Inflation affects profit margins through both revenue and cost channels. Margins improve only when selling-price gains, pricing power, or nominal revenue growth exceed input costs, wages, financing costs, and operating expenses. Margins compress when costs rise faster than prices, and the result can differ across gross, operating, and net margin.

For market interpretation, the useful question is not whether inflation is good or bad for margins in every case. The useful question is which part of the margin structure is being affected, whether companies can pass through higher costs, and whether higher nominal sales translate into stronger operating income.

What Changes Margins During Inflation

- Selling prices and nominal revenue may rise during inflation.

- Input costs, wages, logistics, and financing costs often rise at the same time.

- Pricing power determines how much of the cost increase can be passed through.

- Gross, operating, and net margins may move in different directions.

- Sector exposure can change the reading because commodity-linked, capacity-constrained, brand-led, labor-intensive, and rate-sensitive businesses face different cost and pricing channels.

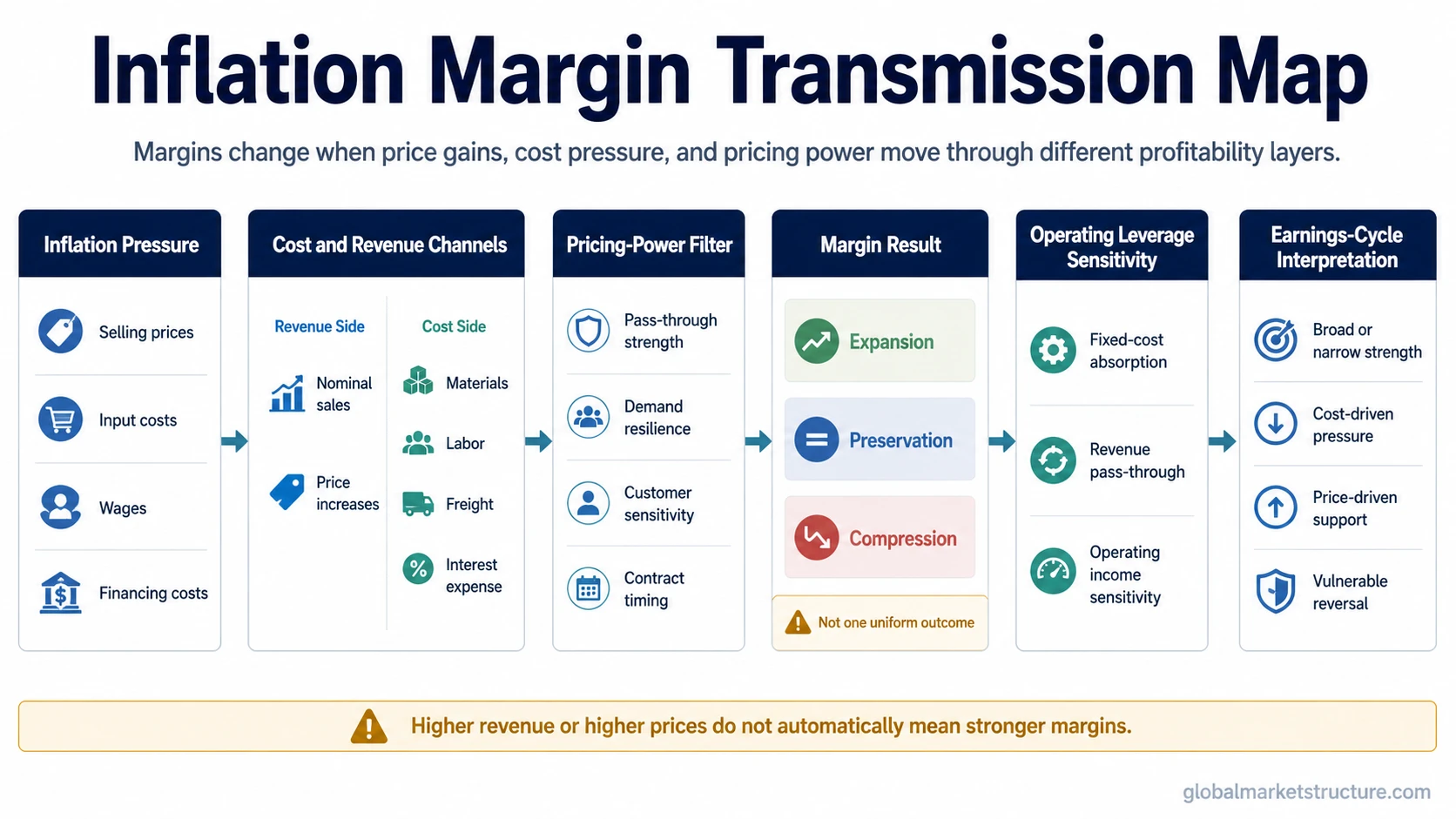

The Inflation-to-Margin Transmission Chain

Inflation pressure reaches margins through a sequence of channels rather than through one simple rule.

- Inflation pressure: the general price environment changes selling prices, costs, wages, and financing conditions.

- Cost and revenue channels: companies may report higher nominal revenue while also facing higher input, labor, freight, rent, energy, or interest costs.

- Pricing-power filter: margin outcomes depend on whether higher costs can be passed through without damaging demand.

- Margin metric effect: gross, operating, and net margins can respond differently because they measure different layers of profitability.

- Operating-income sensitivity: fixed-cost structures can amplify the effect when revenue changes flow through the income statement.

- Earnings-cycle interpretation: margin behavior helps classify whether earnings strength is broad, narrow, cost-driven, price-driven, or vulnerable to reversal.

The sequence prevents a common mistake: reading higher prices or higher sales as automatic evidence of stronger profit margins. Revenue may rise in nominal terms while the margin share of each dollar of sales weakens.

Cost Channels vs Revenue Channels

Inflation may support margins, damage margins, or leave them broadly stable depending on which channel dominates. The same inflation environment can help one sector and hurt another.

| Inflation channel | Possible margin effect | What to check | Interpretation limit |

|---|---|---|---|

| Selling-price increases | Margins may hold or expand if price gains exceed cost growth. | Pricing power, contract terms, customer sensitivity, and demand resilience. | Higher prices may reduce volume if customers resist or trade down. |

