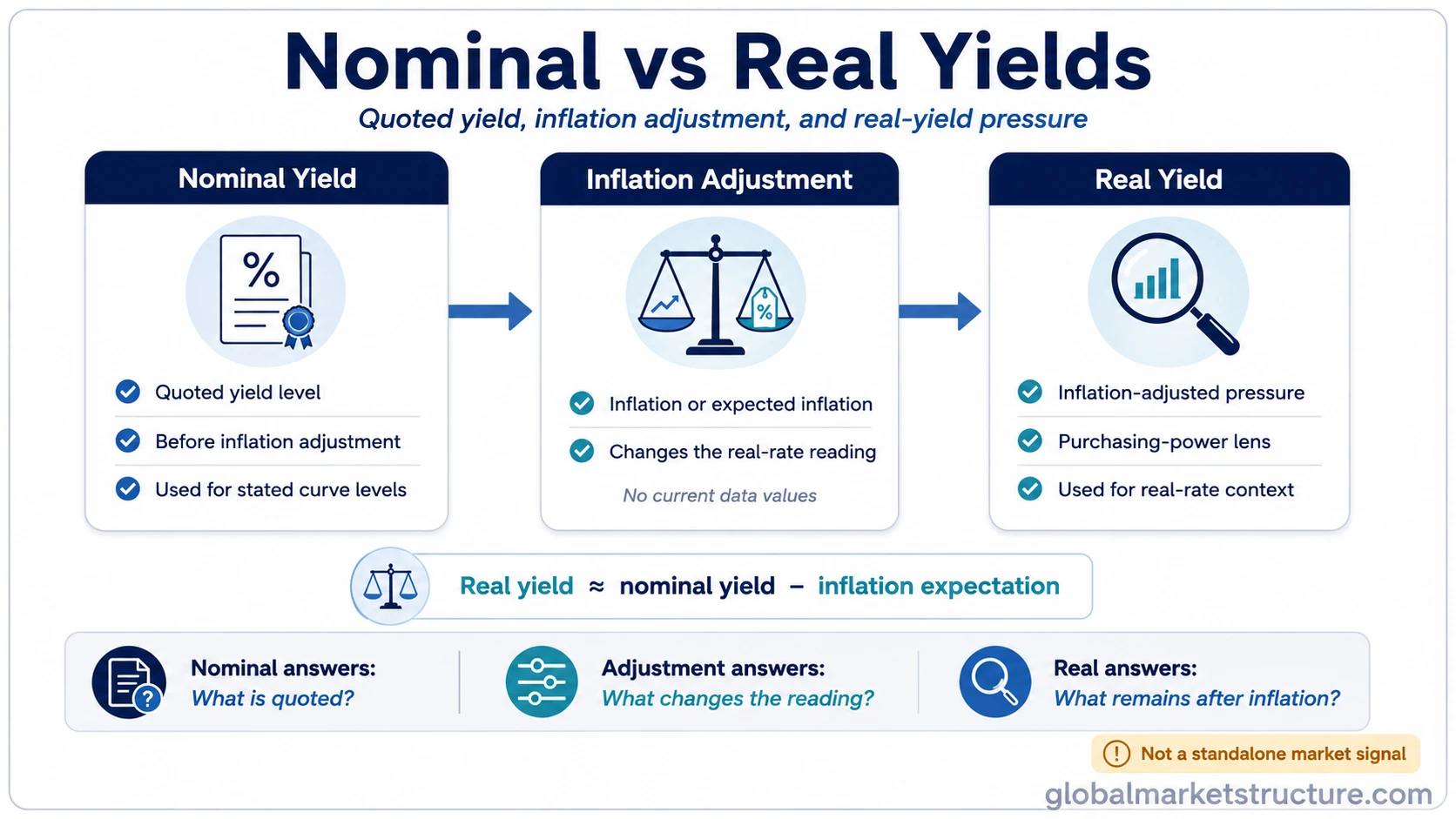

Nominal yields are quoted yields before inflation adjustment. Real yields adjust that yield for inflation or inflation expectations, which makes them useful for reading purchasing-power pressure and real-rate conditions. The two measures are not rivals. Each one answers a different rates and market-structure question.

