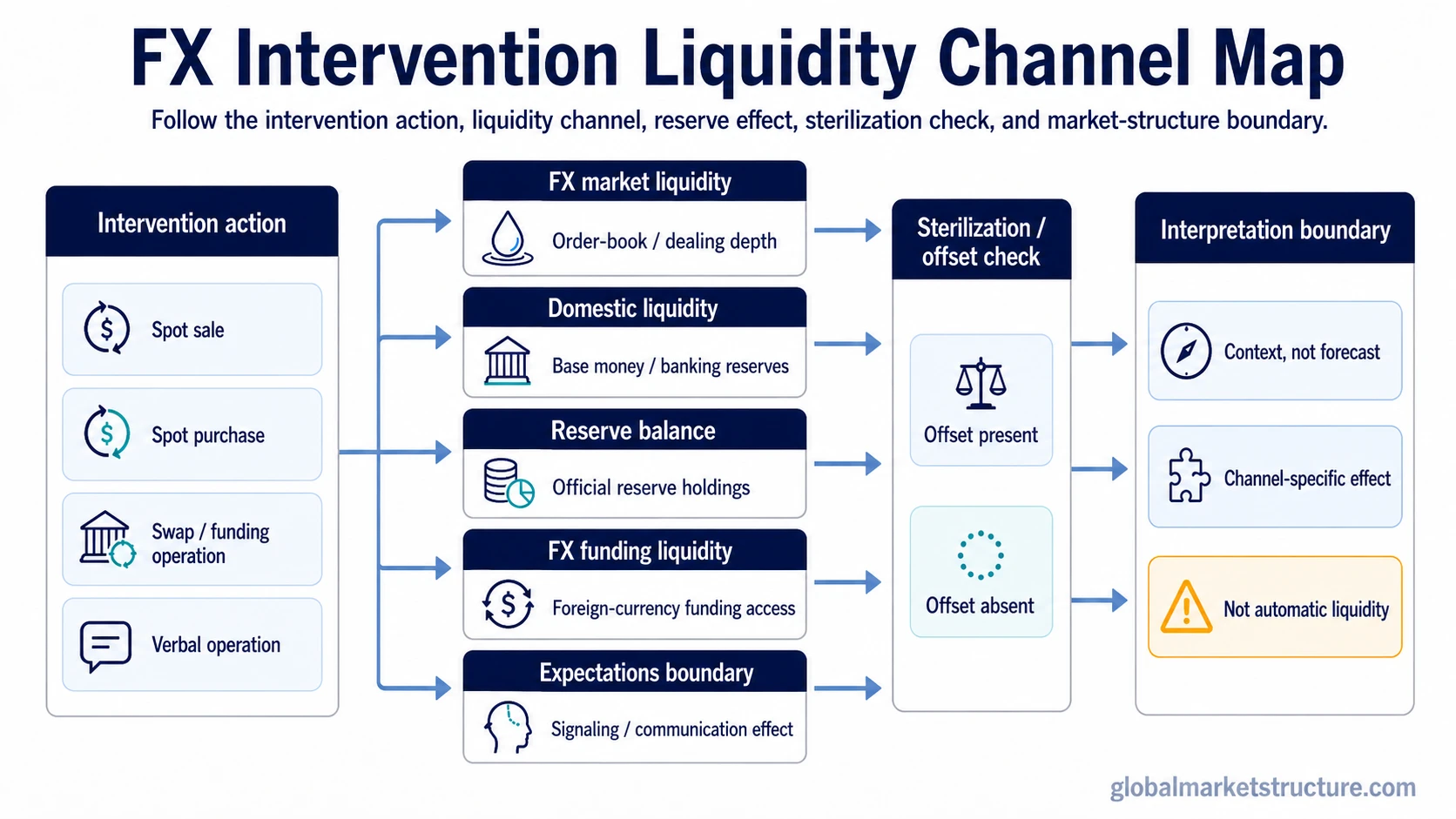

FX intervention and liquidity are connected through the channel used. A central bank action can support FX market functioning, change reserve balances, affect domestic liquidity if it is not sterilized, or provide temporary FX funding liquidity through swaps or related operations. It does not automatically create broad liquidity, prove currency direction, or create a trade signal.