| Input-cost inflation | Margins compress when materials, energy, inventory, or supplier costs rise faster than selling prices. | Cost of goods sold, inventory timing, supplier exposure, and commodity sensitivity. | Some cost pressure may be temporary, delayed, or hidden by accounting timing. |

| Wage inflation | Operating margins may come under pressure, especially in labor-intensive sectors. | Labor intensity, productivity, headcount flexibility, and service demand. | Higher wages may also support demand in some consumer-facing areas. |

| Logistics and distribution costs | Gross or operating margins may weaken when transport, storage, or supply-chain costs rise. | Freight exposure, supply-chain structure, and delivery-cost pass-through. | Supply-chain normalization may later reverse part of the pressure. |

| Financing costs | Net margins may fall when higher rates raise interest expense. | Debt maturity, floating-rate exposure, refinancing needs, and balance-sheet leverage. | Financing pressure may not appear in gross margin or operating margin. |

| Nominal revenue growth | Margins may improve if revenue rises faster than variable and fixed costs. | Volume growth, price growth, cost absorption, and operating expense discipline. | Nominal growth does not prove stronger real profitability. |

Why Pricing Power Matters

Pricing power is the filter between inflation and margins. When a company or sector can raise selling prices without losing too much volume, inflation pressure is easier to absorb. When customers resist higher prices, switch to substitutes, or reduce demand, cost pass-through weakens.

Strong pricing power does not eliminate margin risk. Cost increases may arrive before price increases, contracts may reset slowly, and competitive pressure may prevent full pass-through. A sector may look protected early in an inflation cycle and still face pressure later if demand softens or cost inflation broadens.

Why the Margin Metric Matters

Inflation can affect gross margin, operating margin, and net margin in different ways. A single margin number can hide where the pressure is coming from.

| Margin metric | What it captures | Inflation interpretation |

|---|---|---|

| Gross margin | Revenue after direct production or service costs. | Useful for seeing whether selling prices are keeping up with direct input costs. |

| Operating margin | Revenue after direct costs and operating expenses. | Useful for seeing whether wages, logistics, rent, sales costs, and overhead are pressuring profitability. |

| Net margin | Profit after operating costs, interest, taxes, and other below-operating items. | Useful when higher rates, refinancing costs, or tax effects change the final profit share. |

Gross margin can improve while operating margin weakens if direct costs are controlled but wages or overhead rise. Operating margin can hold while net margin weakens if interest expense increases. Inflation analysis becomes weaker when all margin types are treated as interchangeable.