Core distinction: Nominal yields describe the stated yield level. Real yields describe the yield after inflation or expected inflation is considered.

The useful question is not which yield is better. Nominal yields help organize the quoted curve, benchmark rates, and cash-flow terms. Real yields help interpret how much yield remains after inflation expectations are included.

Nominal vs Real Yields: The Core Difference

A nominal yield is the visible yield quoted on a bond, Treasury, or rate instrument before adjusting for inflation. A real yield is the inflation-adjusted version of that yield. In a simple form, real yield is often approximated as nominal yield minus inflation or expected inflation.

Simple relationship: Real yield is approximately nominal yield minus inflation or expected inflation.

That relationship changes the interpretation of the same quoted yield. A 5% nominal yield does not carry the same real-rate meaning when expected inflation is 2% as it does when expected inflation is 4%. The nominal number is the same, but the inflation-adjusted reading is different.

Quick Comparison Table

| Yield lens | What it measures | Best used for | What it does not prove | Common mistake |

|---|---|---|---|---|

| Nominal yield | The stated or quoted yield before inflation adjustment. | Reading quoted curve levels, benchmark yield levels, and stated cash-flow terms. | It does not show purchasing-power pressure by itself. | Treating the quoted yield as the full real return or full real-rate signal. |

| Real yield | The yield after adjusting for inflation or inflation expectations. | Reading inflation-adjusted pressure, real-rate conditions, and purchasing-power context. | It does not predict market direction by itself. | Treating real yield as the only yield that matters or as a standalone market signal. |

Common confusion: a quoted yield can look high in nominal terms while offering less inflation-adjusted pressure if inflation expectations are also high. The mistake is treating the visible yield quote as the complete real-rate reading.

The comparison works best when both measures stay separate. Nominal yields answer what the market is quoting. Real yields answer how that quote looks after inflation expectations change the real-rate backdrop.

How Inflation Changes the Yield Lens

Inflation changes the interpretation because a stated yield can buy less in real terms when prices are rising quickly. Expected inflation matters because markets often price forward-looking inflation conditions rather than only the last reported inflation number.

When expected inflation rises while nominal yields stay flat, real-yield pressure can fall. When expected inflation falls while nominal yields stay flat, real-yield pressure can rise. The quoted yield level has not changed in either case, but the inflation-adjusted reading has changed.

Inflation expectations are the bridge between the two yield measures because they help explain why the same nominal yield can imply a different real-yield backdrop.

Same Nominal Yield, Different Real-Yield Pressure

Example scenario: A Treasury yield is quoted at 5%. If expected inflation is near 2%, the approximate real-yield lens is around 3%. If expected inflation is near 4%, the approximate real-yield lens is around 1%. The nominal yield is unchanged, but the inflation-adjusted pressure is much higher in the first case than in the second.

The numbers are simplified to isolate the inflation adjustment, not to describe current market levels. They show why a stable quoted yield can carry a different real-yield interpretation when inflation expectations change.

| Nominal yield | Inflation expectation | Approximate real-yield lens | Interpretation effect |

|---|---|---|---|

| 5% | 2% | About 3% | Higher inflation-adjusted yield pressure. |

| 5% | 4% | About 1% | Lower inflation-adjusted yield pressure. |

When Nominal Yields Are the Better Lens

Nominal yields are usually the cleaner measure when the question is about quoted market levels. They help organize the visible yield curve, benchmark Treasury yields, bond coupon comparisons, borrowing-rate references, and the stated terms attached to cash flows.

A nominal-yield view is also useful when comparing levels across maturities. The yield curve is usually discussed first through nominal yields because the curve displays quoted yields across different maturities.

The limitation is that nominal yields do not isolate whether the market is receiving more or less inflation-adjusted compensation. A rising nominal yield can reflect changes in expected real rates, inflation expectations, term premium, growth expectations, liquidity premium, or risk compensation.

When Real Yields Are the Better Lens

Real yields are usually the cleaner measure when the question is about inflation-adjusted pressure. They help clarify whether a quoted yield still looks restrictive, neutral, or loose after inflation expectations are considered.

