A taper tantrum is a sharp market reaction to expectations that a central bank may slow asset purchases, most often referring to the 2013 Federal Reserve taper episode. The reaction matters because investors can quickly reprice policy support, long-term Treasury yields, risk appetite, and global capital flows. It is not tapering itself, quantitative tightening, a rate hike, or a standalone market signal.

Taper tantrum meaning: a taper tantrum is a market reaction to the expected slowing of central-bank asset purchases. The phrase is closely associated with 2013, when Federal Reserve communication about possible tapering led investors to reassess future policy support and reprice long-term rates. The core idea is an expectations shock, not the mechanical act of tapering alone.

Key Points

- A taper tantrum describes a market reaction to expected tapering, not the tapering process itself.

- The 2013 episode is the main reference point because investors rapidly reassessed future Federal Reserve asset purchases and policy support.

- The transmission channel usually runs through long-term rates, especially Treasury-yield repricing.

- Risk assets and emerging-market assets may react when higher U.S. yields change liquidity, currency, and capital-flow conditions.

- The term is not a buy signal, sell signal, rate-hike label, or automatic template for future tapering periods.

What Is a Taper Tantrum?

A taper tantrum is an abrupt repricing that can happen when investors believe a central bank may reduce the pace of asset purchases sooner, faster, or more aggressively than markets expected.

The word “taper” refers to slowing the pace of asset purchases, not immediately reversing the central bank balance sheet. The word “tantrum” describes the market reaction: yields can move quickly, volatility can rise, and risk appetite can weaken as investors adjust to a less supportive policy path.

In Global Market Structure terms, the useful reading is not “the central bank tapered, so markets must fall.” The useful reading is that policy-support expectations changed, and that change moved through rates, liquidity expectations, currency pressure, and cross-asset risk pricing.

Why the 2013 Taper Tantrum Mattered

The 2013 taper tantrum became the reference episode because Federal Reserve communication about a possible slowing of asset purchases caused investors to reassess how long extraordinary policy support would continue.

The reaction was visible in long-term rate markets. When investors expected less future bond-buying support, duration risk was repriced and Treasury yields rose quickly. That rate move became the transmission point for wider market interpretation.

The episode also mattered beyond U.S. bonds. Higher U.S. yields can change the relative appeal of dollar assets, affect currency pressure, tighten financial conditions for some borrowers, and influence capital flows into or out of emerging markets. That does not mean every emerging market reacts the same way, but it explains why taper tantrum is treated as a global market-structure concept rather than only a Federal Reserve phrase.

