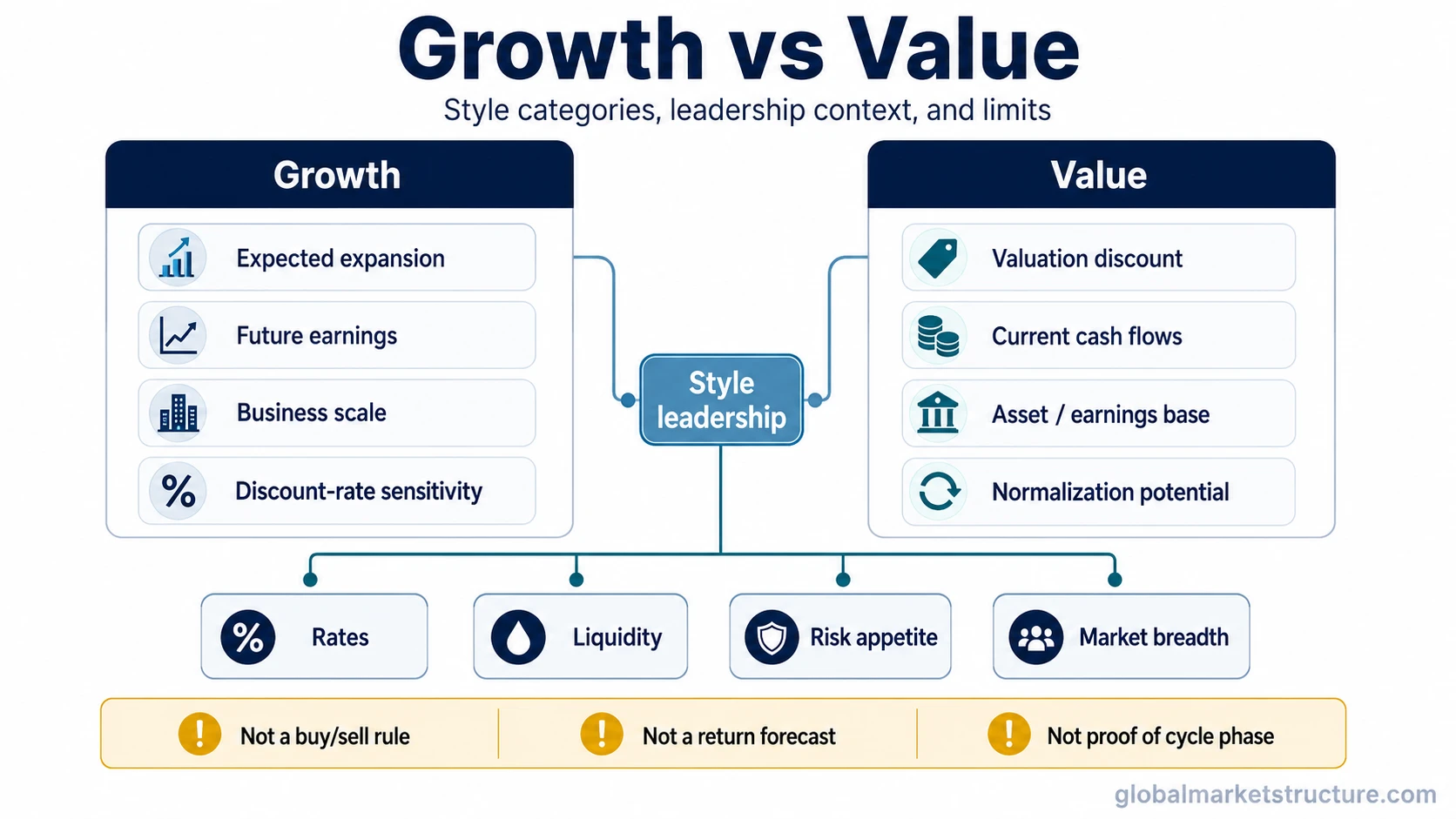

Growth vs value compares two equity style categories. Growth stocks are usually grouped around expected revenue, earnings, or business-scale expansion, while value stocks are usually grouped around lower valuation multiples, mature cash flows, or assets priced below what investors believe they may be worth. In market-cycle analysis, the distinction is useful for reading style leadership, but it is not a buy/sell rule, a return forecast, or proof of the current cycle phase.