Key Points

- FX intervention has to be read by channel, not by the word intervention alone.

- FX market liquidity, domestic liquidity, reserve balances, and funding liquidity can move differently.

- Sterilization can offset or change the domestic liquidity effect of an intervention.

- The liquidity reading is market-structure context, not a forecast or trading instruction.

What FX Intervention and Liquidity Means

Foreign exchange intervention is an official action intended to influence currency conditions, market functioning, or foreign-exchange availability. Liquidity describes how easily money, funding, or assets can move through a market without creating stress or large price impact.

The important distinction is that intervention is an action, while liquidity is an effect that may appear in more than one place. A reserve sale, a reserve purchase, a swap line, or a signaling operation can point to different liquidity conditions.

For interpretation, the useful question is not simply whether a central bank intervened. The useful question is which balance sheet, market, funding channel, or reserve stock was affected.

Liquidity Channels to Separate

FX intervention can touch several liquidity channels at once, but the channels should not be collapsed into one broad reading.

FX market liquidity: whether participants can obtain or trade foreign currency without severe market disruption.

Domestic liquidity: whether local-currency money-market conditions become easier or tighter after the operation.

Reserve-balance effect: how the central bank’s stock of foreign exchange reserves changes.

Funding liquidity: whether banks, firms, or official institutions gain access to foreign-currency funding through swaps or similar arrangements.

These channels can point in different directions. An action that improves foreign-currency availability may still tighten local-currency conditions unless another operation offsets that effect.

How Intervention Can Inject, Drain, Redistribute, or Neutralize Liquidity

Intervention does not have one automatic liquidity effect. It can inject liquidity into one channel, drain another channel, redistribute liquidity across currencies, or leave the net domestic effect mostly neutral.

A spot FX sale from reserves may supply foreign currency to the market. At the same time, it can remove local currency from the domestic system if the central bank receives local currency in exchange and does not offset the effect.

A spot FX purchase can work differently. It may increase reserve holdings and add local currency into the domestic system, but the broader market effect still depends on sterilization, banking-system conditions, and whether the operation is large enough to matter for liquidity conditions.

A swap or funding operation may not primarily signal a currency target. It may show that foreign-currency funding access has become the more important channel to monitor.

Why Sterilization Changes the Reading

Sterilization is the boundary that often changes the liquidity interpretation. When a central bank offsets the domestic money-market effect of FX intervention, the visible FX action and the domestic liquidity effect can diverge.

Unsterilized intervention can affect domestic liquidity more directly because the local-currency side of the operation remains in the banking system or is removed from it. Sterilized intervention uses offsetting operations to reduce, neutralize, or reshape that domestic effect.

This is why a reserve transaction should not be read as automatic liquidity creation or automatic liquidity withdrawal. The final interpretation depends on the instrument, the local-currency offset, the reserve effect, and the funding stress around the operation.

Condition, Liquidity Channel, Interpretation, and Limitation

| Intervention condition | Liquidity channel affected | What it may indicate | Main limitation |

|---|---|---|---|

| Spot FX sale from reserves | FX market liquidity and reserve balance | The central bank may be supplying foreign currency to reduce market pressure or improve currency availability. | It may drain local-currency liquidity unless offset, and it does not prove a durable currency outcome. |

| Spot FX purchase | Reserve balance and domestic liquidity | The central bank may be accumulating foreign currency while adding local currency into the domestic system. | The effect can be sterilized, and reserve accumulation does not automatically create broad asset-price support. |

| Sterilized intervention | Domestic liquidity offset | The authority may want to influence FX conditions without leaving the full local-currency liquidity effect in place. | The FX action is visible, but the net domestic effect depends on the offsetting operation. |

| FX swap or funding operation | FX funding liquidity | The main issue may be access to foreign-currency funding rather than a simple spot-market currency target. | Funding relief can be temporary and may not change broader liquidity conditions by itself. |

| Verbal or signaling intervention | Expectations and market behavior | Officials may be trying to influence positioning, volatility, or expectations without immediate balance-sheet use. | Words do not supply reserves, domestic money, or funding liquidity unless followed by operations. |

| Reserve reallocation or balance-sheet change | Reserve composition and official-flow context | Reserve management may change currency composition, liquidity preference, or official-sector exposure. | A reserve accounting change is not the same as active market intervention unless the operation and channel are clear. |

