Cyclical sectors are more sensitive to economic growth, spending, and earnings cycles. Defensive sectors are less economically sensitive because demand for their products or services is usually more stable or essential. The distinction helps interpret sector leadership and risk appetite, but it is not a buy/sell rule, a return forecast, or proof of the current cycle phase.

For market-cycle analysis, the useful question is not which group is “better.” The useful question is what kind of economic sensitivity the market may be rewarding, avoiding, or balancing at a given point in the cycle.

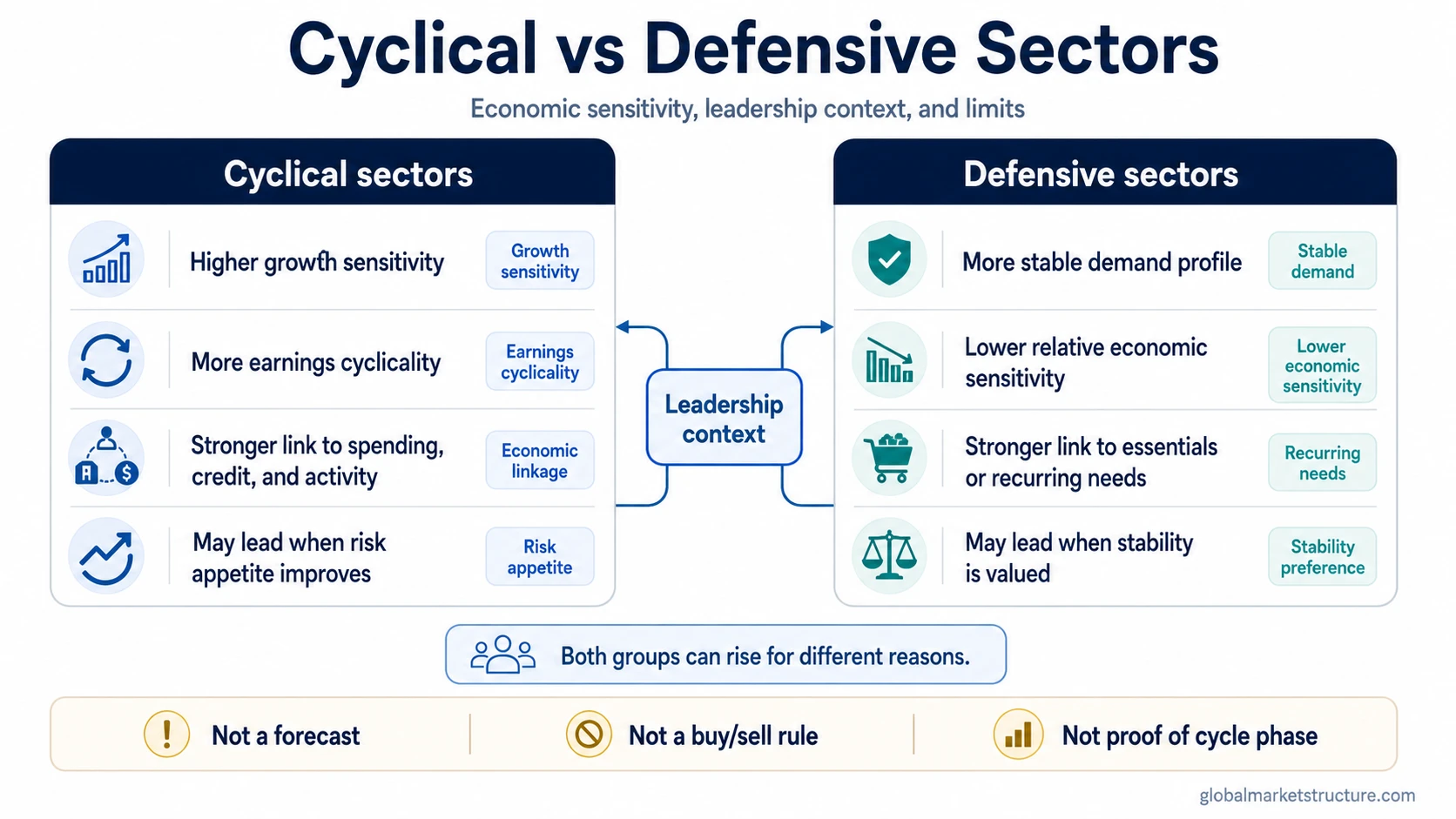

Cyclical vs defensive sectors at a glance

| Comparison point | Cyclical sectors | Defensive sectors |

|---|---|---|

| Core meaning | Sectors whose revenue, earnings, and investor demand tend to move more with the economic cycle. | Sectors whose demand tends to be more stable across different economic conditions. |

| Economic sensitivity | Higher sensitivity to growth, employment, credit conditions, and consumer or business confidence. | Lower relative sensitivity because demand is often tied to essentials or recurring needs. |

| Demand pattern | Demand can strengthen when growth expectations improve and weaken when activity slows. | Demand may hold up better when growth slows, although it can still be affected by margins, rates, regulation, and valuation. |

| Earnings sensitivity | Earnings may accelerate when volume, pricing, and operating leverage improve together. | Earnings may be more stable, but not immune to cost pressure, balance-sheet risk, or industry-specific shocks. |

| Typical leadership context | Often associated with improving growth expectations or stronger risk appetite. | Often associated with uncertainty, slowing growth expectations, or demand for relative earnings stability. |

| What leadership may suggest | Investors may be rewarding economic sensitivity and operating leverage. | Investors may be valuing stability, income characteristics, or lower exposure to the business cycle. |

| Common examples | Often include consumer discretionary, industrials, materials, financials, energy, and parts of technology depending on taxonomy. | Often include consumer staples, utilities, health care, and sometimes telecom-like or infrastructure-linked groups depending on taxonomy. |

| Main limitation | Cyclical does not mean automatic upside, better returns, or a confirmed expansion. | Defensive does not mean risk-free, recession-proof, or guaranteed downside protection. |

