Sentiment extremes do not mean a market top is near by themselves. An extreme reading can mark vulnerability only when it persists and is supported by positioning pressure, stretched flows, liquidity context, weakening breadth, or crowding risk.

The useful question is not whether sentiment is extreme in isolation. The useful question is whether the reading is part of a broader market structure where similar exposures, fragile liquidity, narrow leadership, or forced de-risking could make the market more sensitive to a reversal in flows.

What Sentiment Extremes Mean

Definition: A sentiment extreme is an unusually optimistic or pessimistic reading relative to normal conditions. It may come from surveys, option-positioning proxies, flow measures, risk-appetite dashboards, positioning data, or other sentiment-related inputs.

That makes sentiment extremes part of market sentiment analysis, but not the whole topic. Market sentiment describes the broader risk-appetite environment. A sentiment extreme is one condition inside that environment.

The main value is how the reading behaves next: whether it fades quickly, persists, becomes embedded in positioning, or appears alongside weaker liquidity and narrower market participation.

Common Mistake: Treating Extremes as Reversal Proof

The common mistake is to treat extreme optimism as automatic top evidence or extreme pessimism as automatic exhaustion evidence. That shortcut removes the context that makes sentiment useful.

A strong market can stay optimistic for longer than expected if liquidity remains supportive, leadership broadens, and flows keep reinforcing the move. A stressed market can stay pessimistic if liquidity is tight, breadth remains weak, and investors are still reducing exposure.

The correction is simple: sentiment extremes should be read as a condition, not a conclusion. They raise the need for confirmation. They do not provide the confirmation by themselves.

When a Sentiment Extreme Becomes More Meaningful

A sentiment extreme becomes more useful when it is connected to persistence and positioning. A single reading may only show mood. A persistent reading may show that market participants have started to cluster around the same exposure, narrative, or risk posture.

The interpretation becomes stronger when sentiment sits alongside flow and liquidity evidence. Extreme optimism matters more if inflows are stretched, leadership is narrow, and many participants appear positioned for the same continuation path. Extreme pessimism matters more when selling pressure looks exhausted, but only if liquidity and breadth stop deteriorating.

This is where sentiment analysis connects to crowded trade risk. Crowding does not mean a reversal must happen. It means the market may become more sensitive if the dominant exposure has to unwind through limited exit capacity.

| Observable condition | What it may suggest | What must confirm it | What can make it misleading |

|---|---|---|---|

| Extreme optimism | Risk appetite may be stretched. | Persistent exposure, narrow leadership, stretched flows, or weak breadth. | Supportive liquidity and broad participation can keep the trend intact. |

| Extreme pessimism | Stress or risk aversion may be elevated. | Stabilizing breadth, easing forced flows, and improving liquidity conditions. | Weak liquidity and continued de-risking can keep pressure in place. |

| Fast shift from fear to optimism | Positioning may be rebuilding quickly. | Sustained inflows, improving breadth, and confirmation across risk assets. | A short relief move can fade if macro or liquidity pressure remains unresolved. |

| Extreme reading from one dashboard or proxy | One sentiment input is stretched. | Agreement from other positioning, flow, breadth, or liquidity evidence. | Single-proxy readings can reflect method design rather than broad market pressure. |

Why Extreme Bullish Sentiment Can Mislead

Extreme bullish sentiment can look like obvious late-cycle evidence, but markets do not reverse because optimism exists. They become more fragile when optimism is persistent, widely held, and dependent on continuing inflows or liquidity support.

The difference matters. A market with strong breadth, healthy liquidity, and broad leadership can absorb optimistic sentiment better than a market where only a small group of leaders is carrying the index. In the second case, the same sentiment reading may matter more because the structure beneath it is thinner.

Extreme bullishness can also be a feature of a durable trend. If macro conditions remain supportive and market participation continues to expand, a high sentiment reading may describe confidence rather than exhaustion.

Why Extreme Bearish Sentiment Can Mislead

Extreme bearish sentiment can also be misread. A very pessimistic reading does not automatically mean selling pressure is exhausted. It may simply show that stress is visible while liquidity remains poor or forced de-risking is still active.

The better question is whether the conditions around the reading are stabilizing. Breadth should stop deteriorating, liquidity should improve, and selling pressure should become less forced before the reading becomes stronger evidence of exhaustion.