Real-yield interpretation can help frame discount-rate context, purchasing-power pressure, and broader financial-condition readings. The wording needs care: real yields can affect how rate-sensitive markets are interpreted, but they do not mechanically determine equity, bond, gold, or currency direction on their own.

Important boundary: Real yields are a measurement lens, not a complete market forecast. Their interpretation changes when growth expectations, liquidity conditions, credit spreads, positioning, earnings expectations, and risk appetite change at the same time.

TIPS, Breakevens, and What They Do Not Replace

TIPS yields can serve as a market reference for real yields because Treasury Inflation-Protected Securities are designed around inflation-adjusted principal mechanics. That does not make TIPS the entire real-yield concept. Real yield is the broader inflation-adjusted yield measure.

Breakeven inflation is an adjacent concept. It is commonly read as the spread between nominal Treasury yields and inflation-protected Treasury yields for a comparable maturity. It is market-implied, not the same thing as realized inflation.

The practical boundary is simple: TIPS and breakevens can help observe market pricing, but they do not turn nominal versus real yields into product advice or a complete allocation framework.

Yield Curve Shape Versus Real-Yield Pressure

Nominal curve shape and real-yield pressure are related rates concepts, but they answer different questions. Curve shape compares yields across maturities. Real-yield pressure compares a yield measure against inflation or expected inflation.

A curve can steepen, flatten, or invert for reasons that include policy expectations, inflation expectations, term premium, growth concerns, liquidity demand, and risk compensation. A real-yield lens adds another layer, but it does not replace the curve-shape question.

The clean interpretation separates level, slope, and inflation adjustment. Nominal yields help with level and curve quotation. Real yields help with inflation-adjusted pressure. Curve shape helps with maturity structure.

Common Mistakes and Limitations

Mistake 1: Calling real yields the true yield and nominal yields wrong. Real yields answer a different question, but nominal yields remain necessary for quoted market levels and cash-flow terms.

Mistake 2: Treating TIPS yields as the whole real-yield concept. TIPS can be a useful market reference, but the conceptual real-yield lens is broader than one instrument quote.

Mistake 3: Assuming nominal yield increases prove tightening. Nominal yields can rise for several reasons, including inflation expectations, term premium, growth expectations, liquidity premium, and risk compensation.

Mistake 4: Treating real yields as an asset-direction model. Real yields can affect market interpretation, but they do not predict stocks, gold, bonds, or risk appetite in isolation.

Mistake 5: Using either yield lens as a buy or sell signal. Yield measurement and market action are separate jobs. A yield reading may shape context, but it does not create an investment instruction.

Related Rates Concepts

Nominal and real yields sit inside a broader rates structure. Nominal yields help organize the quoted market level, real yields add inflation-adjusted pressure, and curve shape organizes maturity relationships.

Term premium can also affect quoted yields because investors may demand additional compensation for holding longer-maturity bonds. That makes term premium a separate concept from both nominal yield and real yield.

The cleanest route is to keep the measures separate: use nominal yields for stated levels, real yields for inflation-adjusted pressure, and curve structure for maturity comparison.

FAQ

How do you calculate real yield from nominal yield?

A simple approximation subtracts inflation or expected inflation from the nominal yield. For example, a 5% nominal yield with 2% expected inflation gives an approximate 3% real-yield lens. Exact calculations can vary, especially when compounding and market pricing details matter.

Are TIPS yields the same as real yields?

TIPS yields can be used as a market reference for real yields, but they are not the entire concept. Real yield is the broader inflation-adjusted yield lens. TIPS are one instrument family that can help observe part of that lens in Treasury markets.

Can nominal yields rise while real yields fall?

Yes. That can happen if inflation expectations rise faster than nominal yields. The quoted yield may be higher, but the inflation-adjusted yield lens may still fall if the inflation adjustment increases by more than the nominal yield.

Do real yields predict markets?

No. Real yields can influence market interpretation, especially around discount-rate pressure and purchasing-power context, but they are not a standalone market forecast. Growth, liquidity, credit conditions, earnings expectations, positioning, and risk appetite can change the final market response.