The useful distinction is not deciding which style is “better.” It is reading what changing leadership between growth and value may suggest about rates, liquidity, risk appetite, valuation pressure, and market participation.

Growth vs value at a glance

| Category | Growth | Value |

|---|---|---|

| Core idea | Companies priced around expected expansion in sales, earnings, market share, or business scale. | Companies priced around valuation discount, existing cash flows, asset value, or mean-reversion potential. |

| Market sensitivity | Often more sensitive to discount-rate assumptions when future earnings carry much of the valuation case. | Often more sensitive to current earnings, balance-sheet strength, sector cyclicality, and valuation normalization. |

| Leadership signal | Can point to strong risk appetite, abundant liquidity, falling rate pressure, or confidence in future growth. | Can point to valuation discipline, earnings resilience, reflation expectations, or rotation toward cheaper market areas. |

| Common mistake | Treating high growth expectations as automatic leadership. | Treating low valuation as automatic opportunity. |

| What it does not prove | It does not prove that future returns will be strong. | It does not prove that the discount will close. |

What growth means as a style category

Growth stocks are usually associated with companies where investors pay more attention to expected future expansion than to current valuation cheapness. That expansion may come from revenue growth, earnings growth, business-model scaling, market-share gains, or a long runway for reinvestment.

Because more of the valuation case can sit in the future, growth leadership is often sensitive to the discount rate applied to future cash flows. When rate pressure falls or liquidity conditions feel easier, investors may become more willing to pay for distant growth. When yields rise or liquidity tightens, the same future growth expectations can face more valuation pressure.

This does not mean growth stocks only lead in one type of market. Strong earnings momentum, dominant business models, sector concentration, or narrow index leadership can also support growth-style strength. The label describes the style exposure; it does not explain the full reason for leadership by itself.

What value means as a style category

Value stocks are usually associated with companies trading at lower valuation multiples, with more emphasis on present earnings, assets, dividends, cash flows, or the possibility that the market has priced the business too cheaply.

Value leadership can appear when investors become less willing to pay for distant expectations and more focused on current cash generation. It can also appear during reflationary phases, sector recoveries, commodity-linked leadership, financial-sector strength, or periods when previously ignored market areas start participating.

The value label still needs context. A low valuation may reflect a real problem rather than a mispricing. Weak growth, balance-sheet stress, declining margins, or structural disruption can make a stock look statistically cheap without making it a stronger market-leadership candidate.

Style label, leadership evidence, and cycle interpretation are different

The growth vs value distinction becomes more useful when three layers are kept separate. First, the style label identifies how a group of stocks is commonly classified. Second, leadership evidence asks which group is actually outperforming, how broad that participation is, and whether the move is persistent. Third, cycle interpretation asks what that leadership might suggest about the broader market environment.

Those layers should not be collapsed into one conclusion. Growth leadership does not automatically mean the market is in a healthy expansion. Value leadership does not automatically mean a new cycle has begun. Either style can lead for different reasons, and those reasons can change depending on rates, liquidity, credit conditions, earnings expectations, and sector mix.

This is where style rotation matters. The rotation itself is observable through relative performance, but the interpretation depends on surrounding evidence. A style shift is stronger as a market signal when it is supported by breadth, sector confirmation, credit stability, and consistent participation rather than a short-lived move in a few large stocks.

Same market discussion, different growth and value readings

A common scenario is a market where bond yields begin falling. Growth stocks may respond positively because lower rate pressure can make future earnings streams more attractive. At the same time, value stocks may also rally if falling yields are interpreted as relief for financial conditions or as support for economically sensitive sectors.