Without that confirmation, bearish sentiment can remain extreme for longer than expected. The reading may describe the mood correctly while still failing as a timing tool.

Practical Scenario: Extreme Sentiment With Weak Confirmation

A common scenario is that sentiment surveys become very optimistic while equity indices continue to rise. If breadth remains broad, credit conditions are calm, and liquidity is supportive, the reading may not be enough to suggest vulnerability. It may only show that market confidence is high.

The interpretation changes if leadership narrows, inflows concentrate into the same areas, credit spreads stop confirming risk appetite, and liquidity becomes less forgiving. In that setting, the same optimistic reading can become part of a broader vulnerability map.

The sentiment reading did not change its meaning alone. The surrounding structure changed the weight of the evidence.

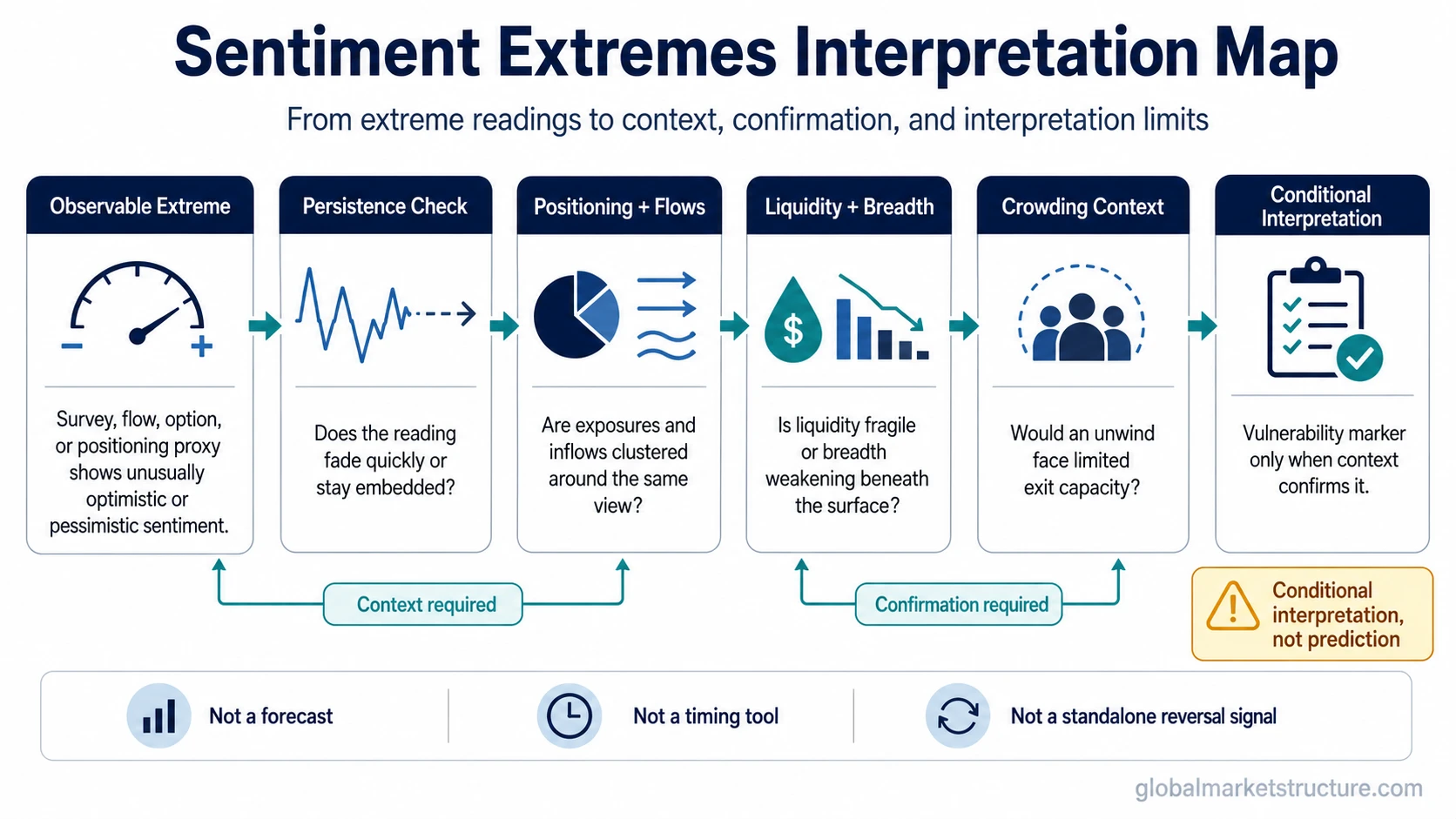

How to Read Sentiment Extremes Without Turning Them Into Signals

A safer approach is to treat sentiment extremes as the first question in a sequence. The reading may justify closer attention, but the interpretation should come from the surrounding evidence.

Start with persistence. A short-lived spike may only reflect temporary emotion. A persistent extreme can suggest that positioning and expectations are becoming more one-sided.

Then check flows and liquidity. If the market depends on continuing inflows and liquidity is becoming less supportive, the same sentiment reading carries more risk. If liquidity is still supportive and flows are balanced, the reading may be less important.

Finally, compare sentiment with breadth, leadership, and crowding. A sentiment extreme matters more when participation weakens and exposure becomes concentrated. It matters less when participation is broad and risk appetite is supported across several market segments.

Limits of Sentiment Extreme Analysis

Sentiment extremes are not forecasts. They do not identify the exact timing of a market top, bottom, reversal, or continuation. They are best used as context for interpreting vulnerability, exhaustion, or one-sided positioning.

The same reading can mean different things in different regimes. Extreme optimism during improving liquidity and broad participation is not the same as extreme optimism during narrow leadership and stretched flows. Extreme pessimism during forced deleveraging is not the same as pessimism after selling pressure has faded.

That is why sentiment extremes should not be separated from broader market structure. They become more useful when they are combined with positioning, liquidity, breadth, flows, and cross-asset confirmation.

How Sentiment Extremes Differ From Sentiment Indicators

