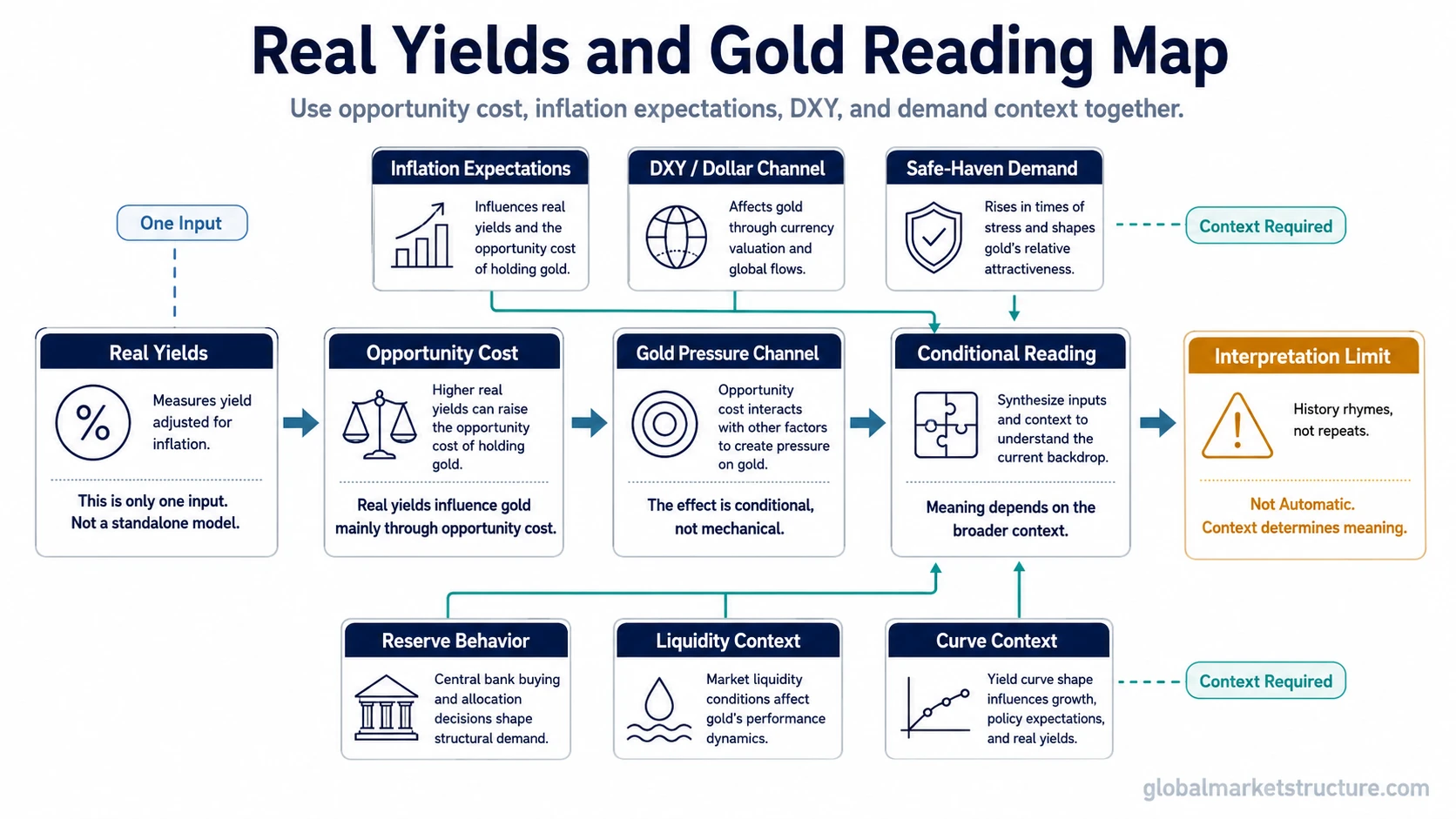

Real yields help explain gold because they show the inflation-adjusted return available from yield-bearing assets. When real yields rise, gold can face a higher opportunity cost; when real yields fall, that pressure can ease. The relationship is conditional because DXY, inflation expectations, safe-haven demand, reserve behavior, liquidity, and curve context can change the reading.

What it means: Real yields are useful for reading gold because they separate nominal rates from inflation expectations.

Why it matters: Gold does not pay income, so higher inflation-adjusted yields can make yield-bearing alternatives more competitive.

What it does not mean: Real yields do not forecast gold by themselves, and the relationship should not be read as an automatic inverse rule.

Real Yields in Gold Context

Real yields are yields adjusted for expected inflation. In gold analysis, the useful question is not only whether yields are rising or falling, but whether the return available after inflation is becoming more or less attractive compared with holding a non-yielding asset.

The main intermarket pressure point is the opportunity cost of holding gold relative to inflation-adjusted safe yield. When that yield becomes more competitive, gold may face more pressure. When that yield becomes less competitive, the pressure may ease. The reading becomes unclear when dollar, liquidity, reserve-demand, or defensive-demand channels move in a different direction.

The Opportunity-Cost Mechanism

Gold can face pressure when real yields rise because investors can receive more inflation-adjusted return from yield-bearing assets. That does not force gold lower, but it can make the relative cost of holding gold higher.