Practical Scenario: Reserve Sale and Channel-Specific Liquidity

A central bank sells foreign exchange reserves to support its currency. The operation may supply foreign currency liquidity to the FX market because participants can obtain the currency being sold from reserves.

The same operation may reduce local-currency liquidity if the central bank receives local currency and leaves that liquidity withdrawn from the domestic system. If the central bank later offsets the local-currency effect through domestic operations, the domestic liquidity impact may be neutralized or changed.

The channel-specific reading is therefore: FX market liquidity may improve, reserves may decline, domestic liquidity may tighten or be offset, and the operation still does not become a currency forecast or trading signal.

Common False Readings

False reading: FX intervention always adds liquidity.

Cleaner reading: It may add liquidity to one channel while draining, offsetting, or leaving another channel unchanged.

False reading: Reserve sales always drain all liquidity.

Cleaner reading: Reserve sales can supply foreign currency to the FX market while the domestic liquidity effect depends on local-currency settlement and any offsetting operation.

False reading: Intervention proves the currency will strengthen.

Cleaner reading: Intervention shows official pressure or market-functioning concern, but the market response depends on size, credibility, liquidity conditions, positioning, and follow-through.

False reading: Intervention is a buy or sell signal.

Cleaner reading: It is a market-structure input. Market view and trade expression are separate decisions.

Liquidity Reading Checklist

FX intervention becomes more useful as liquidity context when the channel and offset are visible. A stronger reading usually separates what happened from what it may mean.

| Question | Why it matters |

|---|---|

| Was the operation spot, swap, forward, verbal, or reserve-management related? | The instrument helps identify whether the main channel is market liquidity, funding liquidity, or reserves. |

| Did reserves rise, fall, or only change composition? | Reserve movement helps separate intervention from accounting or allocation changes. |

| Was the domestic liquidity effect sterilized? | Sterilization can change the local money-market interpretation. |

| Was the stress in FX market depth or foreign-currency funding? | Spot liquidity stress and funding liquidity stress are different problems. |

| Do broader liquidity conditions confirm the reading? | Global liquidity conditions help prevent one FX operation from being overread as a complete regime signal. |

Where FX Intervention Fits in Market-Structure Analysis

FX intervention belongs in a broader capital-flow and liquidity framework. It can show official sensitivity to currency pressure, foreign-currency funding stress, reserve use, or market-functioning risk.

The interpretation stays cleaner when the operation is treated as pressure, not forecast. The channel, instrument, reserve effect, and sterilization decision define the liquidity reading more than the headline intervention label.

Use foreign exchange intervention for the broader concept of official currency-market operations.

Use foreign exchange reserves when the main question is reserve stock, reserve composition, or reserve drawdown.

Use global liquidity when the question is how broader liquidity conditions affect cross-asset market structure.

FAQ

Does FX intervention always add liquidity?

No. FX intervention can add liquidity to one channel, drain another channel, or leave the domestic effect mostly neutral if it is sterilized. The liquidity reading depends on the instrument, settlement, reserves, and offsetting operations.

Can FX intervention support market functioning without expanding domestic liquidity?

Yes. An operation can support FX market liquidity or foreign-currency funding while the domestic liquidity effect is offset through sterilization or other local money-market operations.

Is FX intervention a trading signal?

No. FX intervention is market-structure context. It may show pressure, funding stress, reserve use, or policy sensitivity, but it does not provide a standalone buy or sell instruction.

Why does sterilization matter for FX intervention?

Sterilization matters because it can offset the domestic money-market effect of the FX operation. Without checking sterilization, a reader may confuse a visible reserve transaction with the final liquidity impact.