The same yield move can therefore produce different style readings. If growth leads while breadth remains narrow, the market may be rewarding duration-like earnings and large-cap concentration. If value leads with wider sector participation, the market may be pricing broader recovery, cheaper cyclicals, or improved confidence in current earnings.

The useful question is not “which style should be bought?” The useful question is what the style leadership says about participation, risk appetite, valuation pressure, and the quality of market leadership.

Why growth and value rotate

Growth and value can rotate because the market changes what it rewards. In some environments, investors prioritize future expansion, margin scalability, and long-duration earnings. In others, they prioritize current cash flow, valuation support, dividends, or cyclical earnings recovery.

Several forces can influence that rotation:

| Driver | How it can affect growth vs value |

|---|---|

| Interest rates | Higher discount-rate pressure can weigh more heavily on long-duration growth expectations, while lower pressure can support willingness to pay for future growth. |

| Liquidity | Easier liquidity can support risk appetite and valuation expansion; tighter liquidity can increase scrutiny of cash flows and balance-sheet quality. |

| Inflation and reflation | Reflationary environments can support sectors commonly found in value indexes, but this depends on earnings, margins, and credit conditions. |

| Risk appetite | High risk appetite can support growth leadership, but defensive mega-cap growth can also lead when investors crowd into perceived quality. |

| Market breadth | Broad participation makes style leadership more informative than leadership concentrated in a small number of large stocks. |

How to read growth vs value without turning it into a signal

Growth vs value works best as a classification lens. It helps organize which parts of the equity market are being rewarded and what assumptions the market may be making. It becomes weaker when treated as a mechanical timing model.

A cleaner interpretation process is to compare style leadership with other market-structure evidence. If growth is leading, check whether the move is supported by earnings revisions, liquidity conditions, falling rate pressure, and breadth inside growth-heavy sectors. If value is leading, check whether the move is supported by cyclicals, financials, commodities, credit stability, and broader participation.

The distinction should also be separated from sector rotation. Growth and value are style categories, while sectors group companies by business activity. The two overlap, but they are not the same. A style shift can be driven by sector mix, and a sector shift can change the apparent balance between growth and value.

Limits of the growth vs value comparison

Growth vs value is useful, but it has several limits.

| Limit | Why it matters |

|---|---|

| Style labels are broad | Indexes and funds can classify companies differently, and some companies contain both growth and value characteristics. |

| Leadership can be narrow | A few large stocks can make growth or value appear stronger than the average stock in that style group. |

| Valuation is not timing | Expensive stocks can stay expensive, and cheap stocks can stay cheap if the underlying fundamentals or market environment do not improve. |

| Cycle inference can be wrong | Style rotation may reflect positioning, index concentration, rates, sector mix, or earnings revisions rather than a clean business-cycle signal. |

The safest use is therefore comparative and contextual. Growth vs value can help describe what the market is rewarding, but it should be combined with broader evidence before drawing conclusions about regime, cycle phase, or risk appetite.

FAQ

What is the main difference between growth and value?

Growth usually refers to companies priced around expected future expansion, while value usually refers to companies priced around lower valuation, current cash flows, assets, or potential mispricing. The distinction is a style classification, not a rule for what will outperform.

Does growth leadership mean the market is risk-on?

Not by itself. Growth leadership can reflect risk appetite, easier liquidity, lower rate pressure, strong earnings momentum, or narrow concentration in large companies. It needs confirmation from breadth, credit, rates, and sector participation.

Does value leadership mean the cycle is improving?

Not automatically. Value leadership can appear during reflation, cyclical recovery, or valuation rotation, but it can also reflect defensive positioning or temporary mean reversion. The interpretation depends on the surrounding market structure.

Can a stock be both growth and value?

Yes. Some companies can have growth characteristics and still trade at valuations that look attractive compared with their fundamentals. Style labels are useful categories, but they do not capture every detail of an individual company.