Gold may receive support when real yields fall because the inflation-adjusted return from competing yield-bearing assets becomes less attractive. This is a pressure channel, not a forecast. The reading is stronger when the real-yield move is broad, persistent, and consistent with the surrounding dollar, liquidity, and macro context.

Key limitation: Real yields describe one part of gold’s macro setting. Gold may also respond to dollar strength, inflation uncertainty, policy confidence, reserve demand, stress demand, liquidity conditions, and positioning.

Real Yields vs Nominal Yields

Nominal yields alone can mislead gold interpretation because they do not show how much of the yield move comes from inflation expectations. A rising nominal yield can mean tighter real-rate pressure if inflation expectations are stable or falling. It can mean something different if inflation expectations are rising at the same time.

For gold, the split matters. A nominal yield rise driven by stronger real yields can increase opportunity cost. A nominal yield rise driven mainly by higher inflation expectations may not create the same pressure, especially if investors are also questioning policy credibility or seeking inflation protection.

Inflation Expectations Change the Reading

Real yields depend on the relationship between nominal yields and expected inflation. That makes inflation expectations central to the gold reading. If nominal yields rise but inflation expectations rise faster, real-yield pressure may not tighten. If nominal yields are stable while inflation expectations fall, real yields can rise even without an obvious move in headline rates.

A gold reading based only on Treasury yields can therefore be incomplete. The market may be reacting to the real return after inflation, not simply to the visible level of nominal yields.

DXY and the Dollar Channel

The DXY Index can amplify or offset the real-yield reading. A stronger dollar may add pressure to gold because gold is commonly quoted in dollars. A weaker dollar may ease that pressure even when real yields are not sending a clean supportive signal.

DXY is still only a context input. It does not explain every gold move, and it should not replace the real-yield, inflation-expectation, reserve-demand, and stress-demand checks. The useful reading comes from how these channels line up or conflict.

Condition, Implication, and Limitation Map

| Condition | Possible Gold Interpretation | Limitation / What to Check Next |

|---|---|---|

| Real yields rise while inflation expectations are stable or falling | Opportunity cost may increase for holding gold | Check whether DXY strength, liquidity pressure, or risk-off demand is also present |

| Real yields fall while inflation expectations remain firm | Opportunity-cost pressure may ease | Check whether dollar strength or tightening liquidity is offsetting the supportive reading |

| Nominal yields rise but inflation expectations rise faster | Headline rates may look restrictive while real-yield pressure is less clear | Separate nominal yield movement from the inflation-adjusted yield signal |

| DXY strengthens while real yields are falling | The real-yield channel may look supportive, but dollar pressure can complicate the move | Check whether the dollar move reflects liquidity stress, growth fear, or policy divergence |

| Gold rises while real yields are rising | Demand may be coming from safe-haven flows, reserve behavior, inflation uncertainty, or policy-confidence concerns | Avoid treating the move as a failure of all macro logic; identify which channel is dominant |

| One real-yield point gives a strong signal | The reading may be useful but incomplete | Check curve context, persistence, liquidity, and whether the move is broad across maturities |

Failure-Mode Example

Imagine real yields are rising. The first reading is more cautious for gold because the opportunity cost of holding a non-yielding asset is increasing.

That reading is incomplete if another channel is dominating the marginal demand for gold. Safe-haven demand may be rising, reserve buyers may remain active, or the dollar may be weakening at the same time.

A stronger interpretation compares real-yield pressure with DXY, inflation expectations, liquidity conditions, and evidence of defensive demand. A weaker interpretation relies on the real-yield move alone and ignores why gold is being demanded in that environment.

What the Relationship Does Not Mean

Real yields do not predict gold by themselves. They describe an opportunity-cost channel that may be overridden or weakened by other macro forces.

Nominal yields are not enough. Gold interpretation depends on the inflation-adjusted yield, not only the visible headline yield.

One real-yield measure is not the whole rate regime. Curve shape, maturity point, persistence, liquidity, and policy expectations can change the message.

DXY is not a complete gold model. The dollar can change the reading, but gold may also respond to reserve behavior, safe-haven demand, inflation uncertainty, and confidence in policy.

How to Read Real Yields and Gold Together

A safer reading starts with the opportunity-cost channel, then checks whether other intermarket signals confirm or conflict with it. Real yields answer one question: is the inflation-adjusted return from yield-bearing assets becoming more or less competitive against gold?

The next step is context. Inflation expectations explain the real-yield move. DXY shows whether the dollar channel is adding pressure or relief. Defensive demand, reserve behavior, and liquidity conditions help explain why gold may not respond in a clean inverse pattern.

This is also where gold connects to the broader real assets framework. Gold can behave as a monetary asset, defensive asset, inflation-sensitive asset, or reserve-confidence asset depending on the regime. Real yields help interpret that mix, but they do not replace it.

Related Concepts

Real Yields: Use the full real-yields concept when you need the broader definition, rate structure, and inflation-adjusted yield mechanics.

DXY Index: Use the dollar index context when the gold move may be affected by dollar strength, policy divergence, or global dollar pressure.

Real Assets: Use the real-assets context when gold is being read alongside inflation expectations, commodities, policy confidence, and defensive demand.