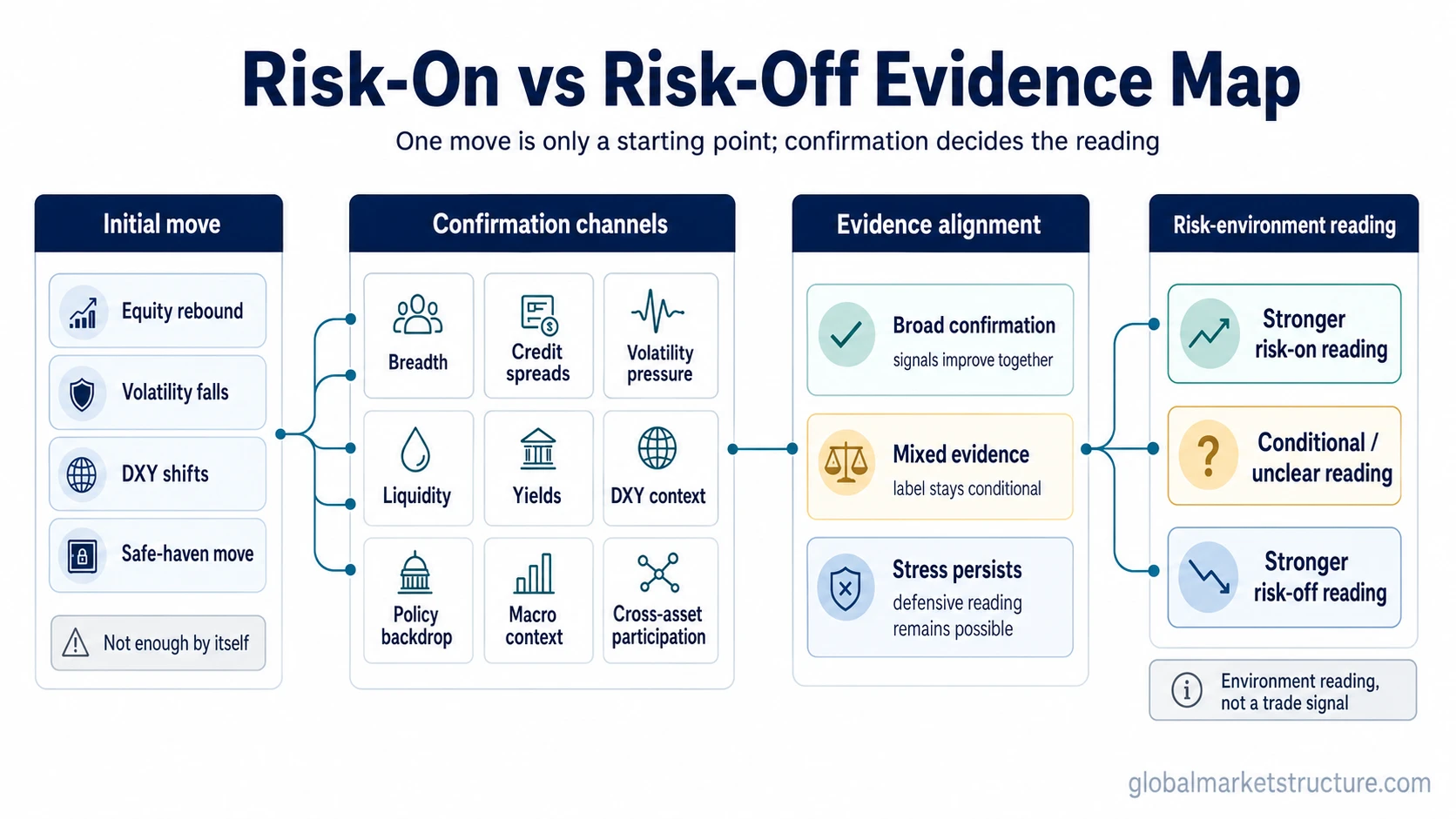

Risk-on and risk-off are opposite risk-environment readings. Risk-on means markets are more willing to reward risk exposure, usually with broader participation in growth-sensitive or cyclical assets. Risk-off means markets are prioritizing safety, liquidity, and capital preservation. The distinction becomes useful only when price behavior is checked against breadth, credit, volatility, liquidity, yields, DXY, policy backdrop, and macro context.

Key Points

- Risk-on describes a market environment where risk exposure is being rewarded more broadly.

- Risk-off describes a market environment where defensive positioning, liquidity preference, and safe-haven demand become more important.

- A rebound, falling volatility reading, weaker dollar, or safe-haven move can help the interpretation, but none is enough by itself.

- The strongest reading comes from agreement across breadth, credit, volatility, liquidity, yields, currency pressure, policy backdrop, and macro context.