Investor sentiment indicators are the tools or proxies used to observe market mood. They can include surveys, positioning measures, flow data, option-related proxies, and broader risk-appetite inputs.

Sentiment extremes are the unusually stretched readings that appear inside those tools or proxies. The indicator provides the measurement surface. The extreme creates the interpretation problem.

This distinction keeps the analysis cleaner. The question is not only which sentiment input is being used, but whether the stretched reading is persistent, confirmed by positioning and flows, and supported by liquidity, breadth, and crowding evidence.

Market Sentiment vs Crowding

Market sentiment describes the broad tone of risk appetite. Crowding describes how concentrated exposure may become when many participants are positioned in similar ways.

The two can overlap, but they are not the same. Sentiment can be optimistic without a trade being crowded. A trade can become crowded even if broad sentiment measures are not at an extreme.

The strongest warning usually comes when sentiment is extreme and positioning is also crowded. In that case, the issue is not mood alone. The issue is whether many participants may need to exit through the same liquidity channel if conditions change.

Summary

Sentiment extremes are useful only when they are interpreted as conditional evidence. They can show vulnerability, stress, or one-sided expectation, but they do not confirm market tops, bottoms, reversals, or timing by themselves.

The strongest interpretation comes from the surrounding structure: persistence, positioning, flows, liquidity, breadth, leadership, and crowding. Without that context, a sentiment extreme is only a stretched reading.

FAQ

Do sentiment extremes mean a market top is near?

No. Sentiment extremes do not mean a market top is near by themselves. They become more meaningful only when they persist and align with positioning pressure, stretched flows, weakening breadth, fragile liquidity, or crowding risk.

Can extreme bullish sentiment stay extreme for a long time?

Yes. Optimistic sentiment can persist when liquidity remains supportive, leadership is broad, and flows continue to reinforce the move. The risk rises when optimism becomes concentrated, one-sided, and dependent on fragile conditions.

Can extreme bearish sentiment be misleading?

Yes. Extreme bearish sentiment can describe stress without proving that stress is complete. It becomes more useful when breadth, liquidity, and flow conditions stop deteriorating.

Are sentiment dashboards timing tools?

No. Sentiment dashboards are proxy surfaces. They can help organize evidence, but their readings need confirmation from positioning, flows, liquidity, breadth, and broader market structure.