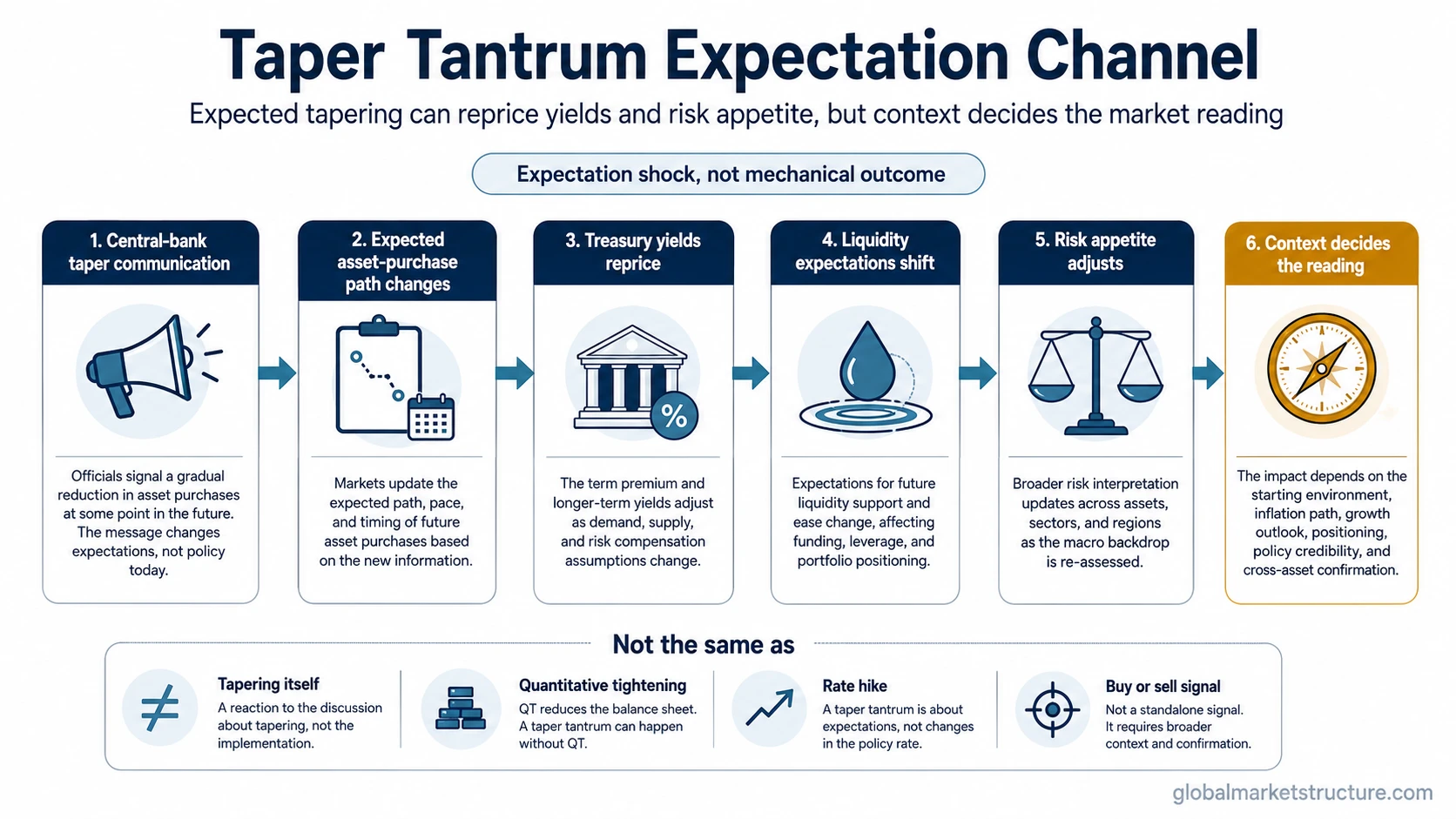

How the Taper Tantrum Mechanism Works

A taper tantrum is best understood as an expectation channel:

- Central-bank communication changes expectations. Investors hear that asset purchases may slow sooner or faster than previously assumed.

- The expected asset-purchase path changes. Markets reassess how much policy support may remain in the system.

- Long-term rates reprice. Bond investors adjust duration exposure, and Treasury yields can rise quickly.

- Liquidity expectations shift. Less expected central-bank support can make financial conditions feel tighter even before balance-sheet contraction begins.

- Risk appetite adjusts. Equities, credit, currencies, and emerging-market assets may react as investors reprice risk.

- Context decides the interpretation. The same yield move can mean different things if it is driven by growth optimism, inflation pressure, bond supply, or a policy-support shock.

Practical Scenario

A central bank signals that asset purchases may slow sooner than investors expected. Bond investors reprice the expected policy-support path, long-term Treasury yields rise quickly, and risk assets or emerging-market assets react to the shift in discount rates, liquidity expectations, and capital-flow pressure.

The useful reading is the expectation shock. It is not proof that every future taper will create the same market outcome.

Tapering vs Taper Tantrum

Fed tapering is the policy process of slowing the pace of asset purchases. A taper tantrum is the market reaction when investors rapidly reprice what that slowing may mean for future policy support, rates, liquidity, and risk appetite.

The distinction matters because a central bank can taper without causing a large tantrum. Markets react most strongly when the communication, timing, inflation backdrop, positioning, or yield sensitivity forces investors to change assumptions quickly.