Risk-On vs Risk-Off: Core Difference

| Comparison point | Risk-on | Risk-off | Interpretation limit |

|---|---|---|---|

| Risk appetite | Investors show greater willingness to accept uncertainty and cyclical exposure. | Investors show greater preference for safety, liquidity, and balance-sheet protection. | Risk appetite can shift before the full market environment confirms. |

| Typical market mood | Confidence, participation, and carry-seeking behavior often improve. | Caution, liquidity preference, and defensive behavior often increase. | Sentiment alone can move faster than underlying credit or liquidity conditions. |

| Asset participation | Growth-sensitive, cyclical, high-beta, and credit-sensitive assets may participate more broadly. | Defensive assets, high-quality bonds, cash-like instruments, and safe havens may receive more attention. | Asset behavior varies when inflation, real yields, policy, or positioning dominate the move. |

| Credit conditions | Credit spreads may stabilize or narrow as default-risk concern eases. | Credit spreads may widen as investors demand more compensation for risk. | Equity strength can mislead if credit is still deteriorating beneath the surface. |

| Volatility | Volatility pressure often eases when stress is fading. | Volatility often rises when hedging demand and uncertainty increase. | A falling volatility index can reflect short-term relief rather than durable risk-on confirmation. |

| Liquidity preference | Markets may become more willing to hold less liquid or more cyclical exposure. | Markets may prefer cash, depth, quality, and instruments that can be exited more easily. | Liquidity can look stable until funding pressure or market depth weakens. |

| Yields and rates context | Rising yields can support risk-on when they reflect better growth expectations and stable credit. | Falling yields can support risk-off when they reflect growth fear, safety demand, or stress. | The same yield move can mean different things depending on inflation, policy, and credit context. |

| DXY and currency pressure | A softer dollar can support easier global financial conditions when other signals agree. | A stronger dollar can reflect funding pressure, global stress, or demand for liquidity. | DXY alone does not classify the full environment. |

| Safe-haven demand | Safe-haven demand may fade when risk tolerance broadens. | Safe-haven assets may attract demand when capital preservation becomes more important. | Safe havens do not move uniformly in every episode. |

| Confirmation quality | Stronger when breadth, credit, volatility, liquidity, and cross-asset participation improve together. | Stronger when defensive demand, credit stress, volatility, and liquidity preference rise together. | Mixed evidence should remain a conditional reading, not a market call. |

What Risk-On Means

Risk-on describes a market environment where investors are more willing to accept risk and markets are more willing to reward that exposure. It often appears through broader participation in equities, cyclical sectors, high-yield credit, emerging markets, or other growth-sensitive assets.

The important point is that risk-on is an environment reading, not an instruction. An equity index can rise while participation remains narrow, credit spreads stay stressed, or liquidity conditions remain fragile. In that case, the move may be a rebound in price rather than a confirmed risk-on environment.

A stronger risk-on reading usually needs more than higher prices. Breadth should improve, credit should stabilize, volatility should calm, liquidity should look healthier, and participation should broaden beyond a small group of leaders.

What Risk-Off Means

Risk-off describes a market environment where investors place more weight on safety, liquidity, and capital preservation. Defensive assets, high-quality bonds, cash-like exposure, or perceived safe havens may become more important when uncertainty rises.

Risk-off does not automatically mean every risky asset must fall. Some assets can rebound inside a still-defensive environment, and some safe havens may fail to rise if inflation, real yields, currency pressure, or positioning are moving against them.

A stronger risk-off reading usually develops when several conditions align: credit spreads widen, volatility rises, liquidity preference increases, market breadth weakens, and capital moves toward perceived quality rather than broad risk exposure.

How to Confirm the Difference

The difference between risk-on and risk-off becomes clearer when several evidence channels point in the same direction. A single signal can start the question, but the broader stack determines whether the label is strong, weak, or mixed.

| Evidence channel | Stronger risk-on reading | Stronger risk-off reading | Why one signal can mislead |

|---|---|---|---|

| Breadth | More sectors, regions, and asset groups participate in the move. | Leadership narrows and more assets weaken beneath the index surface. | A strong index can hide weak participation. |

| Credit spreads | Spreads stabilize or narrow as risk compensation falls. | Spreads widen as investors demand more protection against default or stress. | Equities can rally while credit still signals caution. |

| Volatility | Volatility falls alongside improving breadth and calmer credit. | Volatility rises or remains elevated while hedging demand persists. | Volatility can drop during temporary relief without confirming a durable regime shift. |

| Market liquidity | Depth improves and price moves become less disorderly. | Depth deteriorates and larger price gaps appear more easily. | Index prices may look calm while liquidity beneath them is weaker. |

| Funding liquidity | Financing pressure eases and leveraged participants face less forced reduction. | Funding stress rises and participants prefer cash or balance-sheet protection. | Funding pressure can appear before broad price indexes fully reflect it. |

| Yields | Yield moves support risk when they reflect better growth and stable credit. | Yield moves support risk-off when they reflect safety demand or growth concern. | The same yield direction can carry different meanings in different macro settings. |

| DXY and dollar pressure | A softer dollar can support risk when global liquidity and breadth improve. | A stronger dollar can signal stress when it tightens global financial conditions. | Dollar moves can also reflect rate differentials, policy divergence, or positioning. |