When Inflation Compresses Margins

Margin compression occurs when costs rise faster than revenue or selling prices. During inflation, that can happen through materials, wages, freight, energy, rent, interest expense, or a demand slowdown that prevents full price pass-through.

A practical scenario is a sector with rising nominal sales but even faster growth in wages, freight, and interest costs. Reported revenue may look stronger, but operating margin can weaken because each dollar of sales carries less operating profit. The earnings signal is then more fragile than the revenue line suggests.

When Inflation Preserves or Expands Margins

Inflation may preserve or expand margins when price increases exceed cost increases, when demand remains resilient, or when a sector benefits from higher selling prices before its own cost base catches up. Sector exposure can change the reading: commodity-linked, capacity-constrained, brand-led, labor-intensive, and rate-sensitive businesses may face different cost and pricing channels.

That interpretation still needs caution. A durable reading is stronger when pricing power, volume resilience, and cost control persist together; a weaker reading may reflect inventory timing, delayed cost recognition, sector concentration, or a short-lived price spike. Margin expansion in one area does not automatically prove that margins are improving across the whole economy.

Operating Leverage and Earnings-Cycle Sensitivity

Operating leverage becomes important when inflation changes revenue faster than fixed costs. If nominal revenue rises while fixed costs remain relatively stable, operating income can rise faster than sales. If demand weakens while fixed costs remain in place, operating income can fall faster than revenue.

This is why inflation and margins matter for earnings-cycle interpretation. A company or sector with high fixed costs may be highly sensitive to small revenue changes. Inflation may magnify that sensitivity when price, volume, and cost absorption move in different directions.

Common Mistakes and Interpretation Limits

- Rising sales do not automatically mean stronger margins. Nominal revenue can rise while costs rise faster.

- Higher prices do not automatically mean stronger real profitability. Unit volume, demand quality, and cost inflation still matter.

- One sector does not represent the whole profit cycle. Inflation can expand margins in one industry and compress them in another.

- Gross margin, operating margin, and net margin should not be merged into one signal. Each metric captures a different layer of cost pressure.

- Margin changes do not prove a single cause of inflation. Profit behavior, cost shocks, demand, policy, wages, supply constraints, and sector mix can interact.

How to Read Profit Margins During Inflation

A stronger reading separates observed numbers from interpretation. First, identify whether revenue growth is price-driven, volume-driven, or both. Next, compare that growth against direct costs, operating expenses, wages, logistics, and financing costs. Then check whether the margin effect is broad across sectors or concentrated in a few industries.

The cleanest margin interpretation appears when price gains, cost behavior, demand, and margin metric all point in the same direction. The interpretation weakens when revenue rises but operating costs rise faster, when only one sector benefits, or when net margin is pressured by financing costs while gross margin looks stable.

Where the Margin Reading Connects

Profit margins provide the core earnings-cycle definition. Margin compression describes the narrower condition where costs outpace pricing or revenue. Inflation is the broader macro price-level driver. Operating leverage explains fixed-cost sensitivity after revenue changes.

FAQ

Do profit margins usually rise during inflation?

Profit margins do not have one universal inflation response. They can rise when pricing power and nominal revenue gains exceed cost growth, but they can fall when input costs, wages, logistics, financing costs, or operating expenses rise faster than prices.

Why can revenue rise while profit margins fall?

Revenue can rise because prices are higher, but margins can fall if the cost of producing, delivering, financing, or supporting that revenue rises even faster. Nominal sales growth is not the same as stronger profitability.

Why does pricing power matter for margins during inflation?

Pricing power determines whether higher costs can be passed through to customers without a large drop in demand. Weak pricing power leaves more of the inflation burden inside the cost structure.

Can gross margin improve while net margin weakens?

Yes. Gross margin can improve if selling prices exceed direct input costs, while net margin weakens because operating expenses, interest costs, taxes, or other below-operating items move against the company or sector.