What cyclical sectors mean

Cyclical sectors are groups of companies whose business results tend to depend more on economic activity. When households spend more freely, companies invest more aggressively, credit is easier to access, and demand improves, these sectors may experience stronger revenue and earnings momentum.

The mechanism is usually tied to earnings cyclicality. A company with high fixed costs, variable demand, or exposure to discretionary spending can see profits rise quickly when demand improves. The same sensitivity can work in reverse when orders slow, financing tightens, or confidence weakens.

In market-leadership analysis, cyclical strength can suggest that investors are becoming more willing to own economic sensitivity. That interpretation becomes stronger when it is supported by broader evidence, such as improving breadth, credit stability, liquidity conditions, and earnings revisions.

What defensive sectors mean

Defensive sectors are groups of companies whose demand tends to be less sensitive to the business cycle. These sectors often provide essential goods, regulated services, recurring health care needs, or products that households continue buying even when economic conditions weaken.

Defensive does not mean immune. Utilities can be sensitive to interest rates and regulation. Health care can be affected by policy, pricing pressure, and innovation cycles. Consumer staples can face margin pressure, valuation risk, and company-specific execution problems.

In market-leadership analysis, defensive strength can suggest that investors are placing more value on stability, income characteristics, or lower economic sensitivity. That interpretation becomes more meaningful when it appears alongside weaker breadth, wider credit spreads, declining yields, or other signs of caution.

Why the distinction matters in market cycles

The cyclical-versus-defensive distinction helps organize market leadership by economic sensitivity. It gives sector moves a cleaner context than simply saying one sector is strong and another is weak.

Cyclical leadership may point to improving growth expectations, stronger risk appetite, or investors rewarding operating leverage. Defensive leadership may point to caution, demand for earnings stability, falling rate expectations, or concerns that growth is slowing.

The distinction is most useful when it is combined with other evidence. Sector leadership alone cannot identify the current business-cycle phase. A stronger interpretation usually needs confirmation from market breadth, credit conditions, earnings revisions, yield trends, liquidity conditions, and cross-asset risk behavior.

Same market move, different meaning: cyclicals and defensives can both rise during the same period. Cyclicals may rise because investors expect better growth, while defensives may rise because lower yields increase the value of stable cash flows. The shared price direction does not mean the same macro message.

Boundary cases and taxonomy caveats

Sector classification is useful, but it is not perfectly fixed. Some sectors contain both cyclical and defensive characteristics. Technology can include economically sensitive hardware, enterprise software, semiconductors, and recurring-revenue platforms. Communication services can include advertising-sensitive companies as well as more stable subscription or network businesses.

Energy can behave cyclically because it is tied to commodity demand, supply, and capital spending. It can also respond to geopolitical risk, inflation expectations, and supply constraints in ways that do not fit a simple growth-cycle label.

Financials are often treated as cyclical because credit demand, loan growth, capital markets activity, and default risk change with the cycle. But banks, insurers, exchanges, and asset managers can respond differently to yield curves, regulation, credit stress, and market volatility.

Key limitation: sector labels describe sensitivity, not destiny. A defensive sector can underperform during a weak economy if valuation is too high, margins compress, or regulation changes. A cyclical sector can hold up during a slowdown if expectations are already depressed or if industry-specific supply conditions improve.

How this relates to sector rotation

Cyclical versus defensive classification is one input inside sector rotation. Sector rotation studies how market leadership shifts across groups as economic expectations, liquidity, rates, earnings, and risk appetite change.

The classification helps interpret whether leadership is leaning toward economic sensitivity or relative stability. It does not replace a full rotation framework, and it should not be used as a standalone market-timing tool.

A practical rotation review usually asks whether leadership is broadening or narrowing, whether cyclicals are leading with confirmation from credit and earnings data, whether defensives are leading because of caution or rate sensitivity, and whether style leadership confirms or contradicts the sector message.

FAQ

What is the main difference between cyclical and defensive sectors?

Cyclical sectors are more sensitive to economic growth and earnings cycles. Defensive sectors are less sensitive because demand is usually more stable or essential.

Are defensive sectors safe?

No. Defensive sectors may have lower relative economic sensitivity, but they can still face valuation risk, interest-rate risk, regulation, margin pressure, and company-specific problems.

Do cyclical sectors always outperform in expansions?

No. Cyclical sectors may benefit from improving growth expectations, but valuation, earnings quality, credit conditions, and market positioning can change the outcome.

Can cyclical and defensive sectors both rise at the same time?

Yes. Different sectors can rise for different reasons. Cyclicals may respond to better growth expectations, while defensives may hold up because investors still value earnings stability.

Is cyclical versus defensive the same as sector rotation?

No. Cyclical versus defensive is a classification lens. Sector rotation is the broader study of how leadership shifts across sectors as market conditions change.