| Policy backdrop | Policy expectations reduce stress without creating new inflation or credibility concerns. | Policy uncertainty, tightening pressure, or credibility concern keeps investors defensive. | Policy relief can lift prices briefly without fixing credit or liquidity stress. |

| Macro context | Growth expectations improve without a sharp deterioration in inflation or credit quality. | Growth, earnings, or financial-stability concerns dominate the environment. | Macro narratives can lag the market or overstate a single data point. |

| Cross-asset participation | Equities, credit, cyclicals, and liquidity-sensitive assets confirm each other. | Defensive assets, dollar pressure, credit stress, and volatility confirm caution. | One asset class can move for local reasons while the broader environment stays mixed. |

Same Move, Different Reading

An equity rebound after a selloff can support a risk-on reading if participation broadens, credit spreads stabilize, volatility falls, liquidity improves, and cyclical assets join the move. Under those conditions, the rebound is not just a price bounce. It is being confirmed by the surrounding market environment.

The same rebound can remain a relief rally inside a risk-off environment if credit remains stressed, breadth stays narrow, defensive demand persists, or liquidity is still tightening. Price has improved, but the evidence stack has not fully changed.

No current market classification is implied by that example. The comparison is useful because the same price movement can carry different meaning when breadth, credit, volatility, and liquidity disagree.

Asset Behavior Without Trade Instructions

Risk-on environments often involve stronger participation from growth-sensitive assets, cyclical sectors, high-beta equities, credit-sensitive assets, and markets that benefit from easier financial conditions. That behavior can help identify the environment, but it should not be treated as a list of assets to buy.

Risk-off environments often involve stronger preference for cash, high-quality bonds, defensive assets, gold, the U.S. dollar, the Japanese yen, the Swiss franc, or other perceived safety destinations. That behavior can help identify defensive demand, but it should not be treated as a list of assets that must rise.

Asset behavior is not uniform across every episode. Policy expectations, inflation pressure, real yields, dollar liquidity, credit stress, and positioning can change how the same asset behaves. The useful question is not whether one asset moved. The useful question is whether several markets are telling the same risk-environment story.

Common False Readings

- Equity rebound alone: higher stock prices can reflect short-covering, positioning relief, or narrow leadership rather than broad risk-on confirmation.

- Falling volatility alone: lower implied volatility can appear during temporary calm while credit or liquidity conditions remain weak.

- Weaker dollar alone: a softer dollar can support risk, but it can also reflect rate expectations, positioning, or policy divergence.

- Safe-haven move alone: safe-haven demand can rise for reasons that do not define the entire risk environment.

- Narrow leadership: a few strong index weights can make the surface look risk-on while the broader market remains fragile.

- Calm index level: stable headline prices can hide deteriorating credit, weaker breadth, or thinner liquidity.

Is Risk-On the Same as Bullish?

Risk-on often overlaps with bullish price behavior, but the two labels are not the same. Bullish usually describes directional price bias. Risk-on describes the broader environment around risk appetite, participation, credit, liquidity, volatility, and cross-asset confirmation.

A market can look bullish in price while the risk-on reading remains weak if participation is narrow or credit conditions are deteriorating. The opposite can also happen: early risk-on evidence can begin forming before the strongest price trend is obvious.

Is Risk-Off the Same as Bearish?

Risk-off often overlaps with bearish pressure in risk assets, but it is not identical to bearish. Bearish usually refers to expected or observed downside in a price series. Risk-off refers to a broader preference for safety, liquidity, defensive exposure, or quality.

A risk-off environment can include temporary rebounds, defensive rallies, or mixed asset behavior. The label becomes stronger when the defensive evidence is broad, not when one risky asset falls or one safe-haven asset rises.

Risk-On vs Risk-Off in One Sentence

Risk-on means the market environment is rewarding broader risk exposure, while risk-off means the market environment is prioritizing safety and liquidity, and both labels need confirmation across several market signals before they become useful.

FAQ

Is risk-on the same as bullish?

No. Risk-on often overlaps with bullish price behavior, but bullish describes price direction while risk-on describes the broader risk environment. A market can rise without broad risk-on confirmation if breadth, credit, or liquidity remain weak.

Is risk-off the same as bearish?

No. Risk-off often overlaps with bearish pressure in risky assets, but it describes a preference for safety, liquidity, and capital preservation. Temporary rebounds can still occur inside a risk-off environment.

Can a market rebound still be risk-off?

Yes. A rebound can remain temporary relief if credit stays stressed, breadth remains narrow, volatility stays elevated, or safe-haven demand persists. The rebound becomes more meaningful when several confirmation channels improve together.

Which signals matter most when comparing risk-on and risk-off?

The strongest readings usually come from agreement across breadth, credit spreads, volatility, liquidity, yields, currency pressure, policy backdrop, macro context, and cross-asset participation. One signal can help, but it should not classify the full environment by itself.