What a Taper Tantrum Is Not

| Confused term | Why it is different | Correct reading |

|---|---|---|

| Tapering | Tapering is the policy action of slowing asset purchases. | A taper tantrum is the market reaction to changed expectations around that action. |

| Quantitative easing | Quantitative easing is the asset-purchase program itself. | A taper tantrum can happen when investors expect the pace of those purchases to slow. |

| Quantitative tightening | Quantitative tightening involves balance-sheet runoff or contraction. | A taper tantrum can occur before QT if investors reprice the future policy path. |

| Rate hike | A rate hike changes the policy rate directly. | A taper tantrum can move long-term yields through expectations even without an immediate rate hike. |

| Hawkish tone | Hawkish communication can affect expectations, but tone alone is not the event. | The taper tantrum label fits when markets reprice policy support and rates sharply around taper expectations. |

| Market-direction signal | The phrase describes a macro repricing episode, not a trading instruction. | It can inform market interpretation, but it does not determine timing, direction, or positioning by itself. |

Important Limitation

The 2013 taper tantrum should not be treated as an automatic playbook for every future tapering period. Market reaction depends on the inflation backdrop, growth expectations, starting yield levels, investor positioning, central-bank communication, liquidity conditions, and global risk appetite.

A rise in yields is also not always a taper tantrum. Long-term rates can rise because growth expectations improve, inflation risk increases, Treasury supply changes, term premium rises, or investors demand more compensation for duration risk. The taper-tantrum reading becomes stronger when the move is clearly tied to a policy-support expectation shock.

How to Interpret a Taper-Tantrum-Style Move

A taper-tantrum-style move is most useful as a framework for reading policy expectations through rates. The first question is whether investors are repricing the expected path of central-bank support. The second question is whether that repricing is visible in Treasury yields, volatility, credit conditions, currency pressure, or emerging-market stress.

The interpretation becomes more macro-relevant when several markets confirm the same pressure at the same time. For example, rising long-term yields, a stronger dollar, weaker risk appetite, and stress in rate-sensitive or external-financing-sensitive markets can point to a broader tightening in financial conditions.

The interpretation weakens when the move is isolated, driven by stronger growth expectations, or absorbed without wider liquidity stress. A taper tantrum is therefore a context label, not a mechanical forecast.

Common Misreadings

- “Tapering always crashes markets.” Tapering can be absorbed if communication is gradual, positioning is stable, and financial conditions remain manageable.

- “A taper tantrum is the same as QT.” QT is balance-sheet contraction. A taper tantrum is an expectation shock around reduced purchase support.

- “A taper tantrum is a rate hike.” It can affect long-term yields without an immediate policy-rate increase.

- “The 2013 episode predicts the next one.” The 2013 episode is a reference case, not a universal market template.

- “The phrase is a trading signal.” It describes a macro repricing channel, not a buy or sell instruction.

Related Concepts

Fed tapering: separates the policy action of slowing asset purchases from the market reaction around that expected slowing.

Treasury yields: show where policy-support repricing is often most visible in the rates market.

Quantitative easing and quantitative tightening: clarify the difference between asset purchases, slower purchases, and balance-sheet runoff.

Hawkish policy tone: belongs to the communication layer, while taper tantrum describes the market reaction around taper expectations.

FAQ

What caused the 2013 taper tantrum?

The 2013 taper tantrum followed a rapid investor reassessment of future Federal Reserve asset purchases after communication suggested that the pace of purchases could slow. The reaction moved through long-term rate repricing and broader risk-market interpretation.

Is taper tantrum the same as tapering?

No. Tapering is the policy action of slowing asset purchases. A taper tantrum is the market reaction when investors quickly reprice expected policy support, yields, liquidity conditions, and risk appetite around that expected slowing.

Does tapering always cause a taper tantrum?

No. Market reaction depends on communication, inflation and growth context, starting yield levels, liquidity conditions, investor positioning, and broader risk appetite. Tapering can occur without the same kind of sharp repricing.

Is a taper tantrum a trading signal?

No. A taper tantrum is a macro interpretation label for a policy-expectation and yield-repricing shock. It does not determine market direction, timing, or positioning by itself.